With local interest rates already at record lows, and the RBA expressing concern over the ability of monetary policy to effect change without further inflating property prices (household debt), returns from fixed income products are likely to be lower in the years ahead.

In an effort to provide some perspective as to the yields on offer, we have provided below a very brief selection of fixed income products (both managed funds and a selection of public/private sector debt).

We have included not only the current Yield to Maturity, but also the expected total return were the local economy become weaker or stronger. Under the scenario of a weaker economy, we assume a 0.5% interest rate cut plus a moderate increase in defaults (calculations controlled for credit quality). In a scenario of a stronger economy we assume a 0.5% interest rate rise.

In an effort to provide some perspective as to the yields on offer, we have provided below a very brief selection of fixed income products (both managed funds and a selection of public/private sector debt).

We have included not only the current Yield to Maturity, but also the expected total return were the local economy become weaker or stronger. Under the scenario of a weaker economy, we assume a 0.5% interest rate cut plus a moderate increase in defaults (calculations controlled for credit quality). In a scenario of a stronger economy we assume a 0.5% interest rate rise.

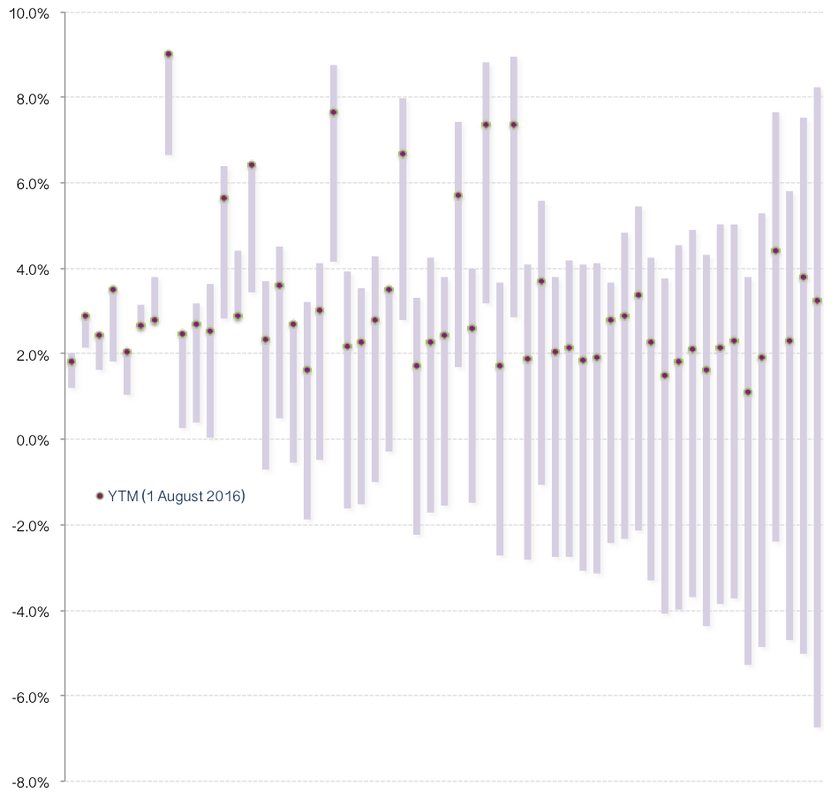

Ranked by YTM

Portfolios are ranked based on current Yield to Maturity. A general observation is that markets appear to be pricing in further deterioration in the local economy. Yields on government issued bonds (state and Federal) are being squeezed to record lows while the same effect is not flowing through to corporate bonds ( the exception being the banks and some large foreign issues like AAPL).

Considering the balance sheets of many of the companies issuing debt it does seem that default risk is somewhat overstated. In saying that, once we get above a YTM of around 4% we see a moderate acceleration in risk. To minimise the capital at risk (default-less-recovery risk) investors would be well served by focusing on issuers’ balance sheets, as well as free cash flow to equity and interest coverage margins.

Portfolios are ranked based on current Yield to Maturity. A general observation is that markets appear to be pricing in further deterioration in the local economy. Yields on government issued bonds (state and Federal) are being squeezed to record lows while the same effect is not flowing through to corporate bonds ( the exception being the banks and some large foreign issues like AAPL).

Considering the balance sheets of many of the companies issuing debt it does seem that default risk is somewhat overstated. In saying that, once we get above a YTM of around 4% we see a moderate acceleration in risk. To minimise the capital at risk (default-less-recovery risk) investors would be well served by focusing on issuers’ balance sheets, as well as free cash flow to equity and interest coverage margins.

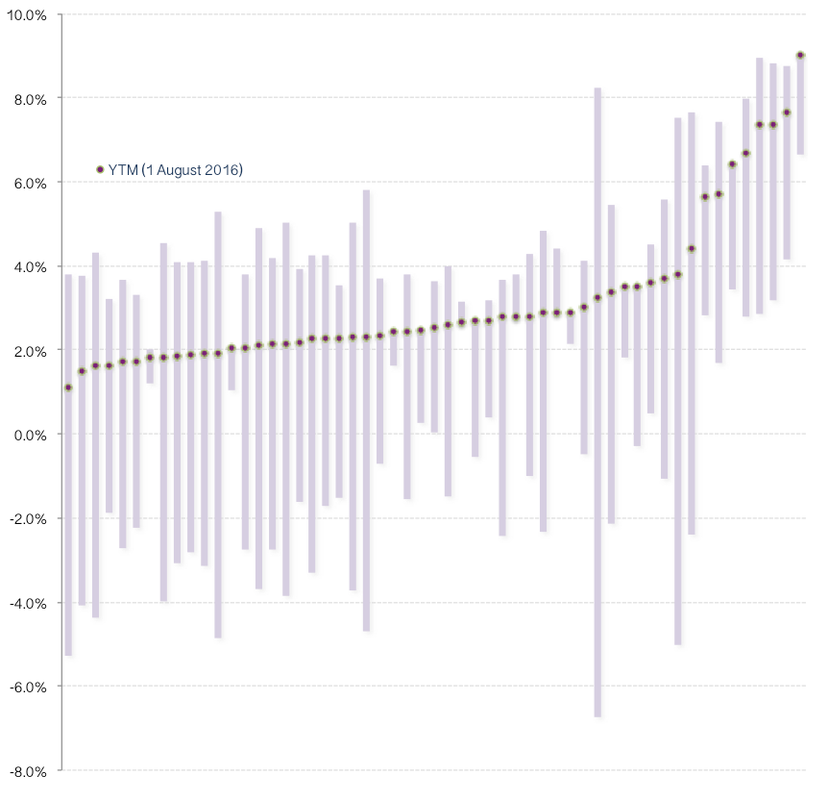

Ranked by Risk

Portfolios are ranked based on underlying risk (left = low risk, right = high risk). This includes credit risk, interest rate risk and manager risk (where applicable).

Portfolios are ranked based on underlying risk (left = low risk, right = high risk). This includes credit risk, interest rate risk and manager risk (where applicable).

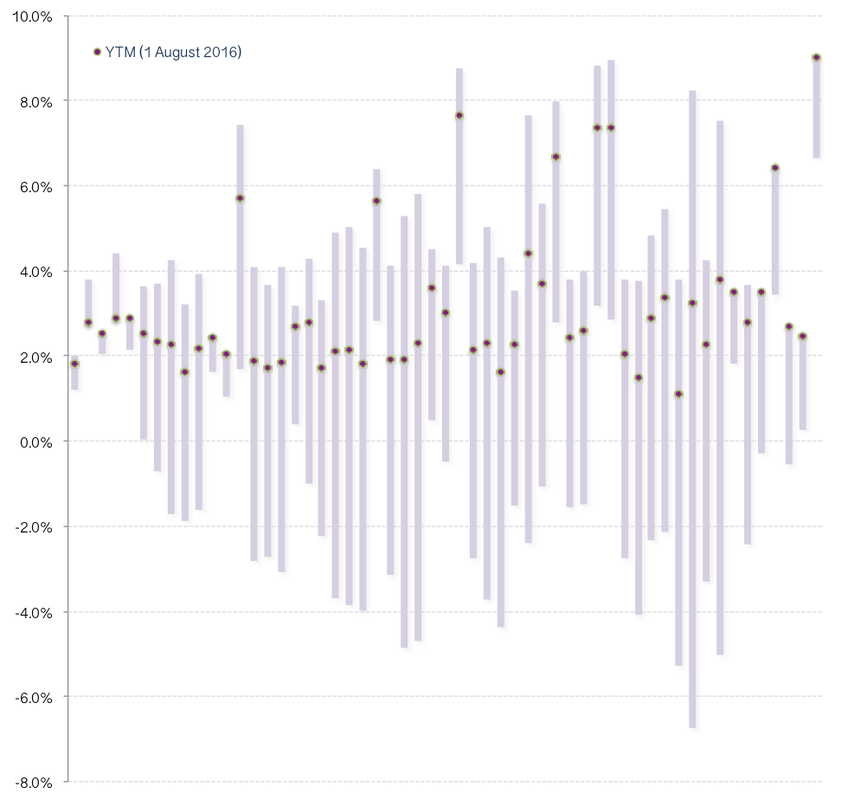

Ranked by Duration