John & Catherine Weir |

Review of Trust Accounts - 7 August 2017 |

Dear John and Cathy,

At our last meeting I suggested we again review the usefulness and cost effectiveness of retaining your Trust accounts.

As you know there are two broad benefits associated with Trusts; tax minimisation and asset protection.

Starting with tax, the benefit of Trusts is that they can distribute income to beneficiaries in whichever manner it (the Trustee) decides. Where the taxable income of beneficiaries vary significantly there can be great benefit from using Trusts. Conversely where tax rates of the beneficiaries are the same there is little to no tax benefit available.

Arguably a bigger benefit of Trusts is that they offer great benefit from an asset-protection standpoint. This is because the beneficiaries don't "own" the assets, so in a legal proceeding the Trust's assets are essentially out of reach from creditors. This is one of the reasons Trusts are very popular with small business and people who feel they may be at risk of legal action being taken against them (this makes them very popular among medical professionals).

There are also downsides to Trusts. Most notably they can be expensive to operate and are not always tax efficient. They can also be inflexible and do not always offer perfect asset protection, particularly if the beneficiary requires disbursements from the Trust to survive. For these reasons it's important to carefully consider whether a Trust is an appropriate vehicle for your wealth.

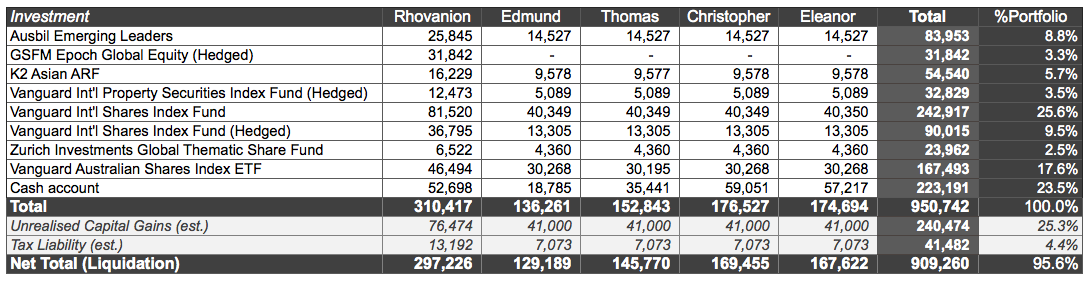

The table below summarises your Trust's current investment portfolio, plus those for each of your four children:

At our last meeting I suggested we again review the usefulness and cost effectiveness of retaining your Trust accounts.

As you know there are two broad benefits associated with Trusts; tax minimisation and asset protection.

Starting with tax, the benefit of Trusts is that they can distribute income to beneficiaries in whichever manner it (the Trustee) decides. Where the taxable income of beneficiaries vary significantly there can be great benefit from using Trusts. Conversely where tax rates of the beneficiaries are the same there is little to no tax benefit available.

Arguably a bigger benefit of Trusts is that they offer great benefit from an asset-protection standpoint. This is because the beneficiaries don't "own" the assets, so in a legal proceeding the Trust's assets are essentially out of reach from creditors. This is one of the reasons Trusts are very popular with small business and people who feel they may be at risk of legal action being taken against them (this makes them very popular among medical professionals).

There are also downsides to Trusts. Most notably they can be expensive to operate and are not always tax efficient. They can also be inflexible and do not always offer perfect asset protection, particularly if the beneficiary requires disbursements from the Trust to survive. For these reasons it's important to carefully consider whether a Trust is an appropriate vehicle for your wealth.

The table below summarises your Trust's current investment portfolio, plus those for each of your four children:

Key Considerations

Unrealised Capital Gains

Concentrating on the Rhovanion Trust for a moment, we see there are approximately $76,500 of unrealised capital gains within your portfolio. While we did make some adjustments last year, continued growth in the value of share investments has continued to compound the impending tax liability. I estimate the tax payable on closure of this portfolio to be around $13,000.

Fees

So far as fees go, actual investment, administration and advice fees are very low for an account of this type. This is in part due to the fee rebates we obtained when we first established the account. To be honest advice fees have been set unsustainably low (my fault), which is an issue we are going to have to address.

Investment Allocation & Risk

From an asset allocation and risk perspective the portfolio is complimentary to your other key portfolios.

Your AAPL shares provide a highly concentrated exposure to North America and the IT/Tech sector in particular, while your superannuation portfolios hold substantial unlisted assets. You also have a large exposure to Australian property, via your investment property in Richmond, home in Malvern, and farmland at Pipers Creek. Rhovanion, on the other hand, has a slight value tilt, plus emerging markets.

Unrealised Capital Gains

Concentrating on the Rhovanion Trust for a moment, we see there are approximately $76,500 of unrealised capital gains within your portfolio. While we did make some adjustments last year, continued growth in the value of share investments has continued to compound the impending tax liability. I estimate the tax payable on closure of this portfolio to be around $13,000.

Fees

So far as fees go, actual investment, administration and advice fees are very low for an account of this type. This is in part due to the fee rebates we obtained when we first established the account. To be honest advice fees have been set unsustainably low (my fault), which is an issue we are going to have to address.

Investment Allocation & Risk

From an asset allocation and risk perspective the portfolio is complimentary to your other key portfolios.

Your AAPL shares provide a highly concentrated exposure to North America and the IT/Tech sector in particular, while your superannuation portfolios hold substantial unlisted assets. You also have a large exposure to Australian property, via your investment property in Richmond, home in Malvern, and farmland at Pipers Creek. Rhovanion, on the other hand, has a slight value tilt, plus emerging markets.

Is the Rhovanion Trust still achieving its objectives?

To determine whether Rhovanion is viable and still relevant there are a number of factors to consider, such as your taxable position (which is likely to be influenced heavily by the sale of AAPL shares), costs of retaining the Trust, and alternative uses for the proceeds from Rhovanion.

Perhaps the starting point is deciding on the timing for closure of Rhovanion. If it was closed this Financial Year it will likely result in taxes of about $13,000; however even if we defer closure it is unlikely we will avoid taxes altogether. Pushing closure back until after tranches of AAPL shares are sold (4 - 5 years) will probably still result in tax of around $7,000; that's $5,000 difference, or about $1,000 per annum. If you are paying more than $1,000 per annum to keep the account open, then the end result is going to be very close.

What's more, if the portfolio continues to accumulate gains, what you decide to do now will have an even greater impact on the end result.

An example:

For example, let's say that a hypothetical portfolio earns 7% per annum (net fees but pre-tax), of which 4% is income and 3% capital growth.

Retaining Rhovanion

Over a five-year period, within Rhovanion the portfolio would be expected to grow to around $349,000 while distributing $66,000 (about $43,000, after tax) of income. The portfolio now has unrealised gains of around $115,000, which if sold at the end of the five-year period (and assuming AAPL share sales were complete) would attract capital gains tax of approximately $12,000.

Therefore the net value extracted from the portfolio is:

Liquidating Rhovanion

Alternatively, let's say we liquidated Rhovanion, then contributed the proceeds to superannuation (as a cash contribution), which we then moved into a superannuation Pension account.

As we bring-forward the tax event, we lose $13,000 in tax at the start. This reduces the amount we contribute to super from $310,417 (the current balance) to $297,226 (the balance after tax).

Over the next five years this portfolio will generate income of $64,000, and will attain a closing balance of $344,000. As the assets are in a tax-free pension there is no tax on earnings (tax of up to 15% would be payable if in superannuation accumulation phase).

Therefore the net value extracted from the portfolio is:

This example highlights the difference in result from changing the investment tax structure. Once fees are taken into account we would expect the difference in results to be even greater.

To determine whether Rhovanion is viable and still relevant there are a number of factors to consider, such as your taxable position (which is likely to be influenced heavily by the sale of AAPL shares), costs of retaining the Trust, and alternative uses for the proceeds from Rhovanion.

Perhaps the starting point is deciding on the timing for closure of Rhovanion. If it was closed this Financial Year it will likely result in taxes of about $13,000; however even if we defer closure it is unlikely we will avoid taxes altogether. Pushing closure back until after tranches of AAPL shares are sold (4 - 5 years) will probably still result in tax of around $7,000; that's $5,000 difference, or about $1,000 per annum. If you are paying more than $1,000 per annum to keep the account open, then the end result is going to be very close.

What's more, if the portfolio continues to accumulate gains, what you decide to do now will have an even greater impact on the end result.

An example:

For example, let's say that a hypothetical portfolio earns 7% per annum (net fees but pre-tax), of which 4% is income and 3% capital growth.

Retaining Rhovanion

Over a five-year period, within Rhovanion the portfolio would be expected to grow to around $349,000 while distributing $66,000 (about $43,000, after tax) of income. The portfolio now has unrealised gains of around $115,000, which if sold at the end of the five-year period (and assuming AAPL share sales were complete) would attract capital gains tax of approximately $12,000.

Therefore the net value extracted from the portfolio is:

- Assets liquidated (end): $349,000

- Plus distributions: $66,000

- Less tax on distributions: $23,000

- Less capital gains tax: $12,000

- Total Value: $380,000

Liquidating Rhovanion

Alternatively, let's say we liquidated Rhovanion, then contributed the proceeds to superannuation (as a cash contribution), which we then moved into a superannuation Pension account.

As we bring-forward the tax event, we lose $13,000 in tax at the start. This reduces the amount we contribute to super from $310,417 (the current balance) to $297,226 (the balance after tax).

Over the next five years this portfolio will generate income of $64,000, and will attain a closing balance of $344,000. As the assets are in a tax-free pension there is no tax on earnings (tax of up to 15% would be payable if in superannuation accumulation phase).

Therefore the net value extracted from the portfolio is:

- Assets liquidated (end): $344,000

- Plus distributions: $64,000

- Less tax on distributions: $Nil

- Less capital gains tax: $Nil

- Total Value: $408,000

This example highlights the difference in result from changing the investment tax structure. Once fees are taken into account we would expect the difference in results to be even greater.

Recommendations

Having reviewed the Rhovanion's investment and fee structure are reasons both for retaining and for closing the Trust.

As an investment structure it is not nearly as efficient as can be achieved through a public offer superannuation Fund, and provides only a very minor edge over what is available from other asset protection vehicles, such as Investment Bonds. The counter argument is that it does provide greater flexibility - both from an investment selection and income disbursement perspective - should these features be required.

You have previously stated that you would like to simplify your financial situation. This being the case, I would lean toward closing the Trust in favour of a more efficient investment structure. Given your ages and financial position the obvious choice would be superannuation as you have a number of years over which you can continue to contribute, and once assets are within super (particularly if contributed using after-tax money) they are treated very favourably.

Before making a decision please discuss with your accountant. With your permission, it would be good to speak with your accountant about this as some of the information I have about the Trust (from a tax perspective) may be unavailable to your accountant.

Having reviewed the Rhovanion's investment and fee structure are reasons both for retaining and for closing the Trust.

As an investment structure it is not nearly as efficient as can be achieved through a public offer superannuation Fund, and provides only a very minor edge over what is available from other asset protection vehicles, such as Investment Bonds. The counter argument is that it does provide greater flexibility - both from an investment selection and income disbursement perspective - should these features be required.

You have previously stated that you would like to simplify your financial situation. This being the case, I would lean toward closing the Trust in favour of a more efficient investment structure. Given your ages and financial position the obvious choice would be superannuation as you have a number of years over which you can continue to contribute, and once assets are within super (particularly if contributed using after-tax money) they are treated very favourably.

Before making a decision please discuss with your accountant. With your permission, it would be good to speak with your accountant about this as some of the information I have about the Trust (from a tax perspective) may be unavailable to your accountant.

Next Steps

If you have any questions please contact me directly on 0406 695 257

Regards,

Joel Mitchell, CFA

Director, Third Sector Advantage

[email protected]

If you have any questions please contact me directly on 0406 695 257

Regards,

Joel Mitchell, CFA

Director, Third Sector Advantage

[email protected]

About your Adviser

Your wealth adviser is Joel Mitchell, CFA®. Joel has been providing strategy and investment advice to clients for over a decade and presently advises on a portfolio of assets valued at more than $240 million on behalf of superannuants, professional investors, charitable foundations and the Australian government.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.