|

Jo Morris

|

Insurance Review - 8 March 2017

|

Dear Jo,

A little while ago I sent you an email notifying you of planned premium increases by some of Australia’s largest life insurance companies.

With the rate increases (and some reductions) now having been announced and gradually being passed onto their existing customers we feel that now is an ideal time to compare how your policy’s features and pricing compare to the broader market.

A little while ago I sent you an email notifying you of planned premium increases by some of Australia’s largest life insurance companies.

With the rate increases (and some reductions) now having been announced and gradually being passed onto their existing customers we feel that now is an ideal time to compare how your policy’s features and pricing compare to the broader market.

Summary

As part of our review process we carefully reviewed all major life insurance companies’ Income Protection products and rated them based on claims history, policy definitions, financial stability, transparency and pricing stability. Any insurer who failed to meet these basic qualitative measures were filtered out and the remaining insurance products were then reviewed and ranked based on price.

|

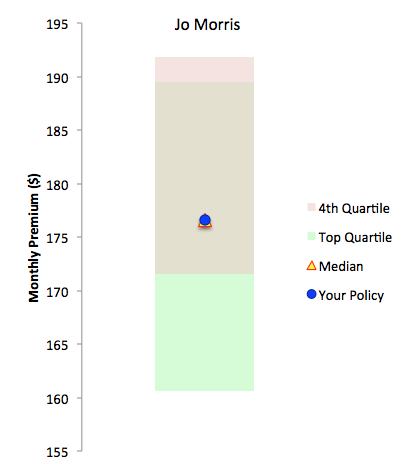

The chart below summarises our findings. As you can see, your current policy is still reasonably price competitive, but well outside the top quartile of products by price. In saying that, we did find three products that were able to offer similar quality cover at a discount of 5% or more from what you presently pay.

The lowest cost product was issued by MLC Insurance, at around $161 per month. MLC has a patchy history when it comes to their insurance products, with very narrow policy terms and high prices, however last year they were acquired by Japanese insurer, Nippon Life, and in the time since have vastly improved their policies and pricing. Other products at a similar price-point include ClearView ($166/mth) and Zurich ($172/mth). Both are good products, though Zurich offers slightly more generous ancillary benefits. It's worth noting that Zurich acquired Macquarie Life last year (which a division within Macquarie Bank); as product lines consolidate we are seeing Zurich's prices improve. |

|

Our Recommendations

With the recent change in policy terms and pricing we find that a similar level of cover is available to you for up to $180 per annum less than you are currently paying.

On the basis of cost alone, it might be at least worthwhile considering making a switch. However, there are four factors we need to carefully consider:

On the basis of cost alone, it might be at least worthwhile considering making a switch. However, there are four factors we need to carefully consider:

- There may be some loss of ancillary benefits. It can be a little hard to quantify the value of these benefits as they tend to be unique to the insurer. For example, one insurer may provide a "bonus" funeral benefit of $20,000, while another may only pay a benefit, but of a greater amount (say $50,000) if injury or death results from a specific cause. For this reason it's best to focus on the primary benefits of your insurance and regard these "extras".

- The rates are based on your continued good health and subject to satisfying the insurer’s risk guidelines (i.e., they need to be satisfied that your extra-curricula activities do not adversely affect your risk-rating)

- It will take time: Although we can manage the bulk of the paperwork it will also require some of your time to answer health and lifestyle questions (~30 min), complete a medical questionnaire (and time to sign and scan /post forms back to us), and possibly have a medical check-up (a nurse will visit you at home or office). All up, I would expect you would need to commit 1 to 1.5 hours from start-to-finish.

- Changing premiums: As you know the cost of insurance can fluctuate from year to year, mainly due to age-based risk factors, but also sometime due to changes in the competitive environment. A perfect example is AIA (your current insurer) who have gone from being the lowest-cost insurer (by a long way) to being priced close to the market average. We should be aware that the lowest cost insurer this year may be one of the more expensive insurers in 5 or 6 years time.

Next steps

If you would like to switch policies, or consider a change in the level of your cover, please let us know and we will advise you of the next step. Be aware that the rates above are estimates; before making any changes we always confirm the exact amount of the quote.

If you would like to retain your current policy there is nothing else you have to do. We will conduct another regular review as we approach your policy anniversary.

Of course if you have any questions whatsoever please contact me to discuss.

If you would like to retain your current policy there is nothing else you have to do. We will conduct another regular review as we approach your policy anniversary.

Of course if you have any questions whatsoever please contact me to discuss.

Joel Mitchell, CFA®

F.Fin, MAppFin, GDFP

Insight Wealth Solutions

Third Sector Advantage Pty Ltd T/A Insight Wealth Solutions, Authorised Representatives of Synchron, AFS License 243313