The Foundation has an investment return target of 5% p.a. income, plus capital growth of CPI plus 1% over rolling 5-year periods. To achieve this objective a ‘high growth’ strategy has been adopted, with up to 85% allocated toward growth assets and 15% of defensive and fixed-income assets. Included in this defensive exposure is cash equivalent to one year’s projected distributions plus six months’ operating expenses. The Foundation accepts that a negative return is likely to occur on average one in every five years.

Although these return objectives have been appropriate and achievable for The Foundation in past years, in an investment climate defined by low inflation, extremely low-interest rates and a generally dour economic outlook, the race to meet these targets may inadvertently expose the Foundation to risks it is neither prepared for nor capable of handling.

One such risk is the mismatch between the Foundation's risk tolerance and 5% income target. While a 5% target makes sense (4% distributions plus ~1% operating expenses), it can result in portfolio managers chasing yield when interest rates are low while dedicating less of the portfolio toward income-oriented assets in times of high-interest rates. The consequence is a portfolio can become heavily exposed to interest rate risk when rates are low (the riskiest time to be exposed to interest rate risk) and underweight yield-oriented assets when they present the greatest opportunity. A related concern is the portfolio's heavy exposure toward Australian banks which, though offering exceptional dividend yields, are experiencing substantial headwinds to credit/earnings growth.

One such risk is the mismatch between the Foundation's risk tolerance and 5% income target. While a 5% target makes sense (4% distributions plus ~1% operating expenses), it can result in portfolio managers chasing yield when interest rates are low while dedicating less of the portfolio toward income-oriented assets in times of high-interest rates. The consequence is a portfolio can become heavily exposed to interest rate risk when rates are low (the riskiest time to be exposed to interest rate risk) and underweight yield-oriented assets when they present the greatest opportunity. A related concern is the portfolio's heavy exposure toward Australian banks which, though offering exceptional dividend yields, are experiencing substantial headwinds to credit/earnings growth.

|

|

|

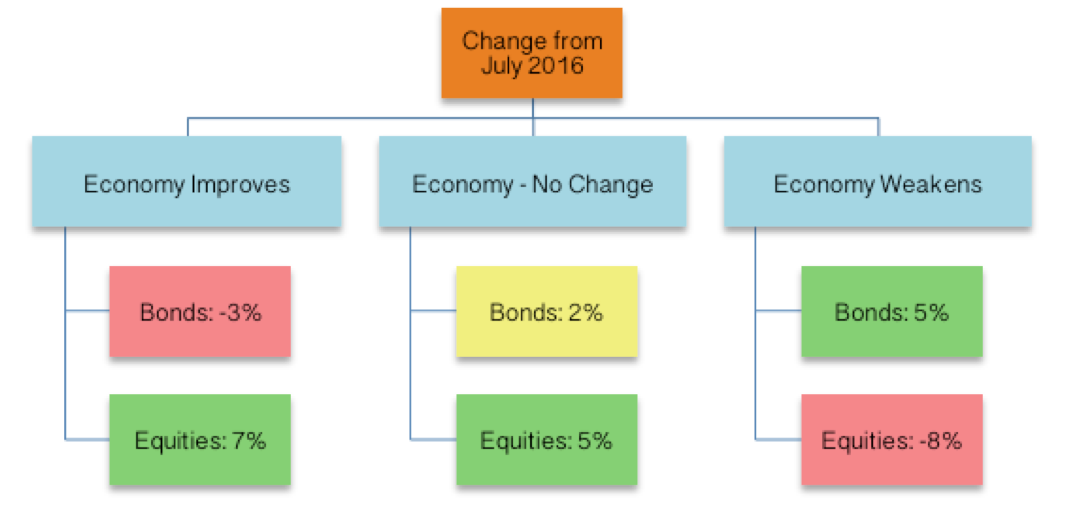

We also consider asset valuations to present a significant mid-term risk. While we accept there is little real value in comparing current valuations to historic norms, as investors adapt to the “lower for longer” hypothesis, markets appear to be overlooking (or just ignoring) the full extent of economic uncertainty and risk. This is not only evident in bond markets, where today close to $12 trillion in debt is held on a negative real yield, but also in equity and property prices that reflect expectations of stable (though relatively low), uninterrupted, earnings growth. It’s a situation where either bond or equity investors will be proven to be correct. There is a very, very fine crossover point at which they both win. The likelihood of economic growth and inflation hitting this sweet spot seems increasingly unlikely.

This leaves us with a situation whereby if economic conditions deteriorate further, market uncertainty and asset risk premiums should rise; or economic conditions improve, in which case equity prices may see a small improvement but bond prices are likely to crash.

While the Foundation's investment managers are capable of managing these risks, they must be afforded sufficient flexibility (both in the mandate, targets, and timeframe) with which to design, implement and manage their investment strategy.

On consideration of the present economic and market climate, as well as The Foundation’s long-term objectives and risk tolerance, we recommend a revision of investment guidelines and a temporary reduction in exposure to risk assets.

On consideration of the present economic and market climate, as well as The Foundation’s long-term objectives and risk tolerance, we recommend a revision of investment guidelines and a temporary reduction in exposure to risk assets.

Reducing Risk – an example

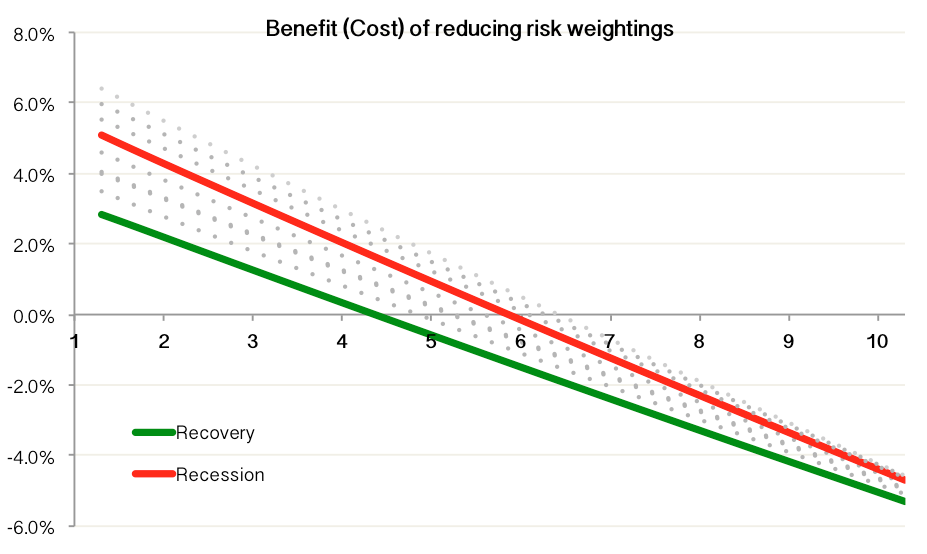

To provide an example as to how a temporary reduction in risk may assist The Foundation in meeting their long-term risk and return objectives, we offer a comparison of the Foundation's existing strategy against an alternative where risk assets are reduced by 20% (to 65% of the portfolio), and proceeds are reallocated to a diversified, low-risk short-duration portfolio of AAA Bonds and Term Deposits. At current rates, we could expect to achieve a yield of approximately 2.38% (after costs).

Comparing these two portfolios under a range of different scenarios allows us to see the effect on returns. As the chart below illustrates, if a change in economic conditions or risk premiums occur in the next 4 – 5 years, we would expect a superior result from the lower-risk portfolio. If we see no change over this time the existing strategy (~85% growth assets) will probably outperform.

To provide an example as to how a temporary reduction in risk may assist The Foundation in meeting their long-term risk and return objectives, we offer a comparison of the Foundation's existing strategy against an alternative where risk assets are reduced by 20% (to 65% of the portfolio), and proceeds are reallocated to a diversified, low-risk short-duration portfolio of AAA Bonds and Term Deposits. At current rates, we could expect to achieve a yield of approximately 2.38% (after costs).

Comparing these two portfolios under a range of different scenarios allows us to see the effect on returns. As the chart below illustrates, if a change in economic conditions or risk premiums occur in the next 4 – 5 years, we would expect a superior result from the lower-risk portfolio. If we see no change over this time the existing strategy (~85% growth assets) will probably outperform.

Of course, it stands to reason that a higher allocation to risk assets will outperform a portfolio heavy in defensive, low-risk assets over the long-term (15 years+). Though these rules also apply to The Foundation's investment strategy, we must also consider that sequencing risk is an issue; that is to say that the timing of returns and withdrawals has an impact on the sustainability of the portfolio.

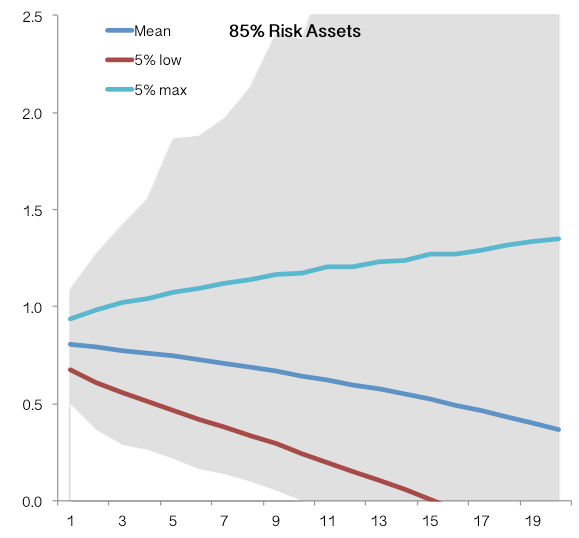

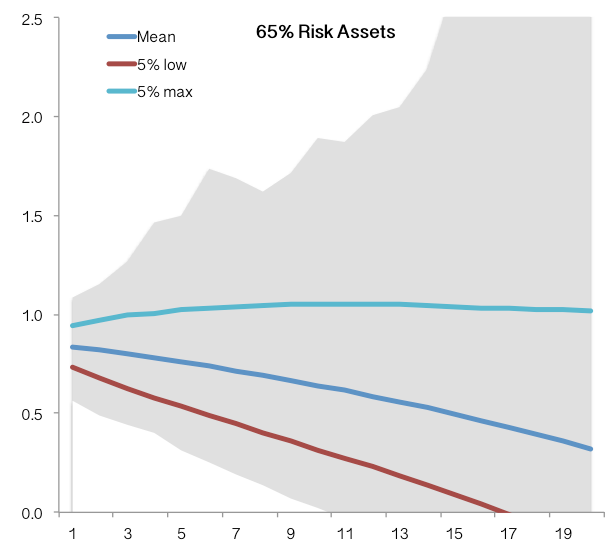

To understand the impact of cash flows we can compare the two portfolios, based on current Foundation overheads and disbursement guidelines. Over a large number of simulations[1], we see that the higher risk strategy does indeed produce a higher average (mean) result but with a wider range of results.

To understand the impact of cash flows we can compare the two portfolios, based on current Foundation overheads and disbursement guidelines. Over a large number of simulations[1], we see that the higher risk strategy does indeed produce a higher average (mean) result but with a wider range of results.

|

|

However it’s interesting to note how similar the results are. The first point is that both portfolios see a gradual decline in the real (inflation-adjusted) value of the portfolio, indicating that if returns are in fact "lower for longer" The Foundation will struggle to maintain the real value of its corpus, let alone consistently meet a CPI+6% target. We conclude that making a temporary change to risk allocations is unlikely to have a significant impact on the value of the corpus.

In other words:

In other words:

- If returns are indeed “lower for longer”, a reduced risk strategy will have minimal impact on overall returns.

- If economic conditions strengthen, overall returns under both strategies will be better, just slightly less so with the lower-risk strategy.

- If economic conditions deteriorate or markets become more nervous, lower risk strategy will be less adversely impacted and will have additional capital available to re-deploy at a higher rate of return.

To measure the "cost" of a lower risk strategy we need only compare the difference in outcomes under each of these scenarios. From this we see that over a five-year period, in an environment of stable pricing and moderate earnings growth, the lower-risk portfolio would be expected to underperform by approximately $2 million. Over 7 years the cost increases to around $3 million.

This cost can be compared to an insurance policy on the portfolio, with $2 million (in deprived returns) providing the Foundation with roughly $10 million (20%) of capital that can be redeployed as opportunities arise at any time within the next 5 years.

This cost can be compared to an insurance policy on the portfolio, with $2 million (in deprived returns) providing the Foundation with roughly $10 million (20%) of capital that can be redeployed as opportunities arise at any time within the next 5 years.

Summary

In the past, the Jack Brockhoff Foundation has sought to meet its obligations and grow the corpus by pursuing a total return target of CPI+6% (comprising 5% income and capital growth of CPI+1% over rolling 5-year periods).

Though these targets have been both reasonable and achievable in past years, maintaining this return objective in the current climate of low inflation and extremely low-interest rates may inadvertently expose the Foundation to an unacceptable – and unnecessary – level of investment risk.

These risks are not only limited to systematic risk and interest rate risk but also risks due to portfolio inefficiencies caused by portfolio managers hunting for yield in an effort to meet a 5% income target.

On consideration of the Foundation's risk tolerance and return objectives and investment conditions, we recommend that a temporary adjustment be made to the Foundation's return and asset allocation targets.

In the past, the Jack Brockhoff Foundation has sought to meet its obligations and grow the corpus by pursuing a total return target of CPI+6% (comprising 5% income and capital growth of CPI+1% over rolling 5-year periods).

Though these targets have been both reasonable and achievable in past years, maintaining this return objective in the current climate of low inflation and extremely low-interest rates may inadvertently expose the Foundation to an unacceptable – and unnecessary – level of investment risk.

These risks are not only limited to systematic risk and interest rate risk but also risks due to portfolio inefficiencies caused by portfolio managers hunting for yield in an effort to meet a 5% income target.

On consideration of the Foundation's risk tolerance and return objectives and investment conditions, we recommend that a temporary adjustment be made to the Foundation's return and asset allocation targets.

Important: Be aware that your other advisers will have their own opinions and assessment of current investment conditions and their ability to achieve certain risk and return targets during this time.

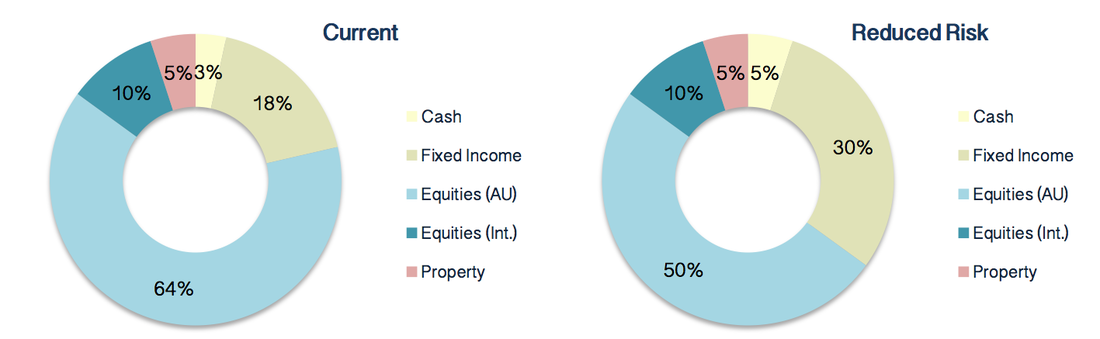

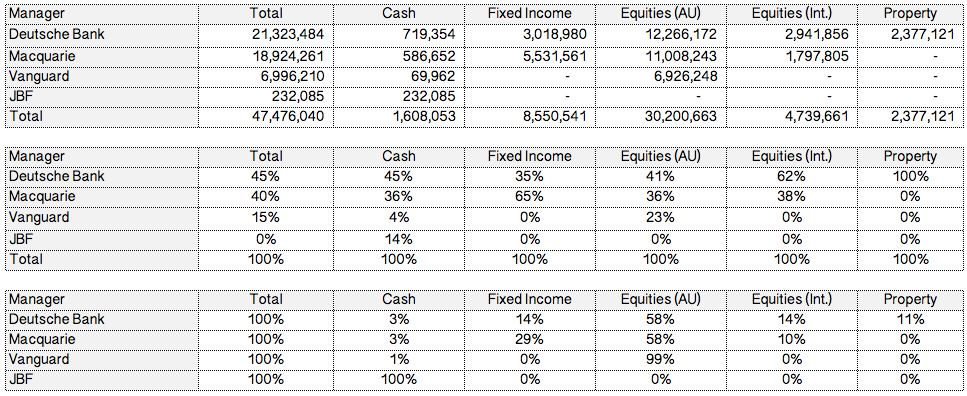

Manager & Asset Allocation (30 June 2016)

[1] Monte Carlo simulation using 20,000 independent trials (parametric, normal distribution, cash flow adjusted)