18 June 2015

|

Greece: good money after bad?

As you may have heard, the worst-kept secret in financial markets is out. Greece can't afford to meet their interest repayments. Not this month's payment. Not next month's payment. And in all likelihood not next year's payments. Worse still, even if they could, it's unlikely they would.

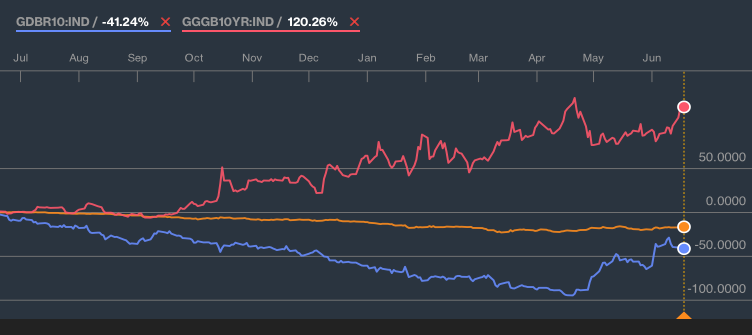

Welcome to 2015 under the rule of Alexis Tsipras, Greece's Prime Minister and leader of the "anti-austerity" Syriza party. In a nutshell, the Syriza party (which was carved our of the KKE, the communist party of Greece) was formed in response to the heavy-handed post-GFC sanctions and austerity measures driven into them as a condition of a last-minute bailout by the International Monetary Fund (IMF), European Central Bank (ECB) and European Union (EU). Now, whether or not the conditions of the loan imposed on Greece were fair is one issue, but refusing to make your debt repayments simply because that's what the people elected you for is an entirely different matter. Especially when you've borrowed around €84 billion from them (and all they were asking for was €1.55 in overdue interest). But the problem here is one of scale. Quite simply the scale of debt relative to Greece's economic production is so large that while they may have been able to keep their creditors at the gate for another month or two it would come at the expense of their domestic budgetary commitments. Not surprisingly the yield on 10 year Greek Bonds have soared since his Tspiras' election, from around 6% to over 13% today. To put that into perspective, German 10 year Bunds are trading on a yield of around 0.8%.

Source: Bloomberg

Change in Yield - 10yr German Bunds (blue) and 10yr Greek Bonds (red). Equivalent to a return of +70% and -55% respectively. Source: Bloomberg

A matter of scale

As you would expect, Greece's bullheadedness isn't making them any friends and has the European Union weighing up whether to just cut their losses and kick them out of the EU (or, as the media tend to refer to it, a "Grexit"). For the moment the EU seem to be holding their cards very close to their chest, however early signs suggest a further (even if reluctant) extension to Greece's credit facility.

While it's always a risk to read too much into the data and talk about what the fallout of a Grexit may be, it seems that the most probable outcome is for the EU to continue to support Greece, if for no other reason than to avoid disruption the economic recovery and confidence of the EU's key members. In fact as much as Greece is a thorn in the EU's side, in relative economic terms the Greek debt crisis is more a story about confidence than dollars (or Euros). Collectively the EU's 28 member countries generate over €14,000 billion in GDP annually (of which less than 2% is attributable to Greece), with this figure growing at well in excess of 1% per annum. As interest rates among their largest members sit at close to zero (0.05% in Germany and France, 0.5% in UK) the actual cost to fund the bail-out is fairly insignificant when we consider the alternative. The counter-argument to this is that Greece has just become a real pain to deal with. While Syrzia's antics are frustrating, Greek politics is dominated by a coalition of "anti-bailout" and "anti-austerity" communists and socialists. Continuing to fund their ailing economy could just be putting good money after bad, and ultimately slow the EU's progress. Investment Opportunties

As investors these conditions present a number of opportunities. For starters, if the EU continues to fund Greece it's likely we will see risk premiums fall, while rising interest rates in the US will accelerate the decline in Greece's global risk premium, causing yields to fall and Greek Bond prices to rise. This scenario could easily provide 100%-plus returns over the next two to three years. The risk (and it is a very real risk) is you may never see your money again.

Another option might be to buy into Greece's recovery through broad investment into their stock market (Athens Stock Exchange - ASE - last traded 684). In my opinion the problem with this approach is that a large proportion of the main indices are held by banks, construction companies and utilities. Current economic conditions, in particular low credit growth, deflation and very high unemployment are not supportive of these industries. All the worse if the EU kick them out. In our opinion both these options are risky. Sure, they're exciting, but for the risk we don't really see how they benefit us as investors. After all, Greece only makes up around 0.3% of global GDP (Australia is a touch over 2%). From this perspective we believe the real opportunity in the numbers is in exploiting market uncertainty, particularly when that uncertainty is carried through to largely unrelated and independently strong markets such as Germany, UK, France and Spain. For investors with a long-term investment horizon we favour unhedged exposure to the Euro (€1 currently trades at AUD$1.46, USD$1.13).

Source: Bloomberg

Outcome for investors

On an absolute return basis Europe still provides some good investment prospects for long-term investors, and now appears to provide more favourable investment conditions than North America and Australia.

As with our domestic equities portfolio, our preferred approach within these markets is to adopt a strategy of buying assets with strong free cash flow, modest gearing, inflation resistant earnings and a book value supported by a high level of tangible assets. While we are not strictly "contrarian" investors, our approach will often result in us gravitating toward "unattractive" companies, sectors or asset classes. Renewed confidence throughout Europe's economic powerhouses (Germany in particular) has made it far more difficult to find major valuation flaws, however it should be noted that we have achieved a significantly better return on these same recovery themes through our heavy tilt toward North America (unhedged). Some of the sectors that we still see further significant upside include commodities (oil producers in particular) and infrastructure services. |

|

Market Stats (current at time of writing)

US Treasury 10yr: 2.31% German Bund 10yr: 0.808% Greek Bond 10yr: 13.12% Australian Treasury 10yr: 2.84% AUD/EUR 0.68 AUD/USD 0.78 Athens Stock Exchange: 684 DAX (Germany): 10,978 S&P500: 2,100 All Ordinaries (XAO): 5,590 |