John & Catherine Weir |

Managing the sale of AAPL Shares - 7 August 2017 |

Dear John and Cathy,

Pursuant to our discussions around your AAPL shares, and the risk presented from having such a concentrated exposure to a single company has on your overall financial position, I am pleased to present a few thoughts and comments around the ways forward to manage this risk.

Pursuant to our discussions around your AAPL shares, and the risk presented from having such a concentrated exposure to a single company has on your overall financial position, I am pleased to present a few thoughts and comments around the ways forward to manage this risk.

However, let's first review the key risks that we are trying to manage:

- Concentration Risk: If we were to estimate the value of your liquid financial assets to be approximately $2.5 million, your AAPL shares comprise 40% of this (~$1 million). Holding such a large proportion of your portfolio not only increases overall volatility of your financial situation, but also creates underlying risks to the long-term sustainability of your portfolio throughout retirement. A sudden fall in the value of AAPL shares, for example, may force you to sell at these shares or other assets at inopportune times, potentially further concentrating your exposure to the success, failure and, ultimately, market opinion of AAPL.

- Taxation: With a cost base of around $10,000, approximately 99% of the value of your shareholding is from capital gains. These unrealised capital gains, and the prospective taxation payable on these gains, represents a liability. Retaining these shares defers payment of this liability; this in itself is a good thing as it allows you to accumulate gains on the liability, however it also threatens to trigger a much greater tax liability than may be payable if this liability is managed. For example, if a forced sale was to take place today, you would be liable for capital gains tax equivalent to approximately $207,000. From a tax perspective our objective should be to manage this liability. This means that over an extended period of time (beyond what we will discuss below) you may wish to continue the sell-down process for your AAPL shares, perhaps re-purchasing them later so that the "cost base" of the shares may be re-set and the future liability is reduced.

Proposed Sell-Down

Considering the current value of your liquid financial assets, asset allocation and risk targets, and income requirements throughout retirement, I believe it is prudent to adjust your exposure to AAPL to no more than 20% of your total investment assets. Long-term, it would be ideal to have this level below 15%.

Given the risks mentioned above, plus our claim that North American equities (of which AAPL is the largest company) are now overvalued, we believe that now is a good time to be selling down. Furthermore, instead of spreading out the sales evenly across multiple years, we believe that selling more aggressively in the near term is appropriate.

With this in mind, we looked to model the impact of different orders and approaches to share sales.

Assumptions

Based on liquid Net Assets of $2.5 million, a risk budget of 70% and single-stock concentration of 25%, we estimate that an ideal AAPL exposure should be no more than $437,500, representing a $562,500 reduction in your AAPL shareholdings. Furthermore we have assumed a normalised return of 7% on your AAPL shares, with volatility of roughly 35%.

Scenarios

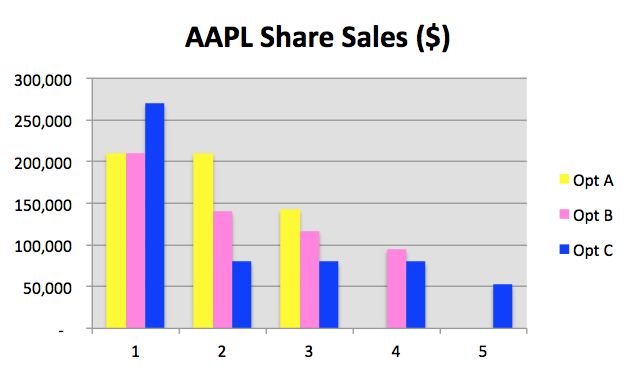

The charts below illustrate three scenarios (options).

Note on taxes - Option C

To explain my comments on headline tax vs Marginal Tax Rates we need to look understand that the "steps" between tax brackets (Marginal Tax Rates) are not smooth or even. For example, consider someone earning $90,000 per annum; they will pay tax (and Medicare) at a rate of 39% on income above $87,000, 34.5% on income between $37,000 and $86,999, and so on and so forth. In other words the "step" between these tax brackets is 4.5%. Meanwhile for someone earning $25,000, while they are in a 21% tax & Medicare bracket, their effective marginal tax rate is actually about 29%. Then we have people with assessable income below about $20,540; while they are above the tax-free threshold they don't actually pay tax. By navigating these "steps" investors are able to better understand when it might be better to pay additional tax now (i.e., stepping up 4.5% from 34.5% to 39%) so that they may "step down" (say, from 29% to 0%) in other tax periods. Don't get too caught up in the details of this, the key message is that when tax planning it pays to view it across multiple years.

Considering the current value of your liquid financial assets, asset allocation and risk targets, and income requirements throughout retirement, I believe it is prudent to adjust your exposure to AAPL to no more than 20% of your total investment assets. Long-term, it would be ideal to have this level below 15%.

Given the risks mentioned above, plus our claim that North American equities (of which AAPL is the largest company) are now overvalued, we believe that now is a good time to be selling down. Furthermore, instead of spreading out the sales evenly across multiple years, we believe that selling more aggressively in the near term is appropriate.

With this in mind, we looked to model the impact of different orders and approaches to share sales.

Assumptions

Based on liquid Net Assets of $2.5 million, a risk budget of 70% and single-stock concentration of 25%, we estimate that an ideal AAPL exposure should be no more than $437,500, representing a $562,500 reduction in your AAPL shareholdings. Furthermore we have assumed a normalised return of 7% on your AAPL shares, with volatility of roughly 35%.

Scenarios

The charts below illustrate three scenarios (options).

- Option A: Here share sales are front-loaded to across the first two years, plus a smaller sale in year three. The level of sales are designed to quickly reduce AAPL exposure while managing overall levels of tax.

- Option B: Option B sees the scale of sell-down decline over time, spreading total sales over four years. This approach takes a little longer and increases the amount of portfolio risk in later years (relative to Option A), but it reduces total taxes by around $10,000

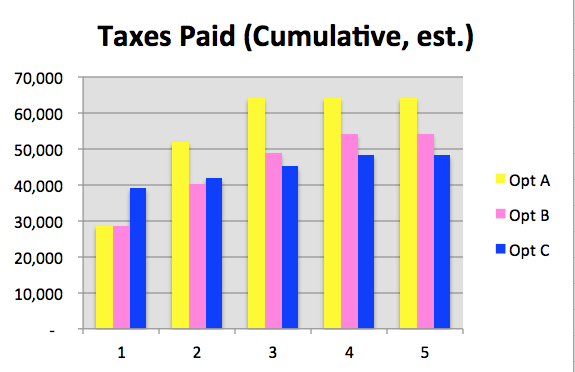

- Option C: The third option shows what happens if shares are sold-off very aggressively ($270,000 in the first year), followed by much more gradual sales in later years. This approach has the effect of immediately reducing risk, then tapering sales across another four years (total five years). Initially tax is higher, however owing to the fact that total tax payable results not only from the headline tax rate but also from differences between Marginal Tax Rate bands, the overall amount of tax paid is about $15,000 less than in Option A.

Note on taxes - Option C

To explain my comments on headline tax vs Marginal Tax Rates we need to look understand that the "steps" between tax brackets (Marginal Tax Rates) are not smooth or even. For example, consider someone earning $90,000 per annum; they will pay tax (and Medicare) at a rate of 39% on income above $87,000, 34.5% on income between $37,000 and $86,999, and so on and so forth. In other words the "step" between these tax brackets is 4.5%. Meanwhile for someone earning $25,000, while they are in a 21% tax & Medicare bracket, their effective marginal tax rate is actually about 29%. Then we have people with assessable income below about $20,540; while they are above the tax-free threshold they don't actually pay tax. By navigating these "steps" investors are able to better understand when it might be better to pay additional tax now (i.e., stepping up 4.5% from 34.5% to 39%) so that they may "step down" (say, from 29% to 0%) in other tax periods. Don't get too caught up in the details of this, the key message is that when tax planning it pays to view it across multiple years.

|

|

|

|

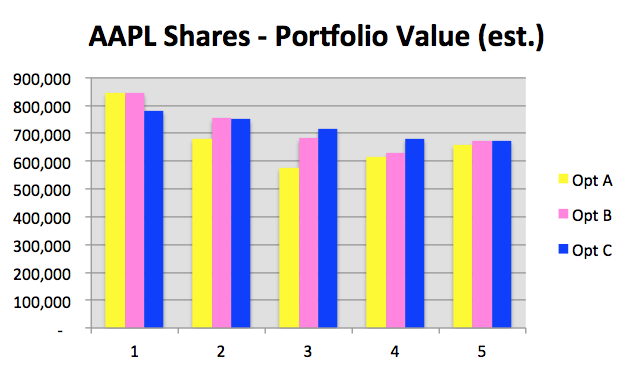

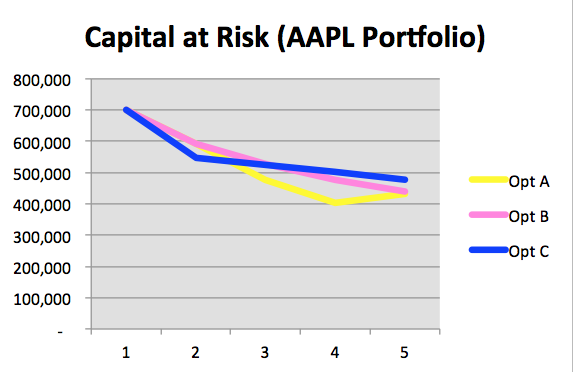

From these scenarios our preference is Option C. This strategy is most effective in rapidly reducing risk (the key objective) while minimising overall taxes.

Moreover, the sequence of sell-down helps minimise potential regret. The table below helps illustrate this. Here we see the estimated value of your AAPL portfolio after 5 years, less the taxes paid on share sales over the preceding 5 years. You can see that for portfolio returns above about -10% your AAPL portfolio is largest under Option C. Note: this is not intended as a realistic guide to returns, particularly in the short term, and especially as currency factors must be included in any total return forecast.

Moreover, the sequence of sell-down helps minimise potential regret. The table below helps illustrate this. Here we see the estimated value of your AAPL portfolio after 5 years, less the taxes paid on share sales over the preceding 5 years. You can see that for portfolio returns above about -10% your AAPL portfolio is largest under Option C. Note: this is not intended as a realistic guide to returns, particularly in the short term, and especially as currency factors must be included in any total return forecast.

Process

The actual process of selling down your shares is quite simple. You have stated that your AAPL shares are already CHESS sponsored. CHESS (Clearing House Electronic Subregister System) is merely a way for brokers (and this includes discount/online brokers) to handle and settle trades without manually looking up the details of who owns what (etc etc).

As you are CHESS sponsored, I would suggest the first step is to find out who your sponsor is, and then consider whether or not they have the facilities to cost-effectively process any share trades on your behalf. If they don't offer the services you need, simply setup an share trading account elsewhere.

The alternative is just to setup a new share broking account and have your shares transferred over to it (technically you are nominating the new broker as your new CHESS sponsor).

Once you have setup your account with your CHESS sponsor, you should have online access that shows your shareholding and provides options for buying/selling shares. Most brokers' systems are very straightforward, you should not have any issues working out how to do this.

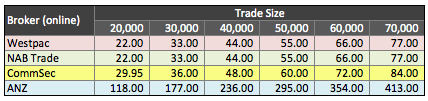

While I will shy away from recommending one broker over another, I provide below a table which summarises the brokerage costs for the online brokerage accounts from the "big four". I personally use Westpac, though have also used CommSec (and others) in the past. These days all have plenty of free "bells and whistles", plus options for more if you wish to pay a bit extra. If you setup an account with a broker with whom you do not also have a bank account please double-check fees as they may vary (some brokers call these "non-integrated accounts").

The actual process of selling down your shares is quite simple. You have stated that your AAPL shares are already CHESS sponsored. CHESS (Clearing House Electronic Subregister System) is merely a way for brokers (and this includes discount/online brokers) to handle and settle trades without manually looking up the details of who owns what (etc etc).

As you are CHESS sponsored, I would suggest the first step is to find out who your sponsor is, and then consider whether or not they have the facilities to cost-effectively process any share trades on your behalf. If they don't offer the services you need, simply setup an share trading account elsewhere.

The alternative is just to setup a new share broking account and have your shares transferred over to it (technically you are nominating the new broker as your new CHESS sponsor).

Once you have setup your account with your CHESS sponsor, you should have online access that shows your shareholding and provides options for buying/selling shares. Most brokers' systems are very straightforward, you should not have any issues working out how to do this.

While I will shy away from recommending one broker over another, I provide below a table which summarises the brokerage costs for the online brokerage accounts from the "big four". I personally use Westpac, though have also used CommSec (and others) in the past. These days all have plenty of free "bells and whistles", plus options for more if you wish to pay a bit extra. If you setup an account with a broker with whom you do not also have a bank account please double-check fees as they may vary (some brokers call these "non-integrated accounts").

Next Steps

The next step for you is to confirm your CHESS registration and consider your options for implementing sales. You may need to register for a new share trading account (relatively straightforward process).

Once your account is setup and your AAPL shares have been attached to your online account, you should confirm your income expectations for the years ahead. This is to ensure you are aware of the tax consequences from any trading.

Finally, the lot size will need to be chosen. It is generally advisable to stagger trades over time, though given AAPL's size market depth and liquidity will not be an issue.

After this is complete you are ready to go. Double check you have everything in order before commencing trading.

As always, if unsure of anything please don't hesitate to call on 0406 695 257.

Warm regards,

Joel Mitchell, CFA

Director, Third Sector Advantage

[email protected]

The next step for you is to confirm your CHESS registration and consider your options for implementing sales. You may need to register for a new share trading account (relatively straightforward process).

Once your account is setup and your AAPL shares have been attached to your online account, you should confirm your income expectations for the years ahead. This is to ensure you are aware of the tax consequences from any trading.

Finally, the lot size will need to be chosen. It is generally advisable to stagger trades over time, though given AAPL's size market depth and liquidity will not be an issue.

After this is complete you are ready to go. Double check you have everything in order before commencing trading.

As always, if unsure of anything please don't hesitate to call on 0406 695 257.

Warm regards,

Joel Mitchell, CFA

Director, Third Sector Advantage

[email protected]

About your Adviser

Your wealth adviser is Joel Mitchell, CFA®. Joel has been providing strategy and investment advice to clients for over a decade and presently advises on a portfolio of assets valued at more than $240 million on behalf of superannuants, professional investors, charitable foundations and the Australian government.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.