Ron & Marian McDonald

|

Investment Portfolio Update - 23 February 2017 |

Summary

Following our last meeting and update of your cash positions we have undertaken a full review and analysis of your portfolio exposures, including assets held within your own name and through Willathoona Investment Superannuation Fund.

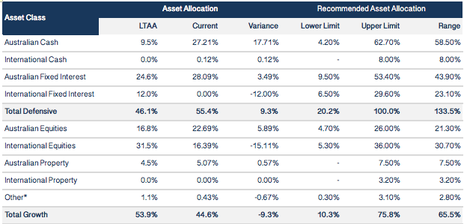

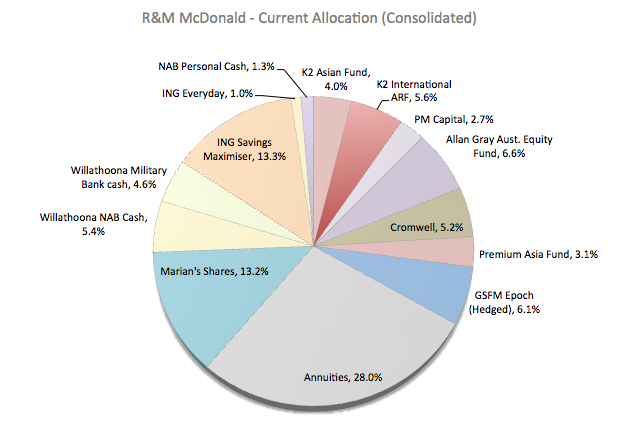

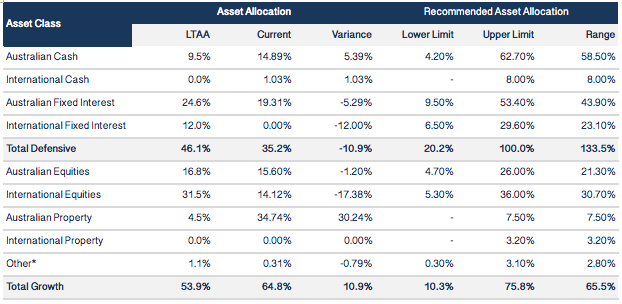

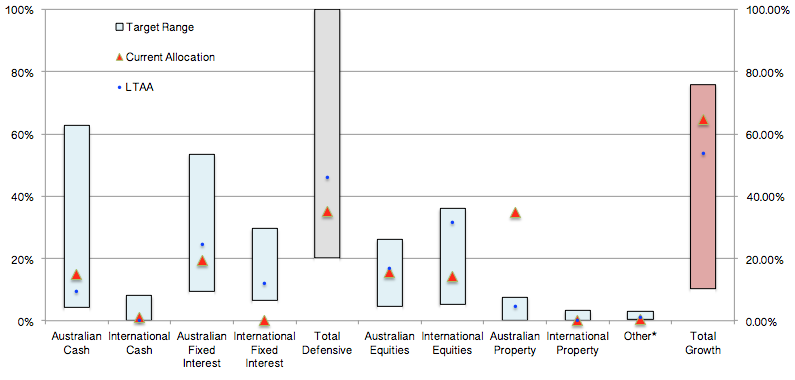

The following table summarises your current asset allocation:

The following table summarises your current asset allocation:

|

|

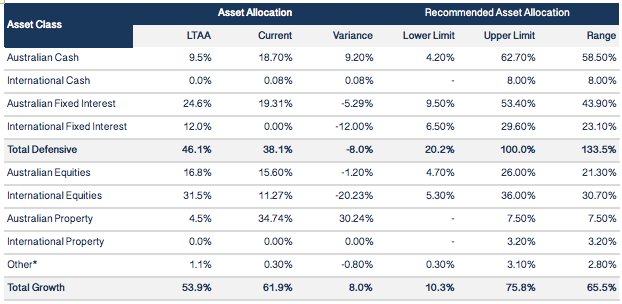

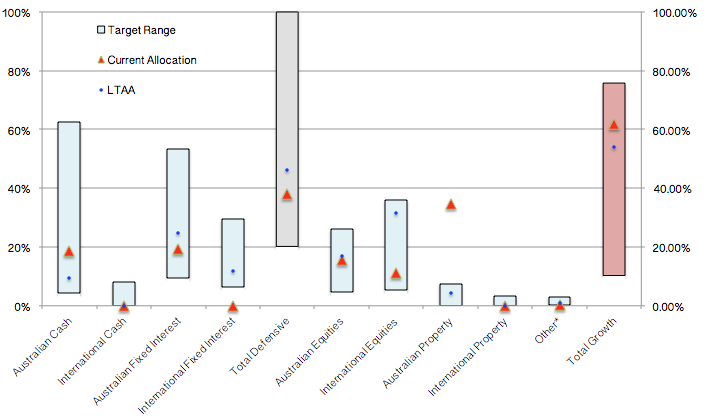

For completeness, in the table below we have also estimated your aggregate market exposure which includes your family home. The reason for this is that you have mentioned the possibility of moving in coming years. Even if this is not planned for another 5, 10, or even 15 years, it still presents an exposure to markets that must be considered. This is particularly relevant should the sale of your home be made to fund a move into residential aged care where costs are uncorrelated to movements (both up and down) in property prices.

|

|

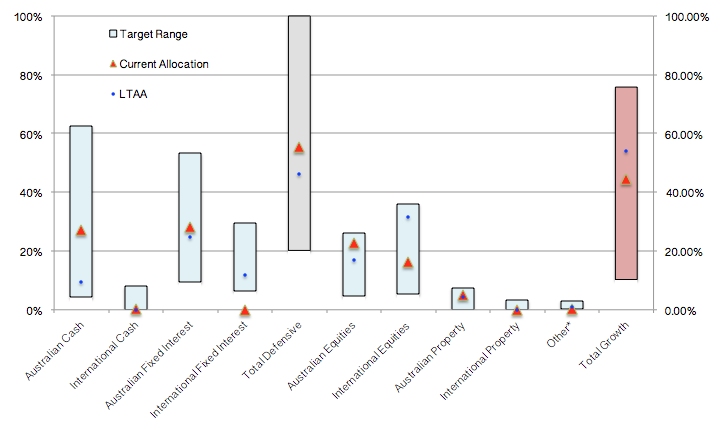

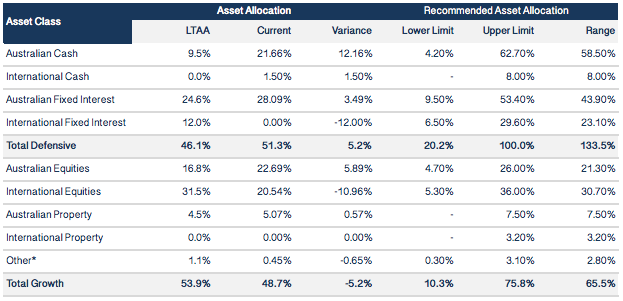

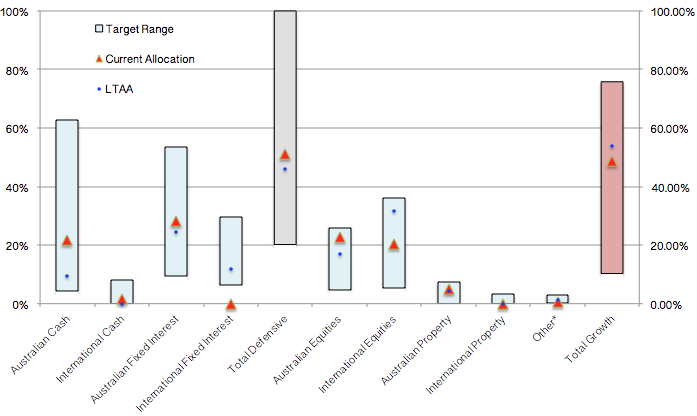

From these tables you can clearly see a number of imbalances. Some are deliberate; for example, our underweight exposure to global fixed income, whereas others, such as our exposure to property, are somewhat unavoidable.

Our Recommendations

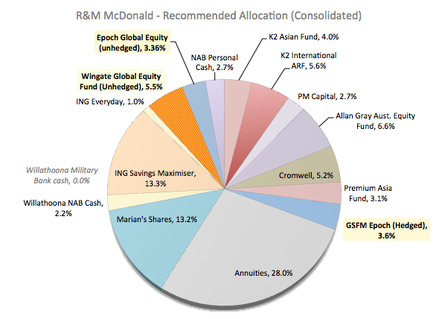

After a thorough analysis of your consolidated portfolio holding we recommend you make the following transactions:

- Pension Payment: Willathoona to make a Pension income payment of $20,000 (from NAB cash account) to Ron and Marian McDonald.

- Transfer cash balance from Willathoona’s Military Bank account (approximately $66,000) to Willathoona NAB cash account.

- Willathoona to invest $78,000 into Wingate Global Equity Fund.

- Sell $35,000 of GSFM Epoch Global Equity Fund (Hedged)

- Invest $48,000 in GSFM Epoch Global Equity Fund (Unhedged)

About Our Recommendations

We have recommended these changes for the following reasons:

1. Pension Payment ($20,000)

As your SMSF is in “Pension” mode, it is requirement that income payments be made to you (the beneficiaries) at a level at or above the minimum threshold. This threshold is age-based, and is currently set at 5% p.a. for those between the age of 65 and 74, rising to 6% between the age of 75 and 79. While there is not limit to how much can be drawn from your SMSF, there are benefits to retaining assets within the superannuation environment, particularly from a tax minimization and asset protection perspective.

As we move closer to the end of year we will look to make an additional transfer to ensure your SMSF remains compliance.

2. Transfer cash from Military Bank

When you set up the Military Bank (formerly ADCU) savings account for Willathoona we were earning an interest rate of 3.76%, which was by far the best in the market. Since then rates have dropped across all their interest-yielding products, with the rate on your account falling to 2.50%. While this is still not a terrible rate, we believe this capital can be better utilized elsewhere, both in developing Willathoona’s equity portfolio and extracting higher yields from term deposits and term annuity products.

3. Wingate Global Equity Fund

Our recommendation to invest $78,000 in the Wingate Global Equity Fund comes after considerable analysis and plays a key strategic role in maximising the risk-adjusted return from your capital. The Fund employs a long-only strategy with covered derivative exposures that allows the manager to earn additional income at the cost of some upside-potential. Importantly the Fund (via option-premium income) benefits from higher market volatility.

We have provided a full explanation of this strategy, and how it benefits your long-term objectives here.

4. & 5. Epoch Global Equity Fund

We have recommended a net $13,000 increase to your investment in the Epoch Global Equity Fund. We remain convinced of the benefit from targeting our investments toward businesses with high free cash flow and proven efficiency in managing their capital structure. Over the long-term this strategy is likely to slightly underperform the broader index, however the return profile of constituent companies should be expected to be much smoother and with much greater asset-backing (meaning that if markets were to fall heavily, there is less risk of permanent loss).

Reducing our hedged exposure by $35,000 (and increasing unhedged exposure by $48,000) reflects our belief that market and economic headwinds favour the $USD over the mid-term. We expect this to add between 8% and 9% to returns over the next three-years ($3,840 - $4,320).

1. Pension Payment ($20,000)

As your SMSF is in “Pension” mode, it is requirement that income payments be made to you (the beneficiaries) at a level at or above the minimum threshold. This threshold is age-based, and is currently set at 5% p.a. for those between the age of 65 and 74, rising to 6% between the age of 75 and 79. While there is not limit to how much can be drawn from your SMSF, there are benefits to retaining assets within the superannuation environment, particularly from a tax minimization and asset protection perspective.

As we move closer to the end of year we will look to make an additional transfer to ensure your SMSF remains compliance.

2. Transfer cash from Military Bank

When you set up the Military Bank (formerly ADCU) savings account for Willathoona we were earning an interest rate of 3.76%, which was by far the best in the market. Since then rates have dropped across all their interest-yielding products, with the rate on your account falling to 2.50%. While this is still not a terrible rate, we believe this capital can be better utilized elsewhere, both in developing Willathoona’s equity portfolio and extracting higher yields from term deposits and term annuity products.

3. Wingate Global Equity Fund

Our recommendation to invest $78,000 in the Wingate Global Equity Fund comes after considerable analysis and plays a key strategic role in maximising the risk-adjusted return from your capital. The Fund employs a long-only strategy with covered derivative exposures that allows the manager to earn additional income at the cost of some upside-potential. Importantly the Fund (via option-premium income) benefits from higher market volatility.

We have provided a full explanation of this strategy, and how it benefits your long-term objectives here.

4. & 5. Epoch Global Equity Fund

We have recommended a net $13,000 increase to your investment in the Epoch Global Equity Fund. We remain convinced of the benefit from targeting our investments toward businesses with high free cash flow and proven efficiency in managing their capital structure. Over the long-term this strategy is likely to slightly underperform the broader index, however the return profile of constituent companies should be expected to be much smoother and with much greater asset-backing (meaning that if markets were to fall heavily, there is less risk of permanent loss).

Reducing our hedged exposure by $35,000 (and increasing unhedged exposure by $48,000) reflects our belief that market and economic headwinds favour the $USD over the mid-term. We expect this to add between 8% and 9% to returns over the next three-years ($3,840 - $4,320).

Results of Our Recommendations

Implementing our recommendations will help bring your portfolio closer toward your long-term strategic asset allocation targets (LTAA) while enhancing your portfolio’s income generating potential. Our recommendations also increase exposure to foreign currency by around $80,000 (in particular $USD) as we seek to take advantage of higher US interest rates while helping protect your portfolio in the event of a market downturn or increase in market volatility. The investments recommended have been carefully selected for their risk-management and income-enhancement properties, and integration with your wider portfolio. We expect these changes to increase your portfolio's mid-term returns by approximately $4,700 per annum.

|

|

|

|

Asset Allocation, Including Family Home

|

|

Next Steps

- Transfer balance from Military Bank (approx. $66,000) to Willathoona's NAB cash account.

- Transfer $20,000 from Willathoona's NAB cash account to your NAB everyday spending/working account.

- Complete application forms for Wingate Global Equity Fund and arrange payment (from NAB cash account).

- Complete investment and redemption forms for Epoch Global Equity Fund; arrange payment for new investment. Proceeds from redemption to be paid to Willathoona's NAB cash account.

We will begin preparing the paperwork (application forms) for stage 3 and 4.

Additional Information

- Why we have recommended the Wingate Global Equity Fund: this provides a discussion around how the Fund's strategy works, and why we think it is appropriate for your portfolio at this point in time.

- Wingate Asset Management's website (managers of the Wingate Global Equity Fund): further information about the fund and performance.

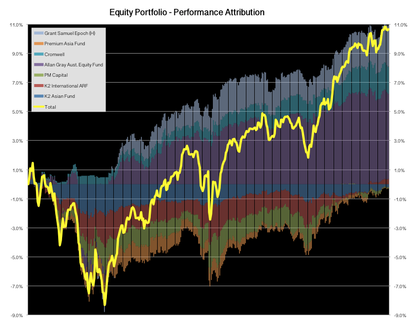

- Portfolio Update: for your reference I have provided a portfolio update (charts only) below.

Portfolio Update - 21 February 2017

|

|

|

|