|

Scott Hannington

|

Insurance Review - 8 March 2017

|

Dear Scott,

A little while ago I sent you an email notifying you of planned premium increases by some of Australia’s largest life insurance companies.

With the rate increases (and some reductions) now having been announced and gradually being passed onto their existing customers we feel that now is an ideal time to compare how your policy’s features and pricing compare to the broader market.

A little while ago I sent you an email notifying you of planned premium increases by some of Australia’s largest life insurance companies.

With the rate increases (and some reductions) now having been announced and gradually being passed onto their existing customers we feel that now is an ideal time to compare how your policy’s features and pricing compare to the broader market.

Summary

As part of our review process we carefully reviewed all major life insurance companies’ life, disability, trauma and income protection products and rated them based on claims history, policy definitions, financial stability, transparency and pricing stability. Any insurer who failed to meet these basic qualitative measures were filtered out and the remaining insurance products were then reviewed and ranked based on price, and compared them against your existing insurance policies.

|

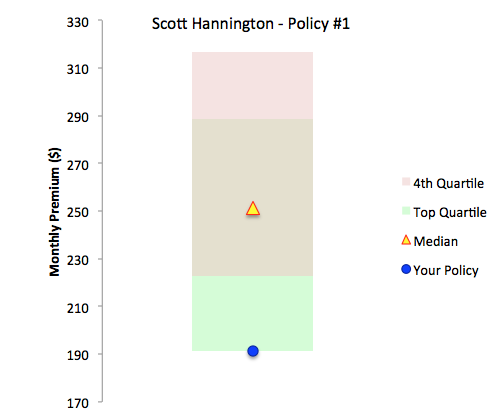

The charts beside summarise our findings. As you can see, your current policies are still very competitive, with few alternatives coming close on price or features.

Policy #1: Income Protection, Trauma & Life Insurance Your existing policy continues to offer the best value, though a number of other insurers have come close. The most notable change in the competitive landscape has been MLC Insurance, which have dramatically lowered their policy costs since being acquired last year by Japanese insurer Nippon Life. They are still slightly more expensive (by around $2/mth) however are worth watching closely in the years ahead. Policy #2: Life and Total & Permanent Disability insurance (via Super) You are currently insured for $500,000 life and $500,000 in the event of Total and Permanent Disability (TPD), at a cost of approximately $66 per month. As some background, it's interesting to note that as this policy was established via your superannuation policy on Group Insurance terms the rate you pay is not directly comparable to ordinary, fully-underwritten insurance policies. Following problems with Group Insurance among some of the large public offer super funds (basically insurers under-cutting each other and making huge losses) we saw a period where Group Insurance became quite a bit more expensive than fully-underwritten policies. As luck would have it, this happened at the same time that AIA (your insurer) was marketing heavily and offering very good policy discounts. The result being that we missed a substantial part of these fee increases. Looking at your costs today, your policy remains the lowest cost among its peers. Of course things can change, so monitoring costs and searching for a better deal should always be on the agenda. |

|

Our Recommendations

Despite the recent change in policy terms and pricing we that your existing insurance policies remain market-leading.

However, as you know, the cost of insurance can fluctuate from year to year, mainly due to age-based risk factors, but also sometime due to changes in the competitive environment. As such, it is recommended we continue to review rates no less than annually to ensure you are getting the best value for money.

However, as you know, the cost of insurance can fluctuate from year to year, mainly due to age-based risk factors, but also sometime due to changes in the competitive environment. As such, it is recommended we continue to review rates no less than annually to ensure you are getting the best value for money.

Next steps

If you would like to retain your current policy there is nothing else you have to do. We will conduct another regular review as we approach your policy anniversary. However, if you would like to alter your level of cover please let us know and we will advise you of the necessary next steps.

Of course if you have any questions whatsoever please contact me to discuss.

Of course if you have any questions whatsoever please contact me to discuss.

Joel Mitchell, CFA®

F.Fin, MAppFin, GDFP

Insight Wealth Solutions

Third Sector Advantage Pty Ltd T/A Insight Wealth Solutions, Authorised Representatives of Synchron, AFS License 243313