Review of the Research

To gain a better understanding of the likely impact from adopting an ethical screening process on The Foundation's portfolio we undertook a review of the significant body of research on the subject, followed by a more detailed attribution analysis of dedicated Australian SRI Funds over recent years.

Empirical Evidence

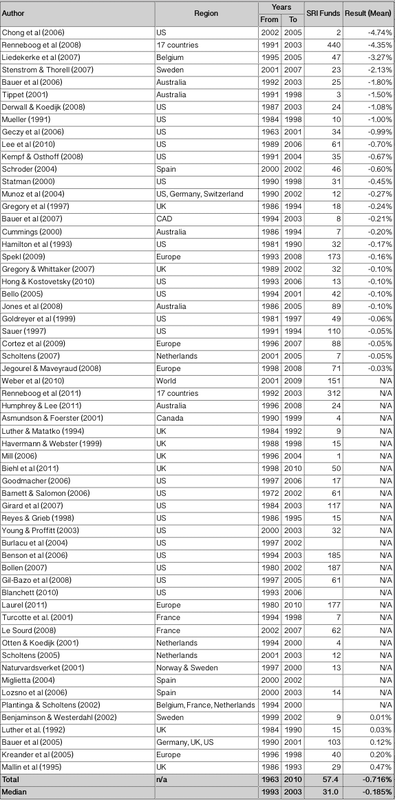

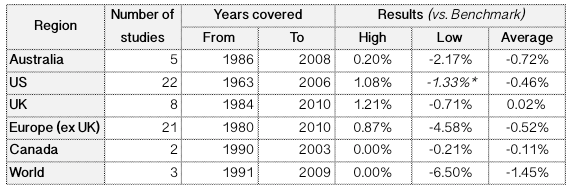

A total of 61 research papers were reviewed, covering over 3,000 SRI-screened Funds between 1963 and 2010. From this review we make a number of observations.

- Of the studies that quantified the difference in returns between SRI and non-SRI-filtered Funds, we find that SRI Funds tend to underperform by around 0.72% per annum. If we include the studies that find no discernible difference in return, the average drag on returns is 0.37%.

- The drag on returns appears to be less pronounced in developed markets.

- In practice, SRI Funds tend to perform much worse than expected by a simple, passive market portfolio with ineligible (non-SRI) securities removed.

- Although we would expect a SRI filter to increase portfolio volatility, a natural consequence from the reduction of eligible securities, we actually find that over a market cycle volatility is reduced.

- Research has found that SRI strategies tend to slightly outperform in periods of crisis (Nofsinger & Varma, 2013)

- Despite only a relatively modest proportion of securities being deemed ineligible for investment by SRI Funds, there tends to be a much higher-than-expected increase in portfolio volatility.

- The return profile of SRI Funds tend to exhibit a negative skew.

- SRI Funds share a very unstable correlation with the broader market.

Summary of Research Papers (High, Low and Average Result)

|

*Adjusted for outliers

|

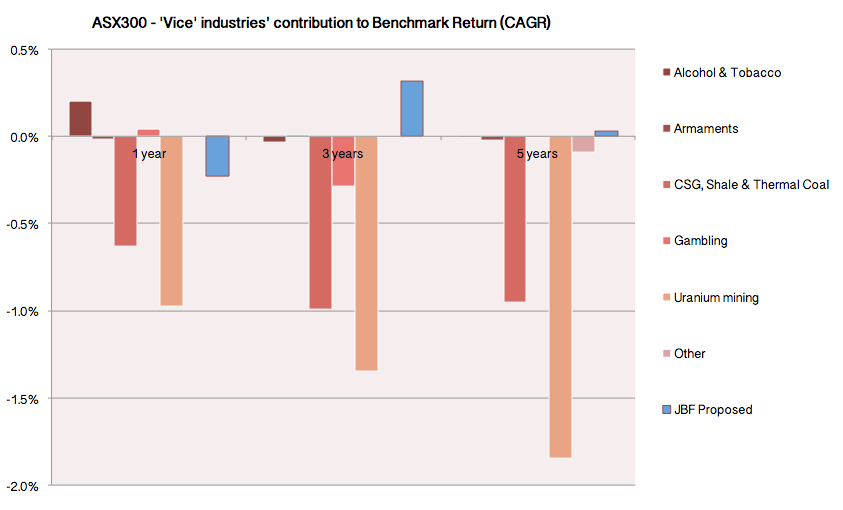

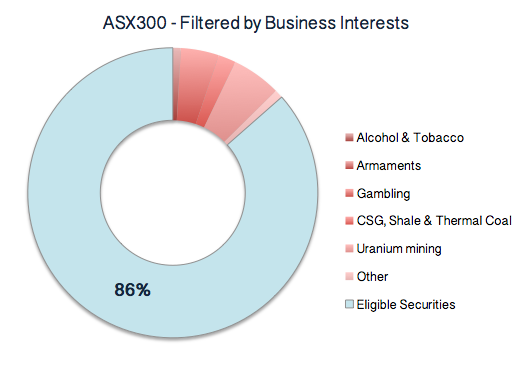

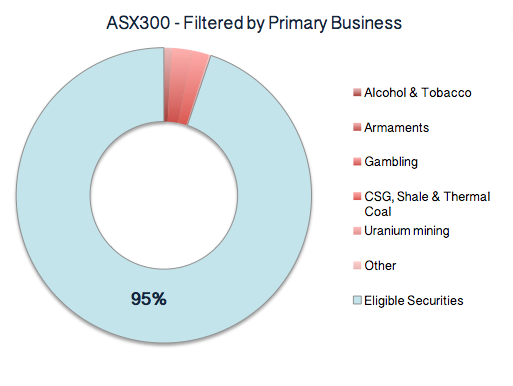

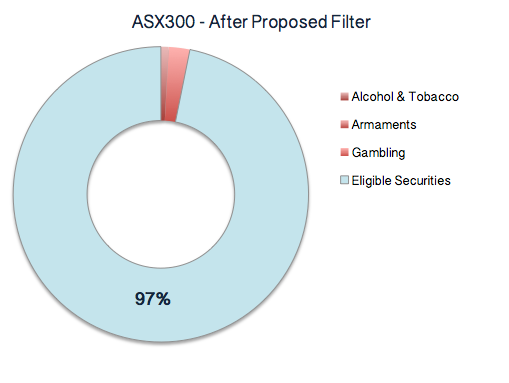

Effect of ESG Filters on Investment Universe (Australia)

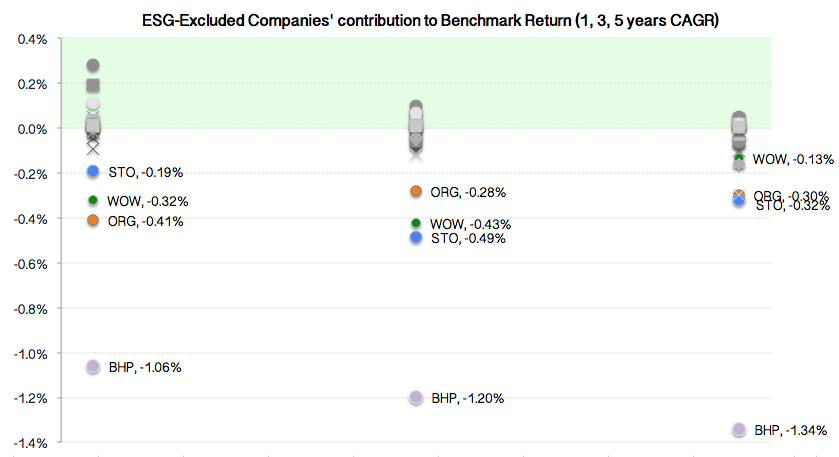

The majority of SRI Fund outperformance can be attributed to their exclusion of BHP, Origin Energy, Santos and Woolworths. Investors should consider this when assessing the recent (past 5 years) performance of SRI Funds.

|

|

|

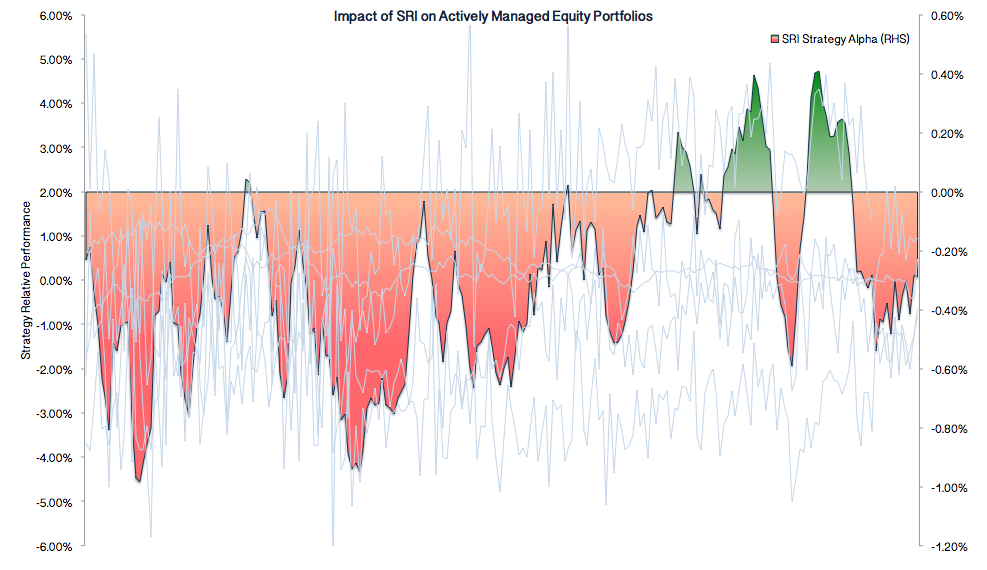

Despite the expectation of SRI Funds outperforming their peers in recent years, this does not appear to have been the experience for most investors. Where SRI Funds are run alongside an unconstrained strategy, they have underperformed in over 90% of trading periods. The average underperformance is equivalent to 0.360% per annum (CAGR).