Ethically Screening Investments: impact on Foundation's Objectives

The question has been raised as to whether an ethical screen can be implemented without substantial impact on the income or maintenance of capital value.

To answer this question requires careful consideration of a number of factors, and raises further questions including:

- What type of companies or business activities are to be avoided?

- For companies with multiple businesses, what level of exposure to 'non-ethical' practices/operations is permissible?

- Are assets to be screened using a 'negative' or 'positive' process?

- How is this change in approach likely to affect returns?

- How is portfolio volatility likely to be affected?

- What are the qualitative advantages from this approach?

- Who is responsible for ensuring compliance with the change in strategy?

To help answer these questions our analysis has encompassed not only a review of the existing literature on the subject of ethical investing, but also a detailed attribution analysis of the Australian equity market and SRI-mandated equity funds. The objective here is to explore the key drivers of market returns and to establish what if any effect an ethical screen is likely to have on The Foundation's ability to fulfil it's primary return <and social> objectives.

Please note the for brevity we refer to ethical screen and Funds using the acronym SRI (Socially Responsible Investment). This term can be used interchangeably with ESG (Environmental, Social and Governance). SRI is sometimes also used to abbreviate 'Sustainable and Responsible Investment; whichever term is used >>> they mean the same thing.>>>

Please note the for brevity we refer to ethical screen and Funds using the acronym SRI (Socially Responsible Investment). This term can be used interchangeably with ESG (Environmental, Social and Governance). SRI is sometimes also used to abbreviate 'Sustainable and Responsible Investment; whichever term is used >>> they mean the same thing.>>>

Socially Responsible Investment (SRI): Review of the Research

|

To better understand the likely impact from adopting an ethical screening process we undertook a review of the already significant body of research on the subject.

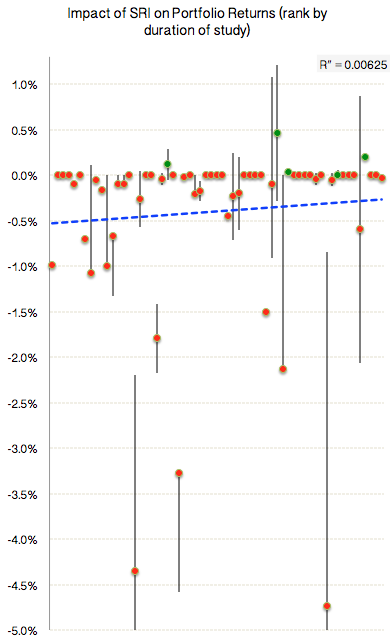

Across a total of 61 research papers covering 3,000 SRI-screened funds across nearly 50 years we found that applying an ethical filter to portfolio selection produced an average drag on returns of approximately 0.37%, with a significant negative skew, though portfolio volatility also tended to be lower. We also found that compared to the market benchmark SRI Funds did tend to have moments of outperformance, particularly in periods of crisis. While its tempting to think this is due to the relative robustness and resilience of companies with a highly developed ethical profile, we should bear in mind that unconstrained active managers also tend to outperform in times of crisis (usually with greater success). This leads us to the observation that unconstrained actively managed portfolios outperform SRI Funds in both times of crisis and normal markets, with analysis of these differences leading us to conclude that SRI-focused Funds tend to underperform their unconstrained peers by approximately 0.2% per annum. Summary A review of the empirical evidence suggests that implementing a SRI filter tends to reduce returns on equity portfolios by an average of between 0.2% - 0.4% per annum. Against The Jack Brockhoff Foundation's portfolio ($47.5 million) this is equivalent to a reduction in investment earnings of $70,000 to $140,000 per annum. A full discussion of our research findings can be found here. |

|

NNNXXX

In summary, the evidence seems to support the notion that SRI portfolios under-perform on an absolute-returns basis, but with less exposure to market risk and volatility than conventional portfolios the risk adjusted return appears the same.

Consideration must be absolute total returns. Focusing too much on risk-adjusted returns when The Foundation's long-run minimum return requirement is so high is dangerous.

NXXXX

In summary, the evidence seems to support the notion that SRI portfolios under-perform on an absolute-returns basis, but with less exposure to market risk and volatility than conventional portfolios the risk adjusted return appears the same.

Consideration must be absolute total returns. Focusing too much on risk-adjusted returns when The Foundation's long-run minimum return requirement is so high is dangerous.

NXXXX

Impact on Lost opportunities

|

One of the few assumptions we can make about SRI mandates is that all else being equal they should not be able to outperform an unconstrained investor. This is because by excluding the depth and breadth of investment opportunities available.

To better understand the relationship between ethical filters and subsequent performance we performed a regression analysis securities from the ASX300 excluded by SRI filters, then comparing their performance over time relative to the benchmark portfolio. From these results we were able to estimate the impact on returns from reducing the number of investment opportunities available to an investment manager. For the Australian share market over the period studied we found that the drag on equity portfolio returns to be between 0.18% and 0.21% per annum (equivalent to $63,000 to $74,000 per annum on The Foundation's $35 million equity portfolio). Summary Analysis of equity market returns using three different SRI filter techniques found that the impact of returns is greatly influenced by the parameters used to exclude stock from managers' opportunity set. For the data we collected we arrive at the conclusion that implementing a SRI screen to The Foundation's investment strategy is likely to cost (through lost returns) between $63,000 and $74,000 per annum. However when we seek to measure this variance we see stark differences in results depending on the period of time and country analysed. To explain these differences we can look to the returns from the companies excluded by SRI mandates. For example, were we to look at US SRI Funds we might notice that over the past 20 years tobacco companies have delivered shareholders roughly twice the rate of return than the broader share market, despite underperforming during market crises, such as in 2000 and 2008-09. A similar result of outperformance can be observed with defence contractors. Though this suggests that companies excluded by SRI mandates outperform, the evidence supporting this is weak. Part of the problem is there are relatively few investment managers who (publicly, at least) actively pursue companies that are involved in contentious sectors or practices. Of those that do exist without doubt the most famous of these the Barrier Fund, formerly called the Vice Fund. While the Fund's chief strategy mandate is to target companies with high barriers to entry, it takes the view that: "tobacco, alcohol, gaming and weapons/defense companies...tend to thrive regardless of the economy as a whole". Fund has slightly underperformed the market (7.38% vs S&P500 7.49%), though with a relatively substantially reduced correlation with market (beta 0.85). <<CLEAN THIS UP: Move to full research section?>>> The degree to which investment opportunities are restricted really depends on how strict The Foundation Looking at the ASX300, for example, we found that specifying the properties which deem a company ineligible for investment makes a substantial impact on the opportunities available to the investment manager. For example:

|

|

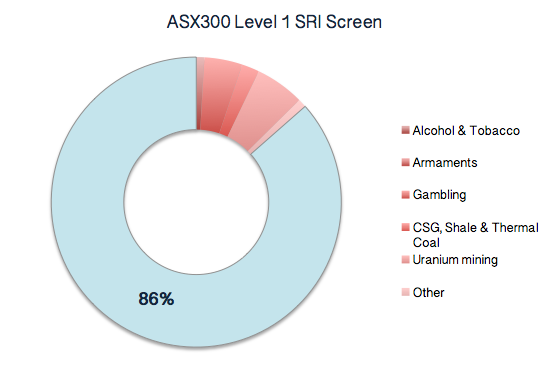

Within the ASX300 (largest 300 companies on the Australian Stock Exchange) as of 30 June 2016 there were 31 companies which derived more than 5% of their revenues from business activities which contravened SRI guidelines. Together these companies accounted for a total market capitalisation of approximately $220 billion. This represents 10.3% of the companies and 14.3% of total market capitalisation represented by the ASX300. Of stock excluded by SRI filters, more than half the market capitalisation comes from just three companies: BHP, Woolworths and Rio Tinto.

One of the few assumptions we can make about SRI mandates (and indeed any other mandate that limits opportunities) is that all else being equal they should not be able to outperform an unconstrained investor. However when we seek to measure this variance we see stark differences in results depending on the period of time and country analysed.

To explain these differences we can look to the returns from the companies excluded by SRI mandates. For example, were we to look at US SRI Funds we might notice that over the past 20 years tobacco companies have delivered shareholders roughly twice the rate of return than the broader share market, despite underperforming during market crises, such as in 2000 and 2008-09. A similar result of outperformance can be observed with defence contractors.

Though this suggests that companies excluded by SRI mandates outperform, the evidence supporting this is weak. Part of the problem is there are relatively few investment managers who (publicly, at least) actively pursue companies that are involved in contentious sectors or practices.

Of those that do exist without doubt the most famous of these the Barrier Fund, formerly called the Vice Fund. While the Fund's chief strategy mandate is to target companies with high barriers to entry, it takes the view that: "tobacco, alcohol, gaming and weapons/defense companies...tend to thrive regardless of the economy as a whole". Fund has slightly underperformed the market (7.38% vs S&P500 7.49%), though with a relatively substantially reduced correlation with market (beta 0.85).

<<CLEAN THIS UP: Move to full research section?>>>

To explain these differences we can look to the returns from the companies excluded by SRI mandates. For example, were we to look at US SRI Funds we might notice that over the past 20 years tobacco companies have delivered shareholders roughly twice the rate of return than the broader share market, despite underperforming during market crises, such as in 2000 and 2008-09. A similar result of outperformance can be observed with defence contractors.

Though this suggests that companies excluded by SRI mandates outperform, the evidence supporting this is weak. Part of the problem is there are relatively few investment managers who (publicly, at least) actively pursue companies that are involved in contentious sectors or practices.

Of those that do exist without doubt the most famous of these the Barrier Fund, formerly called the Vice Fund. While the Fund's chief strategy mandate is to target companies with high barriers to entry, it takes the view that: "tobacco, alcohol, gaming and weapons/defense companies...tend to thrive regardless of the economy as a whole". Fund has slightly underperformed the market (7.38% vs S&P500 7.49%), though with a relatively substantially reduced correlation with market (beta 0.85).

<<CLEAN THIS UP: Move to full research section?>>>

Determining the impact that an 'ethical' overlay or filter will have on The Foundation's objectives and outcomes requires careful consideration not only on the quantitative changes (return and risk), but also practical considerations such as defining what properties or characteristics deem an asset unsuitable for investment and how this can be implemented and monitored.

Indeed a starting point of for this conversation should start by defining the parameters of what is - or more so, what isn't - considered an eligible security under a SRI-focused strategy. As I understand the Directors have suggested applying a broad exclusion for stock of companies "primarily involved with tobacco, alcohol, gaming and armaments".

It should be noted that applying the filter based upon a company's primary business activity is a far less strict definition than is commonly used by the industry. In discussions with Fund managers, consultants and researchers who work in this space, consensus pointed to a threshold of "no more than 5%" being fairly normal. The consequence of having a less strict filter is it will be easier to manage (fewer excluded securities), lower change of breaching The Foundation's guidelines.

a lower chance of inadvertently breaching The Foundation's ethical

The consequence of having a less strict threshold is that The Foundation, if an ethical filter was adopted, would be less likely to inadvertently breach

*Moving to more standardised filter/monitoring : EIRIS, CAER

Bearing in mind that in most cases our investment universe comprises listed secondary market securities, it would be reasonable to make the assumption that all assets should be relatively fairly priced. In other words there shouldn't be a reason for 'ethical' companies to trade at a higher or lower risk premium than 'unethical' companies.

In both our review of the existing research and own analysis we found that applying SRI filters to equity investment strategies produces a drag on returns of approximately 0.36%.

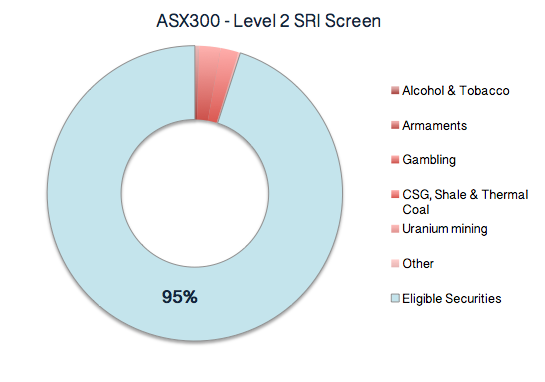

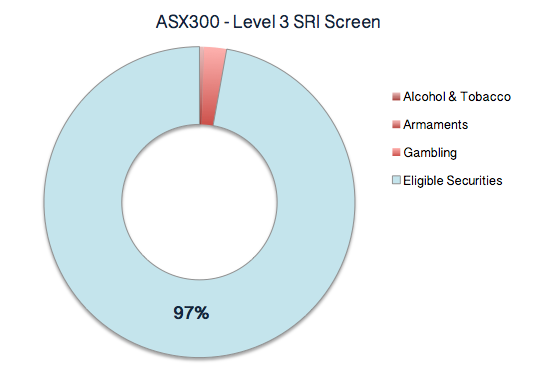

*with a less strict filter many "excluded" companies are still investable; universe reduced by only 3% (97% of securities in ASX300 still investable). The filter most Australian equity SRI Funds use reduces their investment universe by nearly 15%. Ethical filter impact on Australian equity returns ~ 0.10%

*Impact on global equity funds ~ 0.36%

*Impact on total portfolio: approx. $47,000 per annum (0.10%)

SRI portfolios tend to underperform

*

*

Indeed a starting point of for this conversation should start by defining the parameters of what is - or more so, what isn't - considered an eligible security under a SRI-focused strategy. As I understand the Directors have suggested applying a broad exclusion for stock of companies "primarily involved with tobacco, alcohol, gaming and armaments".

It should be noted that applying the filter based upon a company's primary business activity is a far less strict definition than is commonly used by the industry. In discussions with Fund managers, consultants and researchers who work in this space, consensus pointed to a threshold of "no more than 5%" being fairly normal. The consequence of having a less strict filter is it will be easier to manage (fewer excluded securities), lower change of breaching The Foundation's guidelines.

a lower chance of inadvertently breaching The Foundation's ethical

The consequence of having a less strict threshold is that The Foundation, if an ethical filter was adopted, would be less likely to inadvertently breach

*Moving to more standardised filter/monitoring : EIRIS, CAER

Bearing in mind that in most cases our investment universe comprises listed secondary market securities, it would be reasonable to make the assumption that all assets should be relatively fairly priced. In other words there shouldn't be a reason for 'ethical' companies to trade at a higher or lower risk premium than 'unethical' companies.

In both our review of the existing research and own analysis we found that applying SRI filters to equity investment strategies produces a drag on returns of approximately 0.36%.

*with a less strict filter many "excluded" companies are still investable; universe reduced by only 3% (97% of securities in ASX300 still investable). The filter most Australian equity SRI Funds use reduces their investment universe by nearly 15%. Ethical filter impact on Australian equity returns ~ 0.10%

*Impact on global equity funds ~ 0.36%

*Impact on total portfolio: approx. $47,000 per annum (0.10%)

SRI portfolios tend to underperform

*

*