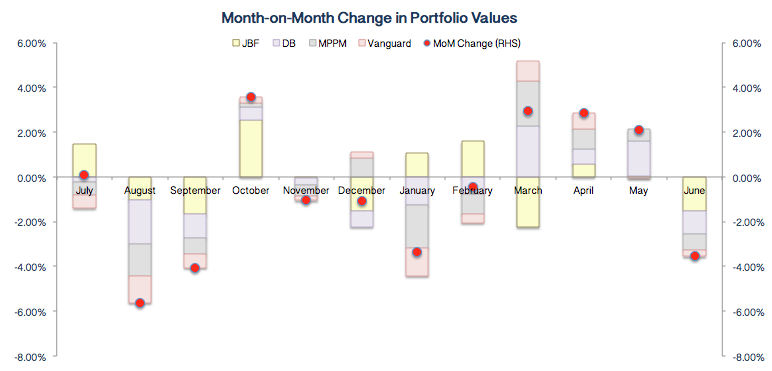

At the close of trade on 30 June 2016, The Jack Brockhoff Foundation's portfolio was valued at $47.48 million. Adjusted for accrued interest, imputation credits, refunds and prepayments of $1.03 million, the total value of The Foundation’s investment assets is valued at approximately $48.51 million. This represents a $3.0 million reduction from the Foundation’s opening balance (including receivables) of $51.52 million.

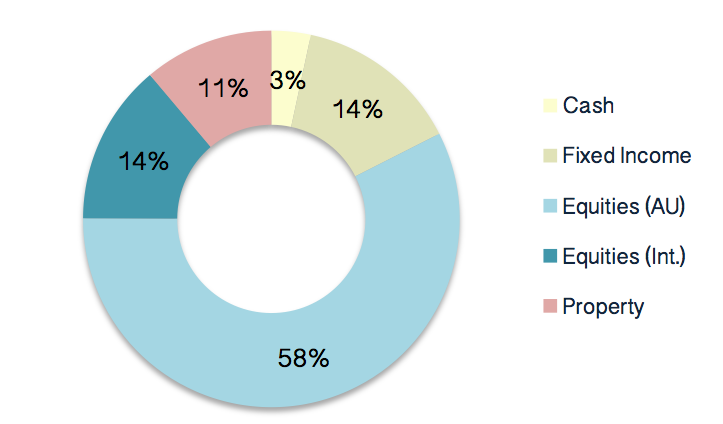

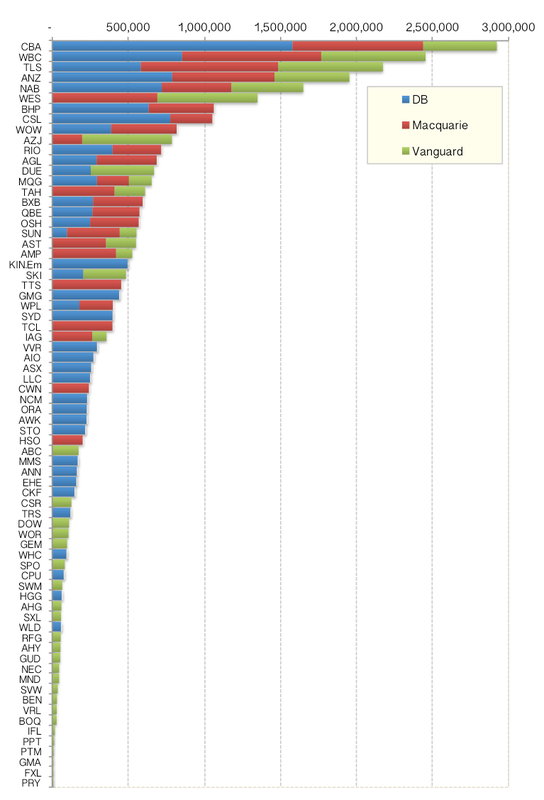

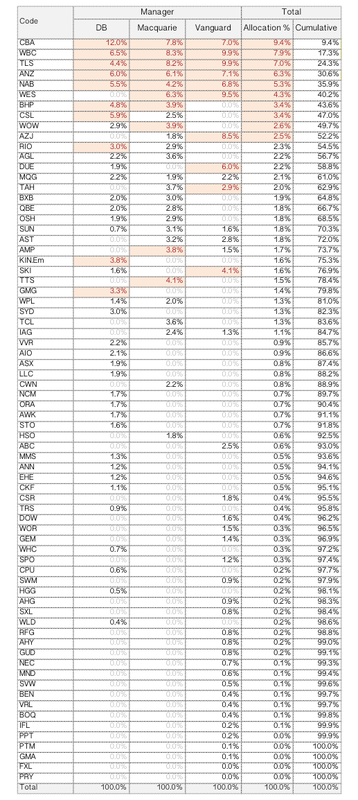

In accordance with investment guidelines three investment managers are employed to invest the Foundation’s assets. Deutsche Bank and Macquarie manage the bulk of these assets (~85%) using an active management style, while Vanguard (~15%) employs a passive rules-based approach.

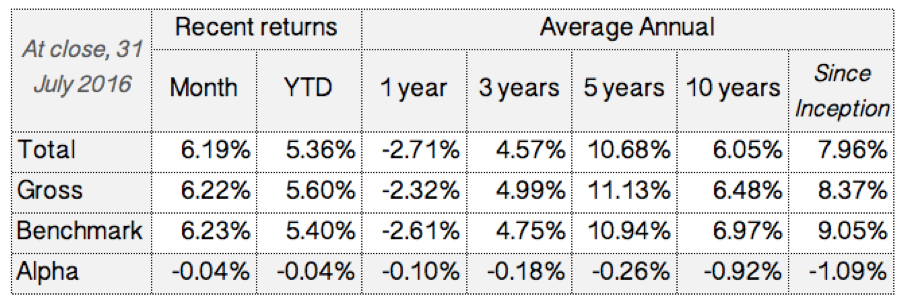

All Fund managers underperformed their benchmarks. The most severe underperformance relative to benchmark was from Deutsche Bank (+0.85% vs. +4.26%), while the worst absolute return was from Vanguard (-6.64% vs. -6.59%)

All Fund managers underperformed their benchmarks. The most severe underperformance relative to benchmark was from Deutsche Bank (+0.85% vs. +4.26%), while the worst absolute return was from Vanguard (-6.64% vs. -6.59%)

Deutsche Bank AG

Deutsche Bank manage approximately $21.3 million of The Foundation’s assets. This is equivalent to approximately 45% of Foundation assets. The account manager is Director and head of Discretionary Portfolio Management, Tim Gough.

For the financial year to 30 June 2016, Deutsche Bank’s portfolio underperformed its benchmarks, achieving a time-weighted return (inclusive of all franking credits) of approximately 0.85%, as compared to an asset-weighted benchmark return of 4.26%.

This rather significant underperformance (-3.41%) appears almost entirely attributable to poor security selection, as opposed to reckless investment behavior. Though this is comforting to know, their net results are especially disappointing when we consider that their asset allocation (exposure to equities, property, fixed income etc.) decisions were actually very well formed.

Put simply, FY2016 seems to have been a year where they got the themes (strategic asset allocation) right, but tactics (security selection) wrong.

On review of their portfolio, risk management guidelines and track record over 3 and 5 years there does not appear to be any immediate cause for concern as to their competence or motivation to act in the best interest of The Foundation.

Deutsche Bank manage approximately $21.3 million of The Foundation’s assets. This is equivalent to approximately 45% of Foundation assets. The account manager is Director and head of Discretionary Portfolio Management, Tim Gough.

For the financial year to 30 June 2016, Deutsche Bank’s portfolio underperformed its benchmarks, achieving a time-weighted return (inclusive of all franking credits) of approximately 0.85%, as compared to an asset-weighted benchmark return of 4.26%.

This rather significant underperformance (-3.41%) appears almost entirely attributable to poor security selection, as opposed to reckless investment behavior. Though this is comforting to know, their net results are especially disappointing when we consider that their asset allocation (exposure to equities, property, fixed income etc.) decisions were actually very well formed.

Put simply, FY2016 seems to have been a year where they got the themes (strategic asset allocation) right, but tactics (security selection) wrong.

On review of their portfolio, risk management guidelines and track record over 3 and 5 years there does not appear to be any immediate cause for concern as to their competence or motivation to act in the best interest of The Foundation.

Macquarie Private Portfolio Management

Macquarie Private Portfolio Management (MPPM) manage approximately $18.9 million of The Foundation’s assets. This is equivalent to approximately 40% of Foundation assets. The account manager is Senior Investment Advisor, David Mattner.

For the financial year to 30 June 2016, Macquarie’s portfolio underperformed its benchmarks, achieving a time-weighted return (inclusive of all franking credits) of approximately 1.10%, as compared to an asset-weighted benchmark return of 2.59%.

Relative to benchmark, MPPM underperformed across all asset categories, though by a less dramatic margin than Deutsche Bank. MPPM employ a segmented approach to portfolio management, appointing each asset category toward a portfolio recommended by specialist asset management teams.

After adjusting for franking, MPPM's Australian and international equity portfolios underperformed by approximately 0.11% and 0.27% respectively. A more substantial underperformance was realised by the fixed income portfolio, which fell short of the benchmark by an estimated 2.6%.

On the matter of fixed income performance, we must note that the Foundation’s investment strategy (with both MPPM and Deutsche Bank) is somewhat different to that of the benchmark, as both managers have incorporated hybrid issues and a somewhat more conservative tilt to their securities selection. Although this appears to have been a drag on returns over the past year, we must bear in mind that the benchmark's strong performance is more a function of a worse-than-expected economic slowdown and falling interest rate cuts. We believe both MPPM and Deutsche Bank have been prudent in their approach to fixed-income portfolio construction.

Despite Macquarie’s underperformance over the past year, the underlying strategies remain consistent and on-track with their medium to long-term objectives.

Macquarie Private Portfolio Management (MPPM) manage approximately $18.9 million of The Foundation’s assets. This is equivalent to approximately 40% of Foundation assets. The account manager is Senior Investment Advisor, David Mattner.

For the financial year to 30 June 2016, Macquarie’s portfolio underperformed its benchmarks, achieving a time-weighted return (inclusive of all franking credits) of approximately 1.10%, as compared to an asset-weighted benchmark return of 2.59%.

Relative to benchmark, MPPM underperformed across all asset categories, though by a less dramatic margin than Deutsche Bank. MPPM employ a segmented approach to portfolio management, appointing each asset category toward a portfolio recommended by specialist asset management teams.

After adjusting for franking, MPPM's Australian and international equity portfolios underperformed by approximately 0.11% and 0.27% respectively. A more substantial underperformance was realised by the fixed income portfolio, which fell short of the benchmark by an estimated 2.6%.

On the matter of fixed income performance, we must note that the Foundation’s investment strategy (with both MPPM and Deutsche Bank) is somewhat different to that of the benchmark, as both managers have incorporated hybrid issues and a somewhat more conservative tilt to their securities selection. Although this appears to have been a drag on returns over the past year, we must bear in mind that the benchmark's strong performance is more a function of a worse-than-expected economic slowdown and falling interest rate cuts. We believe both MPPM and Deutsche Bank have been prudent in their approach to fixed-income portfolio construction.

Despite Macquarie’s underperformance over the past year, the underlying strategies remain consistent and on-track with their medium to long-term objectives.

Vanguard High Yield Fund

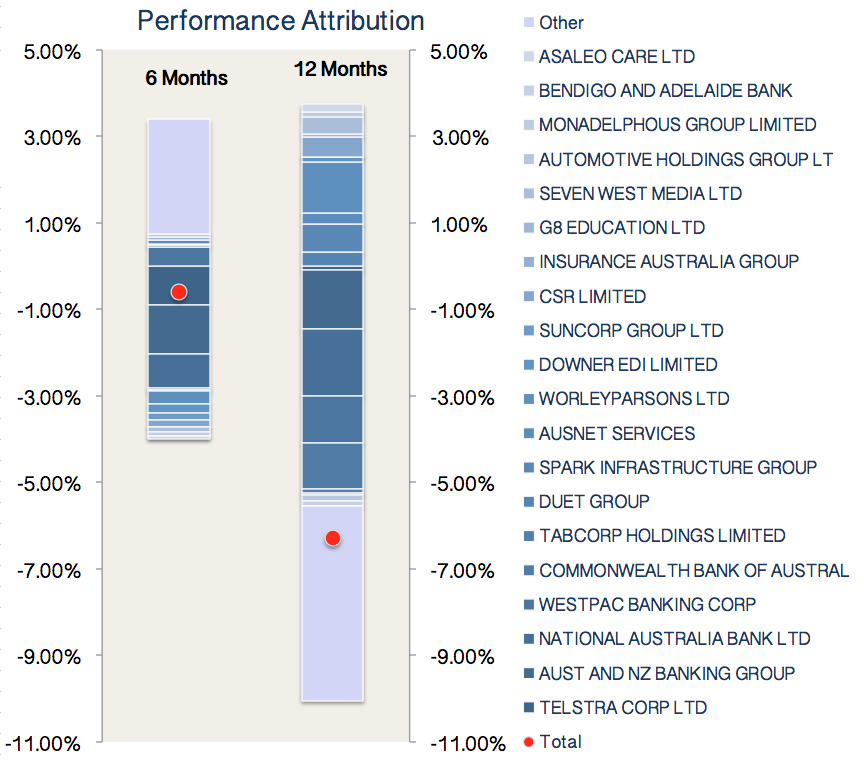

The standout non-performer over the past year has been the Vanguard High Yield Fund, which delivered a loss of 6.64% (~$547,000). In response, the Directors have, quite appropriately, sought to review the Fund's strategy and it's suitability for ongoing inclusion in The Foundation's portfolio.

To provide an answer to this question we must appreciate that the Vanguard High Yield Fund’s objective is not to achieve an absolute return on capital or to avoid loss; rather it merely tries to mimic the FTSE ASFA Australian High Dividend Yield Index. As a “rules-based” benchmark that is focused only on the prospective dividend yield of Australian shares the Fund is not interested in the risk or sustainability of its constituents.

This approach offers a number of benefits, including ensuring a good level of liquidity and a reasonably well-diversified portfolio under normal conditions. However, this approach does have a number of downsides. Most obvious is that the ranking and weighting process can lead to periods of significant portfolio concentration. A related point is that as the construction methodology does not consider qualitative factors, which can over-expose the portfolio to companies forecasting abnormal, unsustainable or unattainable levels of dividends.

An example of this is the Australian banking sector, which has seen many of our largest banks dramatically increase the proportion of earnings distributed to shareholders. As credit growth continues to slow this may indeed be the best use of shareholder capital (best outcome for bank shareholders); yet whether it justifies investing in the banks – especially when retained earnings are often necessary for growth - is an entirely different matter.

Despite the Fund’s relative success in tracking its benchmark, we do have our reservations as to whether it remains appropriate for The Foundation at this moment in time. Of particular concern is that as valuations between sectors diverge this strategy is prone to becoming over-exposed to particular sectors or “yield traps”.

The standout non-performer over the past year has been the Vanguard High Yield Fund, which delivered a loss of 6.64% (~$547,000). In response, the Directors have, quite appropriately, sought to review the Fund's strategy and it's suitability for ongoing inclusion in The Foundation's portfolio.

To provide an answer to this question we must appreciate that the Vanguard High Yield Fund’s objective is not to achieve an absolute return on capital or to avoid loss; rather it merely tries to mimic the FTSE ASFA Australian High Dividend Yield Index. As a “rules-based” benchmark that is focused only on the prospective dividend yield of Australian shares the Fund is not interested in the risk or sustainability of its constituents.

This approach offers a number of benefits, including ensuring a good level of liquidity and a reasonably well-diversified portfolio under normal conditions. However, this approach does have a number of downsides. Most obvious is that the ranking and weighting process can lead to periods of significant portfolio concentration. A related point is that as the construction methodology does not consider qualitative factors, which can over-expose the portfolio to companies forecasting abnormal, unsustainable or unattainable levels of dividends.

An example of this is the Australian banking sector, which has seen many of our largest banks dramatically increase the proportion of earnings distributed to shareholders. As credit growth continues to slow this may indeed be the best use of shareholder capital (best outcome for bank shareholders); yet whether it justifies investing in the banks – especially when retained earnings are often necessary for growth - is an entirely different matter.

Despite the Fund’s relative success in tracking its benchmark, we do have our reservations as to whether it remains appropriate for The Foundation at this moment in time. Of particular concern is that as valuations between sectors diverge this strategy is prone to becoming over-exposed to particular sectors or “yield traps”.

|

|

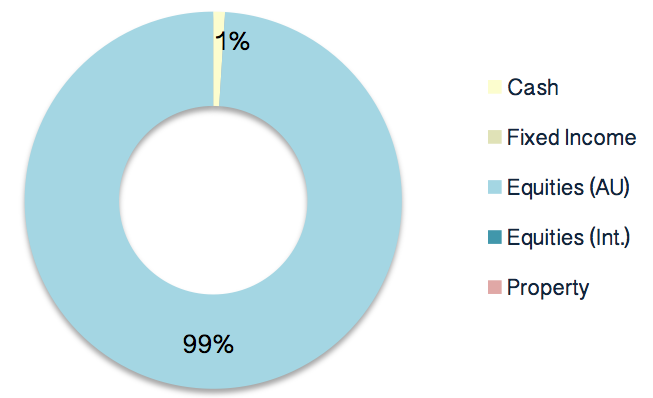

As at 30 June 2016, the portfolio had approximately 40% of the portfolio invested in four banks, plus Telstra. This is despite the fact that within the Fund's portfolio these companies offered among the lowest prospective yield.

Summary

For the 2016 Financial Year, the Foundation’s investment portfolio recorded a loss of approximately $520,000 (1.02%), with disbursements and expenses producing a reduction in total assets (including receivables) of approximately $3.0 million.

All external investment advisers underperformed their benchmarks over the year. While not ideal, returns were still within range of their asset-weighted benchmark. This should be viewed as a relatively satisfactory outcome given very challenging investment conditions.

Both Deutsche Bank and Macquarie Private Portfolio Management successfully managed portfolio risk. Vanguard, which as a passive strategy makes no attempt to manage risk, contributed most to the portfolio’s overall risk and portfolio losses.

Having reviewed each manager's portfolio, investment style, and risk management controls, we see no reason to doubt Deutsche Bank and Macquarie PPM’s ability to add value to The Foundation's investment strategy. We do have some reservations over Vanguard's High Yield Fund given issues of market concentration, in particular, the banking sector.

For the 2016 Financial Year, the Foundation’s investment portfolio recorded a loss of approximately $520,000 (1.02%), with disbursements and expenses producing a reduction in total assets (including receivables) of approximately $3.0 million.

All external investment advisers underperformed their benchmarks over the year. While not ideal, returns were still within range of their asset-weighted benchmark. This should be viewed as a relatively satisfactory outcome given very challenging investment conditions.

Both Deutsche Bank and Macquarie Private Portfolio Management successfully managed portfolio risk. Vanguard, which as a passive strategy makes no attempt to manage risk, contributed most to the portfolio’s overall risk and portfolio losses.

Having reviewed each manager's portfolio, investment style, and risk management controls, we see no reason to doubt Deutsche Bank and Macquarie PPM’s ability to add value to The Foundation's investment strategy. We do have some reservations over Vanguard's High Yield Fund given issues of market concentration, in particular, the banking sector.

|

|