ASX:SWM - Seven West Media

|

Initial review

1 August 2020 Current Price: $0.092 (~ $140 m) 10 Year Price Target: $0.68 ($1.04 billion) RoIC (inc. dividends): 24.7% pa gross / ~16% pa net real |

Updated following release of FY2020 Annual Report

25 August 2020 Current Price: $0.12 (~ $184 m) 10 Year Price Target: $0.92 ($1.41 billion) RoIC (inc. dividends): 25.0% pa gross / ~18.6% pa net real |

From email to HB 1/08/2020

Hi Henry,

Hope you’re well.

By now you would realise that I don’t mind looking at small, obscure, tightly held businesses, especially those that look destined for the scrap heap.

I take the view that things get cheap (or expensive) for a reason, and if you figure out “why” they are being treated/valued) a particular way then -- from time-to-time — you can find some pretty attractive investment opportunities, even if one of the potential outcomes is catastrophic failure.

One such example that I have recently added to my own portfolio is Seven West Media (ASX:SWM). If that made you wince in discomfort, then you are not alone!

When think of others that have found themselves in the same category of “priced for failure” — like TRS in June last year, or ATL during the first wave of COVID-19 — but they were objectively better (albeit much smaller) businesses. With SWM there is “less to love”. ...But, I think that even with all their problems/risks, there is an asymmetry to their potential outcomes that makes it very interesting.

Before starting, I will be clear: this is a company that I strongly believe will not survive the next 5 - 10 years in it’s current form, and there is a moderately high (20%-30%) chance equity investors could be wiped out.

Disclaimer: this is (obviously) not advice, and is not intended to influence you or anyone either way. It’s just some random rants about a company I thought was interesting. I hold some shares in the company, so be warned — my comments/opinion may be tainted.

______________________

Things that I (and EVERYONE) don’t like about the business:

However, there are some brighter spots….

The outlook: Business growth, strategy & sales…

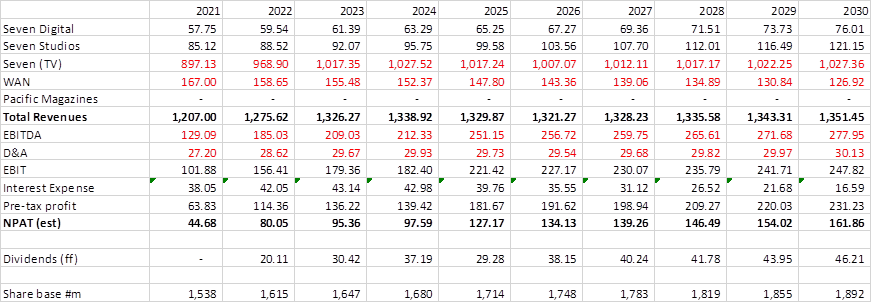

Though the largest source of revenue is still TV, this is far less profitable than their digital channels and production company (both of which run an EBIT around 1.5x higher). Digital business has built their key infrastructure, is growing strongly, asset light and offers very high incremental profits.

The one asset that now looks out of place is WA Newspapers. It’s still profitable, but you would have to think that with WA radio assets and the magazine business gone this “local” business will be next to be sold. I don’t know if they are planning on selling it – reckon they might be able to get $150 - $200m for it.

They have also stated their intention to look at selling Seven Studios (production company) and their Ventures business. If they do this would turn them into a more pure advertising platform. Upside of selling 7Studios is that (I think) they could potentially get another $400-500m, which would allow them to clean a huge amount of debt out of the business. If they go down that path the remaining business lines could probably still support revenues somewhere north of $1 billion pa and NPAT of $60 - $80 m pa.

Short-term outlook…

Take short-term outlooks with a grain of salt, but I have mentioned it here mostly for the purpose of weighing the probability that they will end up in strife and be forced to do something drastic. So here I go:

Adjusted for the pandemic (interruption to sport, lower advertising spend) and Toyko Olympics next year, I expect Channel 7 to book FY21 revenues somewhere in the vicinity of $820 - $850m, plus $120 - $150m from Seven Digital and 7Studios and $180 m from WA Newspapers. Erring on the side of caution, I expect finance costs and D&A to rise, but still think we could see NPAT of $30 - $60m (base case: NPAT $43m). I don’t expect to see dividends for a year or two (at best). Without sounding like an advertisement for the company, they do hold a dominant position in the free to air TV space, and while nothing lasts for ever it’s seems unlikely that market share will shift much in the next 2-3 years. In other words, excluding abnormal items, I think they should be ok.

What could go wrong?

Answer: Plenty. They have made some HUGE impairments on their licences - about $500m over the last 18 months. This seems reasonable, but certainly the potential there is more to come and this could create issues in keeping their creditors happy. If creditors do push back then they could be forced to issue more shares to raise capital (much like what happened with SXL earlier this year). For example, raising another $300m at issue price of $0.05 = 6 billion new shares, increase of 390%. …makes the whole thing seem very unattractive. If this happens, investors should expect to take a hit (back-of-the-envelope calculation; diluted value of recapitalised business would probably see investors lose 20% - 40% from current price). Of course, it could turn out worse that this!

…a bit more on impairments….

For bonus points, the footnotes to their impairments were interesting – looks like they are expecting television to decline over time (+0.5% nominal rate, so presumably somewhere the order of -1.5% to -2% pa. after inflation).

Insofar as the immediate concern for impairments go, it doesn’t really matter if this guess turns out to be accurate. The reason? We can fiddle with the discount and growth rates to see that even if free-to-air TV was to jump off a cliff and go into decline at, say, 20% per annum real, their licences would still be valued at between $200 and $250m. So, worst case scenario there is maybe another $200m of potential impairments. If this happened I would expect the creditors to start sharpening their pitchforks, but it probably wouldn’t be enough to sink the ship. **And, I really don’t think a 20% pa real decline in their free to air stations is going to happen.

Note: The cash from Osborne Park and Pacific Magazines alone should buy a bit of breathing room -- prob $200-$300m worth. And, as noted above, an impairment of that size would require a further 40%-60% write down in the value of their TV licences. Keep in mind that the advertising revenue alone from these licences is close to $1 billion pa.

…margin compression...

The other risk, which I think is inevitable, is we could also see margins in their existing businesses decline. Their digital business is in competition with all other digital providers (and competitors like Nine have a broader range of digital offerings, like Stan). Seven Studios competes against local and international producers and needs to keep winning projects from Amazon/Netflix etc to keep growing. TV business requests advertising spend to hold up. If more of this goes into other channels they will see their profits decline.

Another thing…

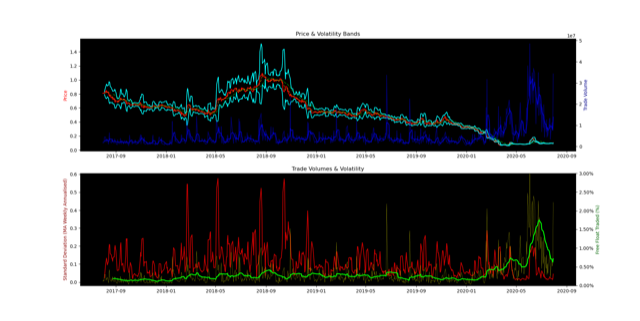

Company is tightly held. 86% of the company is owned by the top 20 shareholders, and over 40% by Seven West alone. They were recently removed from ASX300 means even fewer analysts covering them, and institutional investors are more likely to take their position indirectly through Seven West (which has better market depth and a more diversified portfolio of businesses - Caterpillar etc). Some would see the lack of coverage and market depth as a negative feature, but personally I like the illiquidity. More inefficiency in pricing, the better. Been a slight up-tick in trading lately but very quiet on the 3Y front. (trade volumes and volatility over the last 3 years below)

Hope you’re well.

By now you would realise that I don’t mind looking at small, obscure, tightly held businesses, especially those that look destined for the scrap heap.

I take the view that things get cheap (or expensive) for a reason, and if you figure out “why” they are being treated/valued) a particular way then -- from time-to-time — you can find some pretty attractive investment opportunities, even if one of the potential outcomes is catastrophic failure.

One such example that I have recently added to my own portfolio is Seven West Media (ASX:SWM). If that made you wince in discomfort, then you are not alone!

When think of others that have found themselves in the same category of “priced for failure” — like TRS in June last year, or ATL during the first wave of COVID-19 — but they were objectively better (albeit much smaller) businesses. With SWM there is “less to love”. ...But, I think that even with all their problems/risks, there is an asymmetry to their potential outcomes that makes it very interesting.

Before starting, I will be clear: this is a company that I strongly believe will not survive the next 5 - 10 years in it’s current form, and there is a moderately high (20%-30%) chance equity investors could be wiped out.

Disclaimer: this is (obviously) not advice, and is not intended to influence you or anyone either way. It’s just some random rants about a company I thought was interesting. I hold some shares in the company, so be warned — my comments/opinion may be tainted.

______________________

Things that I (and EVERYONE) don’t like about the business:

- Core business (TV) is in structural decline thanks to digital and on-demand alternatives

- Highly leveraged.

- They have lost their radio and magazine distribution/advertising channels.

- SWM have spent a lot of money for rights to sporting events (AFL, cricket, Olympics) which have now been deferred or compressed.

- TV advertising spend continues to contract (economic reasons, COVID-19, move to digital platforms etc).

- Could be more impairments on the way...

However, there are some brighter spots….

- Over the last 12 months they have absorbed Prime, increasing their reach to regional viewers. This has now been paid for (largely scrip issue). Synergies est >$10m pa, expect this to be value accretive over the medium term.

- After taking over Prime, they sold Osborne Park for $75m, with tenancy to be continued for the next 15 years or so.

- They sold Pacific Magazines to Bauer for $40m (plus around $6.6m in advertising spend)

- The sold their WA radio assets (Redwave) for $28m.

- The sales raise about $140m cash, reducing their borrowings by around 20%, and net debt by about 25% from $570m to $430m.

- I expect the net impact on pre-tax profit is about neutral -- give or take $2-$3m pa.

The outlook: Business growth, strategy & sales…

Though the largest source of revenue is still TV, this is far less profitable than their digital channels and production company (both of which run an EBIT around 1.5x higher). Digital business has built their key infrastructure, is growing strongly, asset light and offers very high incremental profits.

The one asset that now looks out of place is WA Newspapers. It’s still profitable, but you would have to think that with WA radio assets and the magazine business gone this “local” business will be next to be sold. I don’t know if they are planning on selling it – reckon they might be able to get $150 - $200m for it.

They have also stated their intention to look at selling Seven Studios (production company) and their Ventures business. If they do this would turn them into a more pure advertising platform. Upside of selling 7Studios is that (I think) they could potentially get another $400-500m, which would allow them to clean a huge amount of debt out of the business. If they go down that path the remaining business lines could probably still support revenues somewhere north of $1 billion pa and NPAT of $60 - $80 m pa.

Short-term outlook…

Take short-term outlooks with a grain of salt, but I have mentioned it here mostly for the purpose of weighing the probability that they will end up in strife and be forced to do something drastic. So here I go:

Adjusted for the pandemic (interruption to sport, lower advertising spend) and Toyko Olympics next year, I expect Channel 7 to book FY21 revenues somewhere in the vicinity of $820 - $850m, plus $120 - $150m from Seven Digital and 7Studios and $180 m from WA Newspapers. Erring on the side of caution, I expect finance costs and D&A to rise, but still think we could see NPAT of $30 - $60m (base case: NPAT $43m). I don’t expect to see dividends for a year or two (at best). Without sounding like an advertisement for the company, they do hold a dominant position in the free to air TV space, and while nothing lasts for ever it’s seems unlikely that market share will shift much in the next 2-3 years. In other words, excluding abnormal items, I think they should be ok.

What could go wrong?

Answer: Plenty. They have made some HUGE impairments on their licences - about $500m over the last 18 months. This seems reasonable, but certainly the potential there is more to come and this could create issues in keeping their creditors happy. If creditors do push back then they could be forced to issue more shares to raise capital (much like what happened with SXL earlier this year). For example, raising another $300m at issue price of $0.05 = 6 billion new shares, increase of 390%. …makes the whole thing seem very unattractive. If this happens, investors should expect to take a hit (back-of-the-envelope calculation; diluted value of recapitalised business would probably see investors lose 20% - 40% from current price). Of course, it could turn out worse that this!

…a bit more on impairments….

For bonus points, the footnotes to their impairments were interesting – looks like they are expecting television to decline over time (+0.5% nominal rate, so presumably somewhere the order of -1.5% to -2% pa. after inflation).

Insofar as the immediate concern for impairments go, it doesn’t really matter if this guess turns out to be accurate. The reason? We can fiddle with the discount and growth rates to see that even if free-to-air TV was to jump off a cliff and go into decline at, say, 20% per annum real, their licences would still be valued at between $200 and $250m. So, worst case scenario there is maybe another $200m of potential impairments. If this happened I would expect the creditors to start sharpening their pitchforks, but it probably wouldn’t be enough to sink the ship. **And, I really don’t think a 20% pa real decline in their free to air stations is going to happen.

Note: The cash from Osborne Park and Pacific Magazines alone should buy a bit of breathing room -- prob $200-$300m worth. And, as noted above, an impairment of that size would require a further 40%-60% write down in the value of their TV licences. Keep in mind that the advertising revenue alone from these licences is close to $1 billion pa.

…margin compression...

The other risk, which I think is inevitable, is we could also see margins in their existing businesses decline. Their digital business is in competition with all other digital providers (and competitors like Nine have a broader range of digital offerings, like Stan). Seven Studios competes against local and international producers and needs to keep winning projects from Amazon/Netflix etc to keep growing. TV business requests advertising spend to hold up. If more of this goes into other channels they will see their profits decline.

Another thing…

Company is tightly held. 86% of the company is owned by the top 20 shareholders, and over 40% by Seven West alone. They were recently removed from ASX300 means even fewer analysts covering them, and institutional investors are more likely to take their position indirectly through Seven West (which has better market depth and a more diversified portfolio of businesses - Caterpillar etc). Some would see the lack of coverage and market depth as a negative feature, but personally I like the illiquidity. More inefficiency in pricing, the better. Been a slight up-tick in trading lately but very quiet on the 3Y front. (trade volumes and volatility over the last 3 years below)

Overall….

I reckon there is maybe a 20%-30% chance that SWM gets smashed by competition and/or their creditors. If that happens present-day investors are going to have a pretty bad time.

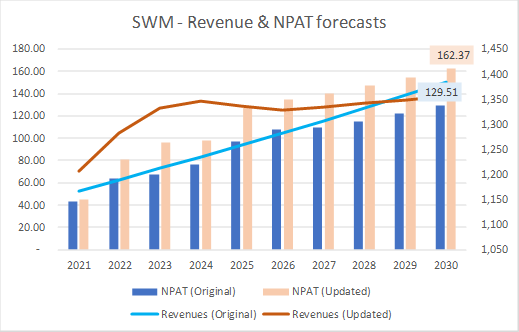

Alternatively, if they continue to tighten up their business I think the future is a lot brighter. FY21 is probably going to be a write-off, though the Tokyo Olympics should give the a bit of a boost in H2. My crystal ball is broken so no idea where we go from there, but with a modest (perhaps overly conservative) projection of recovery still gets them a net profit of around $100m within 5 years if they keep WAN and 7Studios, and $60-$80m if they get rid of WAN, 7Studios and their Ventures businesses. For the consolidated business my 10 year target is a NPAT of about $130m, but if things go well it could be a lot higher than that (potentially >$250m).

So in summary:

I don’t particularly like the business, and like everyone I really don’t like their debt, but I think the current valuation (~ $140 m, $0.092) fails to account for the chance they might make it through the next few years more-or-less intact. This is definitely not on my “best ideas” list, but for me the asymmetric return profile (from current valuation c.$140m) makes it interesting and justifies its inclusion (albeit at a pretty small weighting).

I reckon there is maybe a 20%-30% chance that SWM gets smashed by competition and/or their creditors. If that happens present-day investors are going to have a pretty bad time.

Alternatively, if they continue to tighten up their business I think the future is a lot brighter. FY21 is probably going to be a write-off, though the Tokyo Olympics should give the a bit of a boost in H2. My crystal ball is broken so no idea where we go from there, but with a modest (perhaps overly conservative) projection of recovery still gets them a net profit of around $100m within 5 years if they keep WAN and 7Studios, and $60-$80m if they get rid of WAN, 7Studios and their Ventures businesses. For the consolidated business my 10 year target is a NPAT of about $130m, but if things go well it could be a lot higher than that (potentially >$250m).

So in summary:

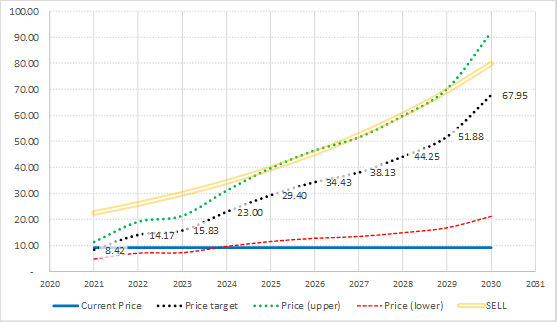

- Assume 30% chance company will fall apart of be destroyed

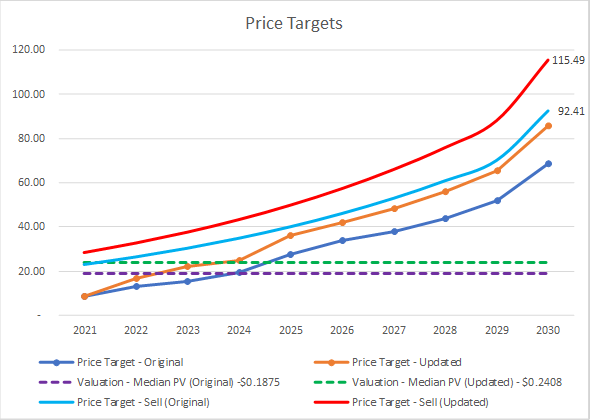

- 10 year price target $0.68, upper range (Sell target: $0.92)

- Est. cumulative dividends next 10 years ~ $0.146 ff ($0.20 grossed up)

- Upper bound return = Net Real return c. 23.4% pa. (10 year total RoIC +721%)

- Expected net return of approx. 16% pa (+304%)

I don’t particularly like the business, and like everyone I really don’t like their debt, but I think the current valuation (~ $140 m, $0.092) fails to account for the chance they might make it through the next few years more-or-less intact. This is definitely not on my “best ideas” list, but for me the asymmetric return profile (from current valuation c.$140m) makes it interesting and justifies its inclusion (albeit at a pretty small weighting).

FYI — Portfolio sizing...

To make it very clear…. There is a moderate chance this company will not survive, and very high probability it will not remain in it’s current form in the years to come. Do your own research (etc etc…).

All the best,

- Current price: $0.092 (valuation: $141m)

- Term: 10 years

- Hurdle (opportunity cost): 8% pa

- Inflation: 3%

- Volatility Premium: 1%

- Failure:

- Probability: 30%

- Loss at failure: 80%

- Liquidity Premium (one-off): 20%

- 10 year valuation — scenario 1 (consolidated):

- Probability 30%

- Price target - consolidated: $0.6795

- Sell Price target - consolidated: $0.91

- Cumulative dividends + imputation credits: $0.21 (~$257m)

- 10 year valuation - scenario 2 (post sales):

- Probability 40%

- Price target - consolidated: $0.58

- Sell Price target - consolidated: $0.73

- Cumulative dividends + imputation credits: $0.13 (~$160m)

- Net return:

- Success: +514% ( +19.9% pa)

- Failure: -64.4% ( -9.8% pa)

- Expected net (after tax) return: 304% ( +15% pa)

- Portfolio weighting (modified Kelly): 12.84% (Note: Kelly is the max weighting)

- Price (mod Kelly weight):

- $0.084 - 20%

- $0.074 - 30%

- Price (mod Kelly weight):

To make it very clear…. There is a moderate chance this company will not survive, and very high probability it will not remain in it’s current form in the years to come. Do your own research (etc etc…).

All the best,

From email update - 25/08/2020 (FY2020 Annual Report released on 25/08/2020)

FYI --- some more rants. Not advice (or suggestion of any kind).

I’ve now had time to look into SWM’s numbers in some detail. Some observations.

Considering substantial contraction in advertising markets over the last 6 months (and last quarter of FY20, in particular) their results were not all that surprising. Underlying NPAT (ex abnormals) was $40.8 m, with EBIT (ex abnormals) of around $99m. They reported a statutory loss of $294m, most of which had already been announced in the third half. This includes $123.5m impairment on intangibles and $137m hit from onerous contracts. Keep in mind Channel 7 is the major playing in sports broadcasting, so a large chunk of this them rightfully acknowledging that a bit chunk of revenues from CY2020 isn’t going to be earned. Hopefully Tokyo Olympics still goes ahead in CY21.

Good news:

Bad points:

Overall, I am more optimistic than I was a month ago. Debt – and specifically, their ability to meet their covenants – will be what makes or breaks them.

While a capital raising would significantly dilute existing shareholders it is not necessarily a bad option for investors. I don’t think it is too much of a stretch to say the operating businesses (in their current shape and form) is probably worth somewhere between $1.5 - $1.8 billion. After netting out liabilities for cash, property and financial assets, the company has around $1.02 billion in liabilities (and maybe as little as $850m, depending on assessment of lease liabilities). This values the equity component at somewhere around the $480 m - $780 m. The market currently values them at $200m (1.54 billion shares x $0.13). So on that (overly simplified) view of the operating businesses the company looks to be trading well under half its true value.

They are currently reporting a LVR of around 117%, but a lot of their assets and liabilities are operating items. Remove those and their “true” assets and liabilities come in somewhere around $482m and $1.4 billion (290%) with “only” $750m of this actual borrowings. As far as I can tell, SWM’s problem is not in making money (their operating businesses all do quite well). The risk is a lender won’t come to the party and roll over their debt (at a reasonable rate). Theoretically, they could replace all that debt through a capital raise. That would be extreme, but just to see the effect, if they did this at an issue price of (say) $0.10 per share, this would increase their total shares on issue to about 9 billion. In that very odd scenario, a business with an enterprise value of $1.5 - $1.8 billion would be “valued” at around $0.17 - $0.20 per share. A more sensible (less extreme) option might be to go half-way. Raising $375m at $0.10 would increase the share base to around 5.3 billion shares, and value the company’s equity at about $1.13 billion - $1.43 billion ( $0.21 - $0.27 per share).

Who knows if they will actually need (or choose) to raise more capital, but honestly I think that anyone looking at the business without assuming that’s on the cards in the next year or two is either crazy or missing the big picture. Personally I am taking the view that’s it’s coming one way or another (and this is actually one of the reasons I like the company; I think a capital raise could be a great benefit for investors).

Anyway. Who knows which way things will go, but the key message is that (with the hope we don’t dive too deeply into recession) I think SWM is probably going to be ok. My 10 year price (sell) target upgraded from $0.92 to $1.15. Median valuation $0.24, up from $0.19. Target entry price $0.17, up from $0.14.

Note: of course if a capital raise occurs these price targets get thrown out the window. Good news is that existing shareholders should be able to participate. So, for example, if they halved their debt by issuing another 3.75 billion shares, and they gave shareholders entitlements to reflect dilution (in this case 3.75 shares for each 1.54 existing) and you took part at $0.10, then a post-raise valuation of $0.21 per share would still look pretty good.

I’ve now had time to look into SWM’s numbers in some detail. Some observations.

Considering substantial contraction in advertising markets over the last 6 months (and last quarter of FY20, in particular) their results were not all that surprising. Underlying NPAT (ex abnormals) was $40.8 m, with EBIT (ex abnormals) of around $99m. They reported a statutory loss of $294m, most of which had already been announced in the third half. This includes $123.5m impairment on intangibles and $137m hit from onerous contracts. Keep in mind Channel 7 is the major playing in sports broadcasting, so a large chunk of this them rightfully acknowledging that a bit chunk of revenues from CY2020 isn’t going to be earned. Hopefully Tokyo Olympics still goes ahead in CY21.

Good news:

- Margins have held up reasonably well

- Lost around 1.4% market share of free-to-air advertising spend

- WA newspaper revenue down around 10%, but much better than broader market (advertising revenues down 9.6% vs 23.4% for newspaper advertising market)

- A number of one-off items relating to recognition and reclassification of assets & liabilities (deferred tax liability approx. $139, AASB lease adjustments ~ $58m)

- Advertising market spend was down 41% in June quarter; were markets/borders to reopen we may see a boost from pent-up demand.

Bad points:

- Debt is still very high, with net debt of around $398m. They have facilities of $750m, which they have almost completely exhausted. One of these tranches is up for refinance at the end of the year. Depending on how the next 6 months play out, they may need to find alternative sources of funding (read: capital raising)

- Majority of their operating cashflow of $47.5m was from discontinued operations (Redwave and Pacific Magazines).

- Economy continues to weaken – potential for further downturn in advertising market.

Overall, I am more optimistic than I was a month ago. Debt – and specifically, their ability to meet their covenants – will be what makes or breaks them.

While a capital raising would significantly dilute existing shareholders it is not necessarily a bad option for investors. I don’t think it is too much of a stretch to say the operating businesses (in their current shape and form) is probably worth somewhere between $1.5 - $1.8 billion. After netting out liabilities for cash, property and financial assets, the company has around $1.02 billion in liabilities (and maybe as little as $850m, depending on assessment of lease liabilities). This values the equity component at somewhere around the $480 m - $780 m. The market currently values them at $200m (1.54 billion shares x $0.13). So on that (overly simplified) view of the operating businesses the company looks to be trading well under half its true value.

They are currently reporting a LVR of around 117%, but a lot of their assets and liabilities are operating items. Remove those and their “true” assets and liabilities come in somewhere around $482m and $1.4 billion (290%) with “only” $750m of this actual borrowings. As far as I can tell, SWM’s problem is not in making money (their operating businesses all do quite well). The risk is a lender won’t come to the party and roll over their debt (at a reasonable rate). Theoretically, they could replace all that debt through a capital raise. That would be extreme, but just to see the effect, if they did this at an issue price of (say) $0.10 per share, this would increase their total shares on issue to about 9 billion. In that very odd scenario, a business with an enterprise value of $1.5 - $1.8 billion would be “valued” at around $0.17 - $0.20 per share. A more sensible (less extreme) option might be to go half-way. Raising $375m at $0.10 would increase the share base to around 5.3 billion shares, and value the company’s equity at about $1.13 billion - $1.43 billion ( $0.21 - $0.27 per share).

Who knows if they will actually need (or choose) to raise more capital, but honestly I think that anyone looking at the business without assuming that’s on the cards in the next year or two is either crazy or missing the big picture. Personally I am taking the view that’s it’s coming one way or another (and this is actually one of the reasons I like the company; I think a capital raise could be a great benefit for investors).

Anyway. Who knows which way things will go, but the key message is that (with the hope we don’t dive too deeply into recession) I think SWM is probably going to be ok. My 10 year price (sell) target upgraded from $0.92 to $1.15. Median valuation $0.24, up from $0.19. Target entry price $0.17, up from $0.14.

Note: of course if a capital raise occurs these price targets get thrown out the window. Good news is that existing shareholders should be able to participate. So, for example, if they halved their debt by issuing another 3.75 billion shares, and they gave shareholders entitlements to reflect dilution (in this case 3.75 shares for each 1.54 existing) and you took part at $0.10, then a post-raise valuation of $0.21 per share would still look pretty good.