Susan's story

Susan recently turned 57 and although she earns a good wage of $90,000 per annum plus 10% superannuation and has no plans on retiring for another few years she feels that she is financially unprepared for retirement.

She is a disciplined saver, having consistently set aside $2,000 per month of her wage into a high interest savings account. Over the past 4 years the balance of this account has grown to $120,000. The current interest rate on this account is 4% p.a.

She has also accumulated $350,000 in superannuation of which 30% is invested in a FI Managers International, a managed fixed income and cash portfolio (yielding 3.5% after fees), and the remaining 70% is invested across a range of shares and listed property trusts (yielding approximately 7.5% p.a.).

Susan currently pays $480 per week to rent an inner-city unit, however she dreams of retiring to the country. She enjoys living in the city, however says that if she could afford it she would ideally like to buy a home with a few acres in her hometown of Healesville, about an hour out of Melbourne. She has priced homes in the area and expects that to buy her "dream home" would cost her approximately $650,000.

She is a disciplined saver, having consistently set aside $2,000 per month of her wage into a high interest savings account. Over the past 4 years the balance of this account has grown to $120,000. The current interest rate on this account is 4% p.a.

She has also accumulated $350,000 in superannuation of which 30% is invested in a FI Managers International, a managed fixed income and cash portfolio (yielding 3.5% after fees), and the remaining 70% is invested across a range of shares and listed property trusts (yielding approximately 7.5% p.a.).

Susan currently pays $480 per week to rent an inner-city unit, however she dreams of retiring to the country. She enjoys living in the city, however says that if she could afford it she would ideally like to buy a home with a few acres in her hometown of Healesville, about an hour out of Melbourne. She has priced homes in the area and expects that to buy her "dream home" would cost her approximately $650,000.

The strategy

In Susan’s case, the strategy was relatively simple. Based on her income, expenses and savings, we are able to determine that her living expenses are approximately $45,400 per annum, of which nearly $25,000 p.a. (55%) is going towards rent.

Based on Susan’s objectives we recommended the following:

Based on Susan’s objectives we recommended the following:

- Establish a second superannuation account. Into this account transfer the $105,000 from her superannuation portfolio’s investment in FI Managers International.

- This leaves her original account with a balance of $245,000. To this we recommended she contribute $110,000 of her cash savings (keeping $10,000 cash for emergencies). No tax deduction is claimed for this contribution.

- After contributing her $110,000 of cash, commute the balance of her original superannuation account ($355,000) to an Account Based Pension, requesting the minimum level of income be drawn from this account on a monthly basis.

- Salary sacrifice $2,165 per month to her new superannuation account as a tax-deductible contribution.

- Upon turning 60, contribute any surplus cash to your superannuation portfolio, then roll the accumulated balance into a second Account Based Pension.

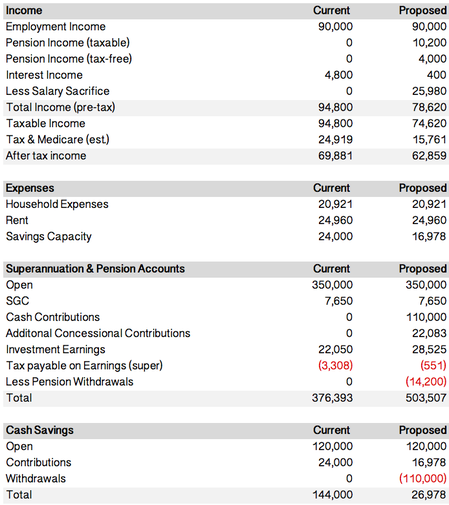

The outcome - pre-retirement

This strategy had the affect of reducing Susan’s after-tax savings capacity and cash flow of around $585 per month ($7,022 p.a.), however resulted in a net increase in her actual savings of $17,114, providing a net benefit of $10,092 per annum. This includes tax savings of $8,017. From age 60 onwards the benefit of this strategy rises to more than $12,000 per annum. The impact of this strategy on her cash flow and savings is illustrated below.

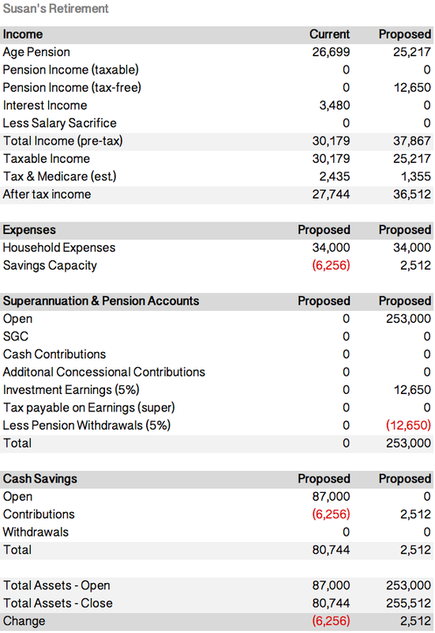

The outcome - retirement

Over time the value of this strategy compounds, adding more than $160,000 to the value of her retirement savings by the time she turns 65. This is projected to increase the total value of her savings to $1,087,000, compared to $921,000 under her current strategy. Upon retiring at age 65 Susan would be entitled to withdraw the entire balance of her superannuation should she wish to do so.

Meanwhile, over this same period of time we have estimated market price of her “dream home” will increase to approximately $790,000, plus $44,000 Stamp Duty (total $834,000), meaning that is she uses her savings to buy this home she will be left with approximately $253,000 (if she follows the strategy) or only $87,000 if she continues with her current savings.

As we previously established, Susan’s living expenses (excluding rent) is approximately $21,000 per annum. Accounting for insurance, rates, repairs and the increased cost of fuel and food in regional villages, we have estimated that her living expenses will increase to as much as $28,000 per annum is she buys her home. Accounting for inflation, this figure is likely to be closer to $34,000. The table below summarises her cash flows in retirement (Age Pension also adjusted for inflation).

Meanwhile, over this same period of time we have estimated market price of her “dream home” will increase to approximately $790,000, plus $44,000 Stamp Duty (total $834,000), meaning that is she uses her savings to buy this home she will be left with approximately $253,000 (if she follows the strategy) or only $87,000 if she continues with her current savings.

As we previously established, Susan’s living expenses (excluding rent) is approximately $21,000 per annum. Accounting for insurance, rates, repairs and the increased cost of fuel and food in regional villages, we have estimated that her living expenses will increase to as much as $28,000 per annum is she buys her home. Accounting for inflation, this figure is likely to be closer to $34,000. The table below summarises her cash flows in retirement (Age Pension also adjusted for inflation).

Summary

Susan’s case is typical of many people that we come across. Her savings regime is such that even if she does make any change to her current financial arrangements she is likely to accumulate sufficient assets to purchase her “dream home”, and will have adequate capital to afford a retirement in the lifestyle that she has become accustomed to for perhaps 20 years (to age 85). At this point she could look to downsize or release equity in her home to fund her ongoing lifestyle needs.

The key difference with our proposal was that she was that she will now, under the same conditions, have significantly more capital to fund her retirement.

While perhaps not necessarily required in the short-term, having access to this cash vastly improves her options and peace of mind should she ever face sudden or unexpected costs such as major renovations or modifications to her home or, as is common in the later stages of retirement, addressing health concerns or relocating to residential aged care.

*Name and details changed to protect client privacy.

The key difference with our proposal was that she was that she will now, under the same conditions, have significantly more capital to fund her retirement.

While perhaps not necessarily required in the short-term, having access to this cash vastly improves her options and peace of mind should she ever face sudden or unexpected costs such as major renovations or modifications to her home or, as is common in the later stages of retirement, addressing health concerns or relocating to residential aged care.

*Name and details changed to protect client privacy.