ST2017 27 December 2016

Portfolio Review - Summary

Highlights:

- Superannuation: Despite very tough market conditions, your superannuation portfolio generated modest returns which, in conjunction with your contributions, helped your portfolio grow by approximately $17,825 (+12.45%). Over the past four years your superannuation portfolio has grown by approximately $88,500 (122%, or 22.1% per annum, CAGR).

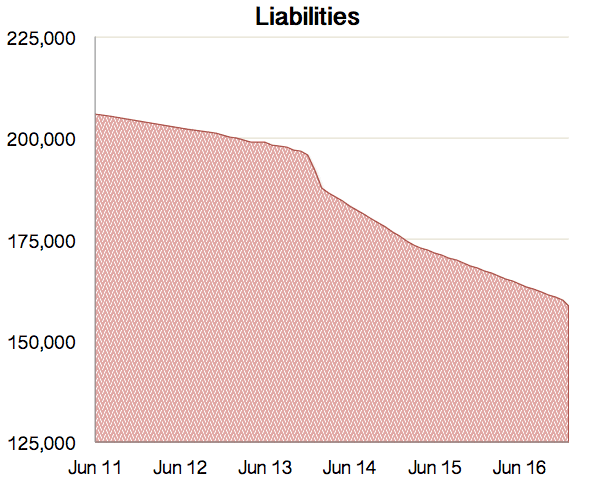

- Mortgage: By making additional repayments to your mortgage your total debt has reduced by approximately $42,000 in the past four years, including approximately $9,000 in the past calendar year. Sustaining mortgage repayments of $1,300 per month should see your debt reduced to around $131,000 by December 2020. Note: Keeping the same level of repayments but reducing your variable interest rate by 0.15% (from 4.37% to 4.22%) would reduce debt outstanding by around $700.

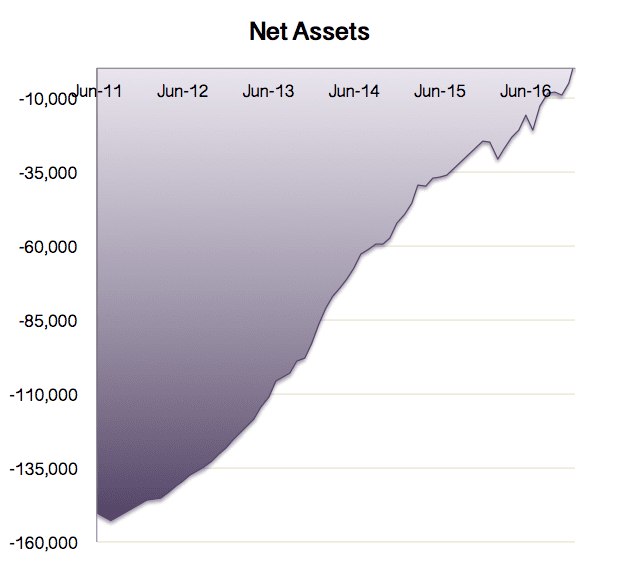

- Net Assets: Year-to-date, your Net Asset position improved by approximately $27,000 (~$130,000 over past four years).

- 9% Reduction in Household Leverage: The ratio of total debt-to-assets fell from about 34% to 31%, a reduction of approximately 8.8%. Household Leverage provides an indication of the overall level of financial debt you are exposed to.

- Investment Debt: Even more significantly, your Debt-to-Investment Assets ratio fell from 1.17 to 0.98, an improvement of 16%. A ratio under 1.0 indicates that you have sufficient investment assets to extinguish all liabilities, should the need arise.

|

|

|

Investment Strategy

Insurance Strategy

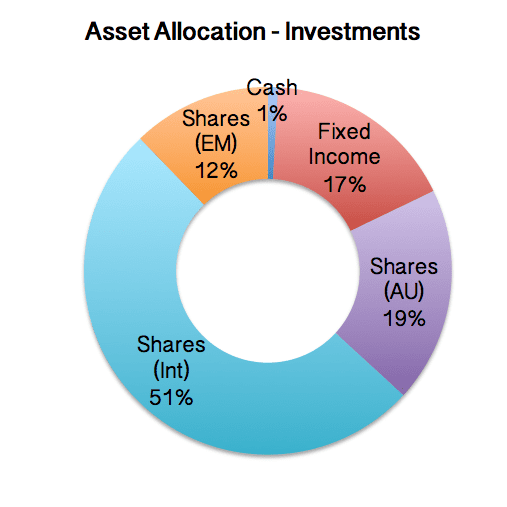

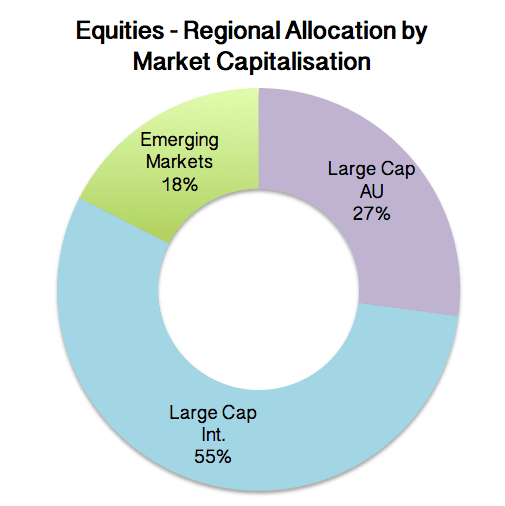

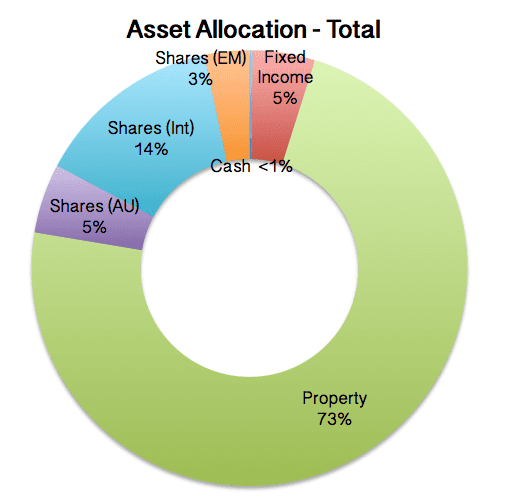

- Asset Allocation: Within your superannuation portfolio, our asset allocation has seen a slight reduction in Australian equities and transition toward emerging markets (predominantly Asian markets). We still have a substantial overweight toward international equities. While global equities face headwinds (expensive valuations for developed markets and debt-market risks in emerging markets) market risk premiums still look relatively attractive on a 3 - 5 years horizon. We retain roughly 18% in cash and fixed income assets. While yields from these sectors are very poor, they provide an important cushion in the (likely) event of a market re-pricing. To reitterate: we do expect 2017 to present considerable challenges, including some market dips which, if significant enough, will be used to increase your exposure to equities.

- Australian Economy: On this note, we do expect the Australian economy will see a recession in 2017 or 2018, reflecting the continuing deterioration in Terms of Trade and rising unemployment.

- Australian Property: Importantly, a key risk to the Australian economy is the property sector. Residential construction continues to out-pace demand, further adding to an aggregate oversupply; with Real Wages growth likely to slide backwards in the near-term, debt servicability is a significant concern. Following a 25-year debt binge, a property market "crash" of 30% - 40% (in Real terms) over the next 5 - 10 years remains highly likely.

Insurance Strategy

- You currently have $70,000 of Crisis Recovery (Trauma, held directly through AIA), plus $150,000 Life and $200,000 TPD held within superannuation (within Aon Super, insured through AIA group). The montly cost of these insurance policies is approximately $156.28 for your Trauma insurance, plus $198 for your life and TPD cover.

- As your investment assets now exceed the debt on your home, on 27 December 2016 you agreed to cancel your life insurance. This would reduce reduce the cost of your insurances by approximately $460 per annum ($38/month).

- You also wish to consider the impact of reducing your TPD insurance. If we were to reduce cover from $200,000 to $150,000 we would expect the cost to reduce by $480 ($40/mth). Reducing TPD to $100,000 would reduce the cost by approximately $80 per month.

- As discussed, TPD imposes very strict qualifying criteria, which somewhat reduces your likelihood of being entitled to a claim. To consider the value of this cover, we should seek to determing which expenses - both upfront and ongoing - that we are seeking to replace, and then compare this to out savings. As your assets are now sufficient to extinguish your debts, the dominant expenses are ongoing costs of living (with care) plus home modification expenses. Were we to allow $40,000 for home modifications plus $500 per week for living expenses, our total out-of-pocket expenses (net Disability Pension) would be around $61.50 per week ($3,200 per annum) plus modification expenses of $40,000. To support these expenses over 30 years, total savings of around $100,000 would be required. Alternatively, were you to sell your home and move into care your assets (plus additional support payments, such as Rent Assistance) should be sufficient to maintain a standard of lifestyle indefintely.

|

|

|

|

Retirement Projections

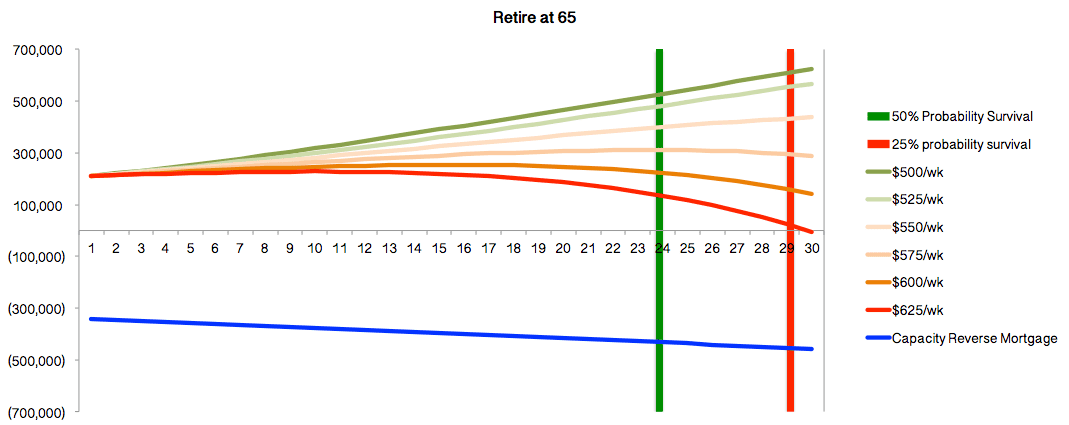

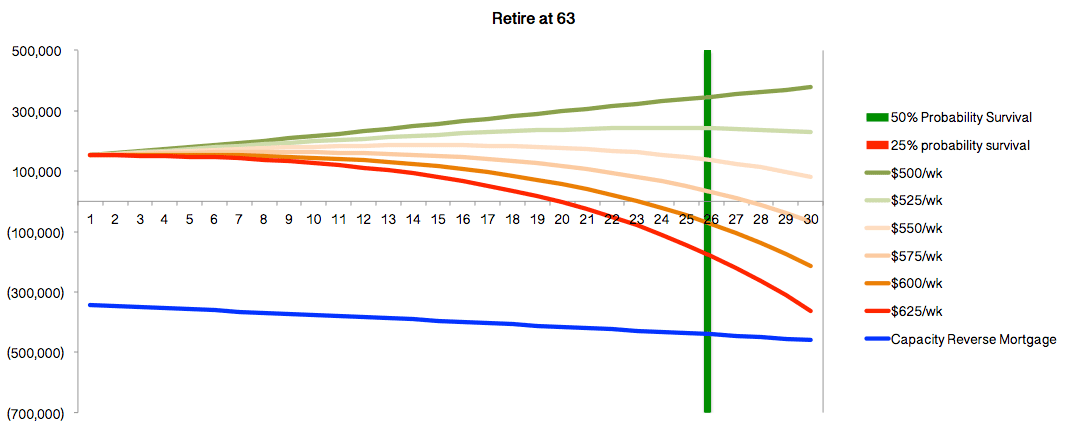

- Capital Adequacy & Spending in Retirement: While we are yet to confirm accurate numbers for your retirement expenses and budget, we can make some rough projections based upon the expected value of your savings at different ages, and calculating the impact of Age Pension over time. We present two scenarios: one in which you retire at 65, and another at age 63. We can confirm details later; this is just for a rough illustration of different scenarios. As you will notice, by age 63 we expect you to have accumulated sufficient assets to ensure 30-plus years of retirement with a spending allowance of around $550 to $575 per week. If you were to work an additional two years, to age 65, your savings would last around the same amount of time while spending $625 per week (i.e. an additional $50-$75 per week).

- Mortality Risk & Spending in Retirement: Importantly, if we look at mortality expectations, there is only a roughly 50% probability of living beyond 88 years of age, and a 25% probability of living beyond 93 years of age. This an important consideration as the longer you leave it to retire, the less time you will have in retirement, which in turn enhances your ability to spend during retirement. Adjusting for this, and looking to our account balance at 93 years of age, we see that a retirement at age 63 and spending $550 per week, will result in you having approximately the same amount left in your bank account as if you worked until 65 but spent $620 per week. In other words, working an extra two years provides you with around $3,640 per annum extra spending money in retirement.

- Aged Care: As residential aged care costs are likely to change substantially between now and when aged care becomes an option for you we will not get too deep into the details. Main thing to note is that the accomodation component of the expense is highly variable and somewhat negotiable. Changes a few years back have made the system fairer for all. While it increases some of the costs of care, many of these a "front end loaded", meaning they are most substantial in the first few years before reducing (or disappearing completely). A simple "rule of thumb" might be to treat the move into residential aged care as the accomodation bond (now called a Refundable Account Deposit, or RAD) plus about $64,000 in means-tested-care fees. In other words, if you had $500,000 of assets (including from the sale of your home) you could comfortably afford a room priced at around $400,000, while still leaving you with money for spending/excursions etc. For this price you could probably find a nice "room" with your own bathroom, storage space etc. If you did run out of cash, you can (usually) deduct care fees from your RAD. Again, don't get too caught up in the details as they will inevitably change in coming years.

Next Steps

- Renegotiate mortgage interest rate: I notice that a few lenders are advertising rates at around (just below) 4%. Ongoing fees are around $120 - $150 per annum, plus an application fee of a few hundred (~$300). On a loan of $158,000, this works out as a savings of about $585 on interest, or $335 after fees. That's equivalent to about 0.22% than your current interest rate of 4.37%. Just be careful of the fees and "special discounts", which tend to expire after 2 - 3 years before reverting to a much higher interest rate. If it were me, I would suggest that if Bank of Melbourne can offer a loan of 4.15% or lower, without ongoing fees, then this would be a good option. **There is a must lower advertised rate of 3.59% offered by State Custodians, but there are terms & conditions associated with this loan which are not on their website. Even so, use this as a bargaining chip with Bank of Melbourne. I would ask Bank of Melbourne for a rate of 4.00% and no ongoing fees. See where they go from there.

- Insurance: Let me know what you think about the levels of TPD. We can retain, reduce or cancel cover, it's up to you. While it does provide a valuable safety-net, we also need to weigh up the costs against the (extremely) low probability of claim, and the alternative use of that money. Once you let me know, I will prepare the necessary paperwork to adjust cover and cancel your life insurance through super.

- Budget, estimate of expenses: As discussed, we should try to get a more accurate estimate of your living expenses. This will help us plan for strategies both throughout this year (working out how much we can contribute to mortgage/super), plus it allows us to map out plans/cash flow for retirement (with or without working part-time), and enables us to determine how much we need to save to afford a comfortable retirement.