|

Business Summary

|

Metcash (MTS) is a wholesale distribution and marketing company specialising in grocery, fresh food, liquor, hardware and automotive parts and accessories. Metcash is structured as three distinct business units; their Food and Grocery businesses (IGA, Foodworks, Campbells Wholesale), Automotive and Hardware (Mitre 10, Autobarn, Autopro, Midas) and Liquor (IGA Liquor, Bottle-O, Cellarbrations). Together they account for roughly $13 billion in annual sales, with 2/3 of this coming from their groceries division.

|

|

Business Conditions and Strategy

|

Over recent years Metcash has developed a somewhat unfavourable reputation among analysts for their fragmented and seemingly disorganised approach to retaining market share, with an overriding emphasis on developing their franchise "footprint" through expansion of existing stores and acquisition of liquor distribution businesses.

Of course with the benefit of hindsight it's clear to see that this was the wrong approach. EBIT margins within their food and grocery division are less than half those of their key competitors (Coles, Woolworths and Aldi), while they attempted to prop up margins by aggressively buying-up liquor distribution franchises throughout NSW, Queensland and Victoria. |

|

The good news (for some)

|

Last week's shock announcement that they were going to write $640 million off the value of their assets ($507 m against intangibles) and suspend dividends for 18 months has hit investor confidence hard. Though I'm not really sure why. After all, their earnings growth has been weak and the carrying value of their goodwill was outdated and exaggerated. As for the decision to suspend dividends, well this was clearly the most prudent approach for management given that their leverage is about to jump up a few pegs. But, as they say, a dividend in the hand is worth two reinvested. So that partly explains why the share price has taken a hit, which is bad news for existing investors, but for those of us sitting on the sidelines (and with a bit of patience) it provides an opportunity. Here's why.

|

|

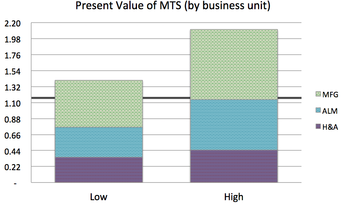

Valuation

|

In valuing MTS as an entire business unit it's tempting to revert back to management estimates of earnings. Although there are some positive signs of improvement - both in terms of earnings and management responsibility and direction - the company still has some significant challenges ahead. As such we have erred heavily on the side of caution.

As MTS's Hardware and Automotive businesses essentially operate independently to their groceries and liquor businesses, we value this business unit separately. Given the prospect of divestiture, we conservatively value this business at an enterprise value in excess of $300 million, or $0.35 per share. For their food and grocery (MFG) and liquor (ALM) divisions we don't expect to see any great reversal of fortune for some time. While this may be an overly pessimistic assessment of their ability to manage market market expectations, their current sales growth initiatives seem to be consuming a relatively large amount of CAPEX for relatively small improvements in sales. Furthermore their strategy to compete on price seems to place undue pressure on profit margins. Despite this, so long as management doesn't do anything too stupid, Metcash's ALM and MFG businesses are worth well in excess of $1.5 billion (~$0.90 per share). In fact even if they did, it's hard to justify an enterprise value of less than $1.25 billion (~$0.63 per share). Of course this leaves us with considerable upside should they achieve their objectives. Time will tell. For investors a key consideration for this type of investment is time. Patience is often required for value to be realised, and for companies like Metcash, which has fairly consistently disappointed shareholders for the past 10 years or so, it's likely to take several years to recover. We expect that some time in the next, say, 4 or 5 years, value will be extracted from the company. It's also important to note that full year results will be released next week (15 June) which could sway the market either way, however if history is any guide then preparing the market for such a significant (but overdue) write-down could be a sign that management is ready to leave some of their disappointing legacy behind and focus on the future. |

|

Summary

|

Risk: Medium/High

Target holding period: 4 years Target price: $1.78 plus dividends of $0.58. Current price: $1.102* Annual Return: 20.97% *6 June 2015 |

|

Disclaimer

|

Disclaimer: The information and opinions provided below are provided as general information only and is not to be interpreted as personal advice. Forecasts are based on extracts from independent analysis carried out by Third Sector Advantage (TSA). We recommend conducting your own research and consulting with your adviser prior to making any investment decision.

|

|

Update

|

Shortly after issuing the report above, Burson purchased Metcash's automotive division for $275 million. While this price was below the price tag of $300 million we estimated, it was still welcomed by the market as a way to strengthen MTS's balance sheet and fund enhancements to their core business segments. Over the year the roll-out of Metcash's MFG improvement program also showed some signs of success. Whether this translates to real, meaningful improvement to the bottom line is something we won't know for several years.

In February 2016, only 8 months after our purchase at $1.10-$1.12 per share, MTS broke through $1.80 per share. This came at a time where the ASX200 was suffering, and with (what we thought were) more attractive opportunties available, over the next month we sold ~30% of our shareholdings at an average price of $1.74. We sold our remaining shareholdings in the second half of June 2016, shortly after qualifying for the CGT discount (holding>12 months), at an average price of $1.88. Although MTS has continued to perform well, reaching a high of $2.28, we believe the "easy gains" have been had and the current price understates the challenges ahead. Though unlikely to happen, we may consider purchasing MTS again at a price below $1.30, until then we see insufficient margin of safety to justify making another purchase of the company. Average entry: $1.11 Average exit: $1.83 Gross return*: 64.6% Benchmark (ASX200) Gross Return*: -7.90% Relative performance: +73.5% After tax return Tax Assessable gain: $0.46 per share Net Return at MTR 37%: +49.5% *MWR |