An effective investment strategy is vital to ensuring The Jack Brockhoff Foundation can continue its good work in providing support and funding to organisations that benefit the community. Our recommendations are designed to ensure this objective can be sustained in perpetuity, with the highest degree of certainty possible given difficult investment conditions.

Recommendation 1: Risk and Return Targets

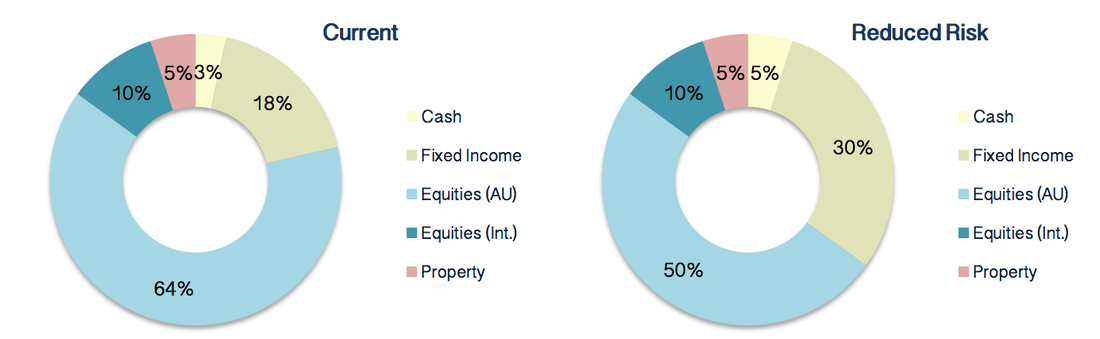

The Foundation’s investment strategy specifies a target asset allocation of 85% growth assets (currently 79%) and 15% in fixed income and cash. The investment guidelines also set an income target of 5% per annum and capital growth of CPI+1%.

On an assessment of the current investment climate, including the continued decline in cash and fixed income yields, we believe the Foundation's investment targets command a level of risk which could result in permanent, if not irreparable damage to the corpus.

The Foundation’s investment strategy specifies a target asset allocation of 85% growth assets (currently 79%) and 15% in fixed income and cash. The investment guidelines also set an income target of 5% per annum and capital growth of CPI+1%.

On an assessment of the current investment climate, including the continued decline in cash and fixed income yields, we believe the Foundation's investment targets command a level of risk which could result in permanent, if not irreparable damage to the corpus.

Recommendation 1a:

For this reason, it is recommended that the Foundation consider reducing making a temporary adjustment to investment allocations, reducing exposure to growth assets from 85% to 65%.

For this reason, it is recommended that the Foundation consider reducing making a temporary adjustment to investment allocations, reducing exposure to growth assets from 85% to 65%.

This reduction in growth assets will be balanced by a 20% increase in defensive assets. We must accept that this reallocation will (or at least should be expected to) result in a material reduction of portfolio earnings. While we don’t want to forfeit returns unnecessarily, the primary focus of this rebalance must be capital preservation[1].

In an effort to best address the issues around portfolio risk we would suggest this 20% reduction come from Australian equities. The cost of this risk reduction is estimated at $2 million in lost earnings over five years. Beyond the benefits in reducing portfolio volatility, this can be expected to provide a net financial benefit in the event that during this time the local share market sustains a fall of 16%. We believe that a market adjustment will be more substantial (and quite likely sooner) than this, hence we believe the cost (i.e., lower earnings) justify lowering the Foundation’s exposure to risk assets. This reduced risk allocation should be reviewed every 12 -18 months.

In an effort to best address the issues around portfolio risk we would suggest this 20% reduction come from Australian equities. The cost of this risk reduction is estimated at $2 million in lost earnings over five years. Beyond the benefits in reducing portfolio volatility, this can be expected to provide a net financial benefit in the event that during this time the local share market sustains a fall of 16%. We believe that a market adjustment will be more substantial (and quite likely sooner) than this, hence we believe the cost (i.e., lower earnings) justify lowering the Foundation’s exposure to risk assets. This reduced risk allocation should be reviewed every 12 -18 months.

We should also note that changing the asset allocation targets would cause a mismatch with the Foundation’s return objectives. By allocation a higher proportion of a portfolio to assets yielding a relatively low (<2.6%) return the guideline income target of 5% will become further out of reach. Attempting to meet this target through the portfolio’s growth assets would corner investment managers into chasing yield at the expense of maximising total return and risk of permanent loss of capital.

Recommendation 1b:

It is recommended that the Foundation make two changes to investment guidelines:

It is recommended that the Foundation make two changes to investment guidelines:

- Income Target: It is recommended the income target be set with reference to the official cash rate (example: RBA cash rate + 2%).

- Total Return Target: The Foundation should focus on total returns relative to CPI. The Foundation’s existing target is equivalent to CPI+6% over rolling 5-year periods. This remains appropriate, albeit at the higher range of market expectations over the mid-term given tolerance for negative returns no more than one-in-five years.

This will improve the flexibility with which investment managers can pursue The Foundation’s long-term return objectives, reduces the risk of channeling investment managers toward potential yield traps. We provide a short summary of a selection fixed income products and associated risk profiles here.

Recommendation 2: Vanguard Australian High Yield Fund

Although Vanguard’s Australian High Yield Fund has done consistently well in tracking its benchmark, we do have concerns as to whether the strategy is appropriate given the Foundation's discomfort with risk and the present outlook for the Australian economy.

Of particular concern is the Fund’s investment methodology, which ranks securities on the basis of prospective yield, without regard to dividend stability or company quality. If weakness in Australia’s economy persists we could see earnings growth reduce sharply and dividends reduced across sectors with either high levels of debt or capital adequacy requirements (such as banks’ CET1).

Bear in mind too that markets tend to react quickly and favorably to increases in dividends, and equally quickly but negatively when dividends are cut. Vanguard’s strategy – which is only rebalanced quarterly and on the basis of prospective dividends - is by design more prone to the negative impacts from of dividend announcements.

While an economic downturn is by no means assured, history has shown that mandates with the flexibility and agility to respond to market crises tend to outperform (both protecting and redeploying capital).

Although Vanguard’s Australian High Yield Fund has done consistently well in tracking its benchmark, we do have concerns as to whether the strategy is appropriate given the Foundation's discomfort with risk and the present outlook for the Australian economy.

Of particular concern is the Fund’s investment methodology, which ranks securities on the basis of prospective yield, without regard to dividend stability or company quality. If weakness in Australia’s economy persists we could see earnings growth reduce sharply and dividends reduced across sectors with either high levels of debt or capital adequacy requirements (such as banks’ CET1).

Bear in mind too that markets tend to react quickly and favorably to increases in dividends, and equally quickly but negatively when dividends are cut. Vanguard’s strategy – which is only rebalanced quarterly and on the basis of prospective dividends - is by design more prone to the negative impacts from of dividend announcements.

While an economic downturn is by no means assured, history has shown that mandates with the flexibility and agility to respond to market crises tend to outperform (both protecting and redeploying capital).

Recommendation 2:

For this reason we recommend that the Foundation withdraw from Vanguard Australian High Yield Fund.

For this reason we recommend that the Foundation withdraw from Vanguard Australian High Yield Fund.

Important: While we have not provided advice on where to redeploy this capital we do point out that the Foundation's (current) investment guidelines recommend using a minimum of three investment managers.

Recommendation 3: Ethical Screening of Investments

Having reviewed the research, performed an attribution analysis of the Australian share market and analysed the Foundation’s investment portfolio we conclude that the direct impact from implementing an ethical screen in the manner proposed by the Foundation is between 0.08% and 0.17% per annum (roughly $37,000 to $82,000 per annum).

Though this cost is fairly minimal in comparison to the size of the portfolio and return objectives, we must acknowledge that formal implementation of an ethical screening process may cause compliance issues, especially if the definition of what does or does not constitute an ‘ethical’ investment leaves room for interpretation.

What’s more, these costs also bring forward the important question as to whether a loss of prospective returns achieves greater benefit[2] (i.e., more “good”) than would otherwise be created were these additional returns contributed toward disbursements.

Of course deciding whether the Foundation should or should not pursue an ethical mandate is not for us to say. We can confidently assert that there will be a cost and potential compliance risks, but as the motive behind ‘ethical investing' is not to increase returns the Board must decide whether the qualitative and ideological benefits justify the expense.

Having reviewed the research, performed an attribution analysis of the Australian share market and analysed the Foundation’s investment portfolio we conclude that the direct impact from implementing an ethical screen in the manner proposed by the Foundation is between 0.08% and 0.17% per annum (roughly $37,000 to $82,000 per annum).

Though this cost is fairly minimal in comparison to the size of the portfolio and return objectives, we must acknowledge that formal implementation of an ethical screening process may cause compliance issues, especially if the definition of what does or does not constitute an ‘ethical’ investment leaves room for interpretation.

What’s more, these costs also bring forward the important question as to whether a loss of prospective returns achieves greater benefit[2] (i.e., more “good”) than would otherwise be created were these additional returns contributed toward disbursements.

Of course deciding whether the Foundation should or should not pursue an ethical mandate is not for us to say. We can confidently assert that there will be a cost and potential compliance risks, but as the motive behind ‘ethical investing' is not to increase returns the Board must decide whether the qualitative and ideological benefits justify the expense.

Note: I will comment that should the Foundation wish to pursue an ethical strategy, the investment guidelines should be worded very carefully (perhaps stating a preference to avoid particular industries). This will reduce inadvertent breaches of the guidelines.

[1] This is important to keep in mind. With global interest rates trawling record lows, fixed income Funds are struggling to find returns. Many have responded by reducing portfolio credit quality, increasing duration and focusing on headline yields. This gives the appearance of better returns in the short term, but a significant risk if the global economic outlook improves. Accordingly, high-quality short and medium term bonds and deposits will be more appropriate than some of the superficially attractive issues, such as those currently being offered by "third-tier" lenders/financiers.

[2] Keep in mind that the secondary market neither adds nor removes capital from the firm. In fact, we can argue that shareholders' voting rights provide them with greater influence/control.

[2] Keep in mind that the secondary market neither adds nor removes capital from the firm. In fact, we can argue that shareholders' voting rights provide them with greater influence/control.