Fixed Income Review - 3 January 2015

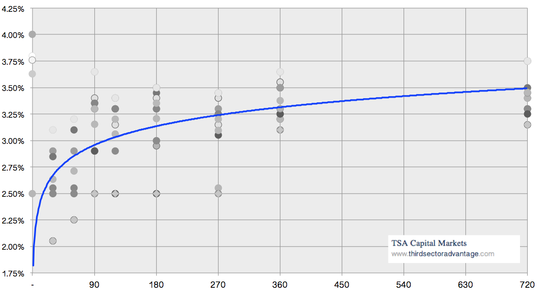

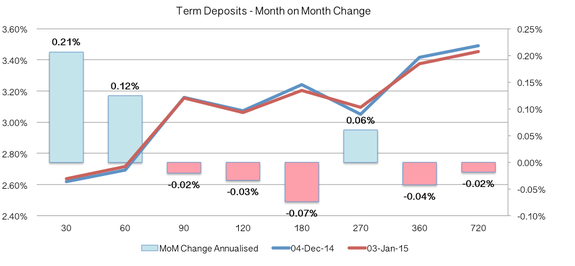

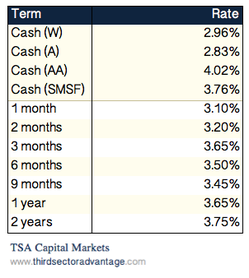

Term Deposits - remain stable

Interest rates on Term Deposits have remained very stable over the past month as all major financiers converged toward the industry average. There are a number of underlying reasons for this: credit (lending) growth has been very subdued, guidance from the RBA suggest no change to the official cash rate within the near term and and margins are already under pressure. Until one of these three factors change it's unlikely that we will see any of the majors go out on a limb to offer any particularly exciting "deals".

Bond markets - Aussie interest rate differential contracting

Bond markets, on the other hand, saw considerable movement at the "long end" of the yield curve as cracks in Australia's economy proved worse than many anticipated, while at the same time conditions in North America continued on an upward trajectory despite scaling back of QE. Overall this has seen the risk premium between Australia and the United States shrink dramatically, with the spread on 2 year Government Bonds contracting 0.35% within the past month. Over the past 12 months the spread on 10-year Government Bonds has contracted by a staggering 2.34%. You will recall that last year we forecast that compression in the interest rate differential would see the $AUD sold off heavily (as it has), however it still appears that we are lacking any meaningful increase in the Australia vs. North America risk premium. This tells us that despite our economies travelling in different directions many still believe that standard rules of economics don't apply to Australia. Time will tell, but in the meantime it's a risky time to be betting on a resurgence in the $AUD.

Interest rates 2015 - The recession we need to have?

It is perhaps also worth noting that we don't think the RBA is going to be rushing out to cut interest rates any time soon. In fact, if they do it'll be because we are sinking into recession (which is a more probably outcome for 2015 than most expect). Those in favour of further rate cuts point to our economy (source of revenues, Terms of Trade, negative real wages growth). Though we can't discount these as all good reasons to cut rates, the learned experience in Australia is that lower rates perpetuate household debt (we are terrible, terrible savers). The main culprit here is residential property. For some reason the collective wisdom of most Australians says that borrowing money to "invest" in an asset yielding barely more than cash (and with capital appreciation roughly in line with inflation) is not only justified, but a sure-fire way to get rich. But, like all good Ponzi schemes, so long as there are willing and able debtors, the house of cards can continue...

Outlook - January 2015

Looking toward the weeks ahead it's hard to see anything changing. It's a quiet time of the year for foreign bond issuances and with some heavy falls in commodity prices it's unlikely we will see too many domestic issuers in the mood for (capital raising and) spending.

Interest rates on Term Deposits have remained very stable over the past month as all major financiers converged toward the industry average. There are a number of underlying reasons for this: credit (lending) growth has been very subdued, guidance from the RBA suggest no change to the official cash rate within the near term and and margins are already under pressure. Until one of these three factors change it's unlikely that we will see any of the majors go out on a limb to offer any particularly exciting "deals".

Bond markets - Aussie interest rate differential contracting

Bond markets, on the other hand, saw considerable movement at the "long end" of the yield curve as cracks in Australia's economy proved worse than many anticipated, while at the same time conditions in North America continued on an upward trajectory despite scaling back of QE. Overall this has seen the risk premium between Australia and the United States shrink dramatically, with the spread on 2 year Government Bonds contracting 0.35% within the past month. Over the past 12 months the spread on 10-year Government Bonds has contracted by a staggering 2.34%. You will recall that last year we forecast that compression in the interest rate differential would see the $AUD sold off heavily (as it has), however it still appears that we are lacking any meaningful increase in the Australia vs. North America risk premium. This tells us that despite our economies travelling in different directions many still believe that standard rules of economics don't apply to Australia. Time will tell, but in the meantime it's a risky time to be betting on a resurgence in the $AUD.

Interest rates 2015 - The recession we need to have?

It is perhaps also worth noting that we don't think the RBA is going to be rushing out to cut interest rates any time soon. In fact, if they do it'll be because we are sinking into recession (which is a more probably outcome for 2015 than most expect). Those in favour of further rate cuts point to our economy (source of revenues, Terms of Trade, negative real wages growth). Though we can't discount these as all good reasons to cut rates, the learned experience in Australia is that lower rates perpetuate household debt (we are terrible, terrible savers). The main culprit here is residential property. For some reason the collective wisdom of most Australians says that borrowing money to "invest" in an asset yielding barely more than cash (and with capital appreciation roughly in line with inflation) is not only justified, but a sure-fire way to get rich. But, like all good Ponzi schemes, so long as there are willing and able debtors, the house of cards can continue...

Outlook - January 2015

Looking toward the weeks ahead it's hard to see anything changing. It's a quiet time of the year for foreign bond issuances and with some heavy falls in commodity prices it's unlikely we will see too many domestic issuers in the mood for (capital raising and) spending.

|

|