The Board has raised the question as to whether an ethical screen can be implemented without substantial impact on the income or maintenance of capital value.

Indeed the question as to whether the ethics and behavior of companies affect shareholder returns is one that has attracted significant attention over recent decades from investors, academics, analysts and product manufacturers alike.

Of course, the starting point in evaluating the impact of ethically screened portfolios is first to define what we mean by ethical, or perhaps what more importantly what consider unethical (or otherwise earmarked for exclusion).

The Jack Brockhoff Foundation has enquired as to the potential impact of an ethical screen that specifically excludes companies whose primary businesses are in tobacco, alcohol, gaming, and armaments. Our review seeks to identify and quantify the costs associated with this type of filter, and evaluating the impact of this on The Foundation’s long-term goals and objectives.

As The Foundation's focus is on the impact of excluding specific business practices we focus our attention on the body of research covering Socially Responsible Investment (SRI) practices[1]. Furthermore, we have concentrated our efforts on measuring and estimating the impact of SRI on prospective returns; we have not discussed the qualitative or ideological reasons for pursuing such a strategy, partly because this is relatively inconsequential for secondary market securities[2].

Indeed the question as to whether the ethics and behavior of companies affect shareholder returns is one that has attracted significant attention over recent decades from investors, academics, analysts and product manufacturers alike.

Of course, the starting point in evaluating the impact of ethically screened portfolios is first to define what we mean by ethical, or perhaps what more importantly what consider unethical (or otherwise earmarked for exclusion).

The Jack Brockhoff Foundation has enquired as to the potential impact of an ethical screen that specifically excludes companies whose primary businesses are in tobacco, alcohol, gaming, and armaments. Our review seeks to identify and quantify the costs associated with this type of filter, and evaluating the impact of this on The Foundation’s long-term goals and objectives.

As The Foundation's focus is on the impact of excluding specific business practices we focus our attention on the body of research covering Socially Responsible Investment (SRI) practices[1]. Furthermore, we have concentrated our efforts on measuring and estimating the impact of SRI on prospective returns; we have not discussed the qualitative or ideological reasons for pursuing such a strategy, partly because this is relatively inconsequential for secondary market securities[2].

Evaluating the cost

To ensure a fair and balanced assessment of the costs or benefits of SRI we approached the question of impact on investment returns from three distinct, yet ultimately related angles:

• Review of the existing research.

• Opportunity cost.

• Administration costs.

To ensure a fair and balanced assessment of the costs or benefits of SRI we approached the question of impact on investment returns from three distinct, yet ultimately related angles:

• Review of the existing research.

• Opportunity cost.

• Administration costs.

Results (highlights)

- There is a direct relationship between the strictness of SRI-screening parameters and the costs incurred. The stricter the requirements the higher the cost. The ethical screen proposed by The Foundation is toward the lowest-cost end of the scale.

- Implementing a complete ethical screen (SRI) can be expected to reduce listed property and equity investment returns by between 0.10% and 0.22% per annum, over the long term. This is equivalent to a reduction in The Jack Brockhoff Foundation’s gross returns of between $37,000 to $82,000 per annum.

- Both Deutsche Bank and Macquarie have indicated there will be no direct increase in fees as a result of changing the investment mandate, however, we should accept there will be an indirect cost through their managed fund holdings. We estimate this cost at $14,000 per annum.

- Between $23,000 and $68,000 per annum (0.05% - 0.14%) can be attributed to opportunity costs (reducing the number and breadth of eligible securities)

- The costs from implementing an ethical screen are highest for equity investments. Thus a reduction in risk assets would be expected to reduce the overall cost.

- While the evidence suggests that SRI reduces returns over the long run, SRI portfolios tend to exhibit lower overall volatility and outperform their market benchmark in times of market crisis.

- In periods of crisis, companies that fare the worst also tend to share the lowest SRI and ESG ratings, though this relationship is only statistically significant on an ex-post basis. SRI rankings appear to be of no use in predicting future performance.

- We note that outperformance in times of crisis is likely a side effect of SRI portfolios carrying less market exposure than normal equity portfolios (i.e., a beta of less than 1.0; research suggests an average of around 0.8). It’s important to note that this paints a somewhat distorted view of returns: on a risk-adjusted basis SRI strategies tend to return about the same as unconstrained equity mandates, yet this comparison only takes into account portfolio volatility and not real capital risk or alternative use of cash.

- While the evidence suggests that SRI strategies underperform in the long run, there is insufficient evidence to suggest that “unethical” industries offer higher returns to investors. This leads us to believe that SRI underperformance is a second order effect; a consequence of investment constraints, additional compliance and management fees and reduced portfolio efficiency.

- SRI mandates necessitate ongoing monitoring and management. The Foundation must be careful to define what assets are and are not eligible for investment, and must put measures in place to ensure compliance with these directives.

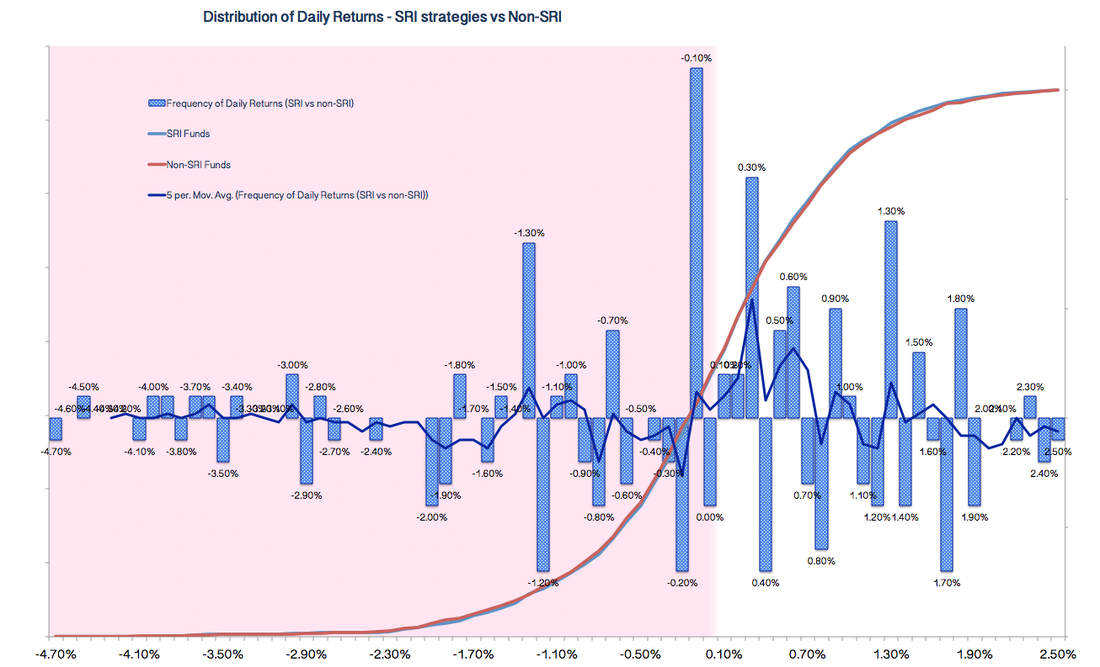

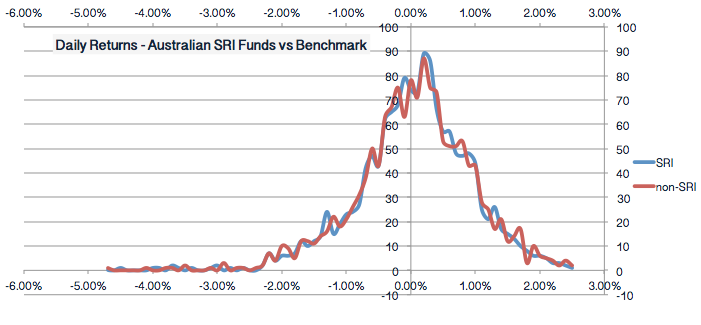

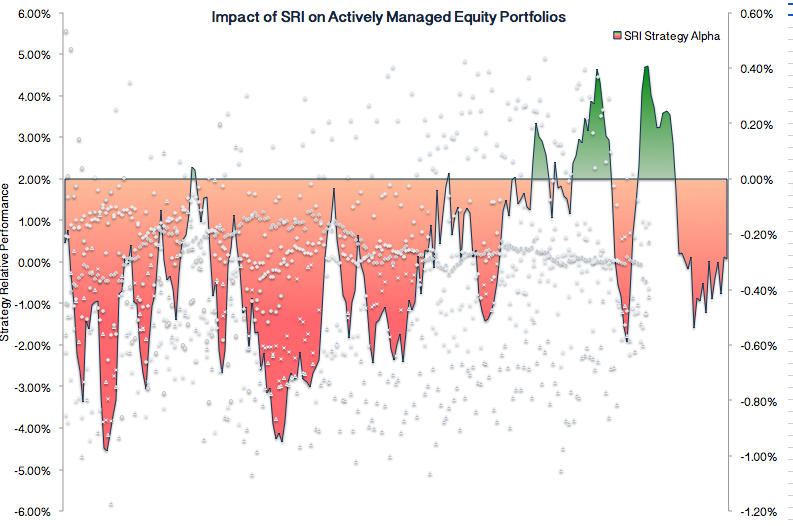

We found numerous investment advisers running portfolios with SRI and non-SRI versions. Comparing the portfolio return and volatility data allows us to see how returns differ. Interestingly, we find that SRI funds report relatively frequent, but small, losses. These are partly made up for with periods of outperformance, but with not enough consistency to generate alpha long-term.

|

|

Conclusion

Our research suggests that implementing an ethical screen to The Jack Brockhoff Foundation’s portfolio can be expected to reduce prospective returns by between $37,000 and $82,000 per annum (0.08% - 0.17%).

While the overall cost of implementing the suggested ethical screen is low in proportion to The Foundation's long-term return objectives it is prudent to consider the cost of this decision against the potential benefit that may be achieved from investing with an unconstrained mandate.

In other words: is more "good" achieved by increasing Foundation disbursements or by avoiding particular sectors?

The Board must also consider the practical and administrative implications. Placing exclusions on assets based upon their behaviour invariably increases the likelihood of a breach occurring, particularly if sections of the portfolio are managed via external unit trusts or internally by The Foundation’s staff.

In conclusion, we find that while implementing an ethical screen does come at a cost it is unlikely to have a substantial impact on The Foundation's investment income or ability to preserve the inflation-adjusted value of the corpus. It does, however, present a number of administrative challenges and responsibilities that will require ongoing monitoring and management.

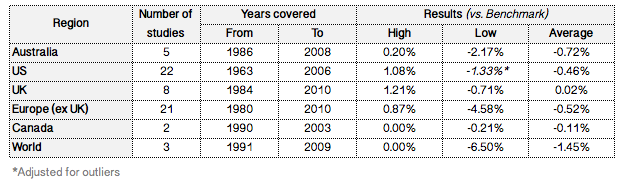

Most empirical research into SRI strategies finds a penalty on returns of 0% - 0.5% p.a.

|

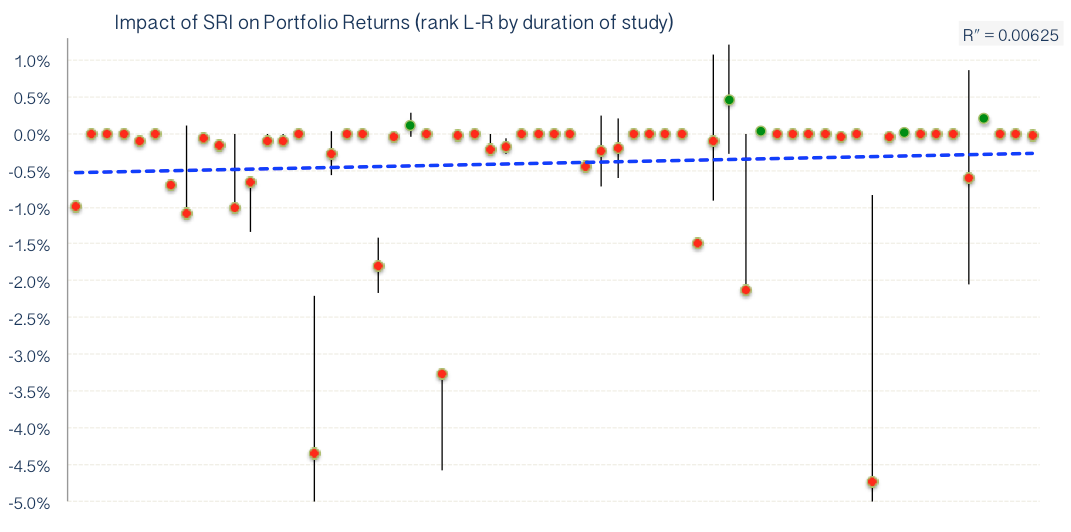

Timing is everything: We found that SRI out/(under)performance depends greatly on an investor's entry and exit point.

|

[1] This acronym is commonly used interchangeably with Sustainable and Responsible Investment (SRI). Be aware that the approach used in SRI differs from ESG (Environmental, Social, and Corporate Governance), which focuses less on the sector in which a company operates, and more on how the company is managed.

[2] Though shareholder advocacy has increased asset managers' influence on the behaviour of business, this concentrates more on the corporate governance and reputational aspects, not business activities. Within the context of large secondary-market securities (such as listed equities), the decision to divest from particular sectors is likely to be inconsequential to the companies in question.

[2] Though shareholder advocacy has increased asset managers' influence on the behaviour of business, this concentrates more on the corporate governance and reputational aspects, not business activities. Within the context of large secondary-market securities (such as listed equities), the decision to divest from particular sectors is likely to be inconsequential to the companies in question.