|

Helen Penman

|

Portfolio Review & Adjustment - 28 February 2017

|

Summary

As reporting season draws to a close our expectations have been confirmed, with a broad downgrade across industrials largely compensated by patchy but strong growth across cyclicals. On its own, this divergence between earnings results and forecasts is not a concern, however in monitoring market reaction we fear these results have been extrapolated unreasonably. Furthermore, with interest rates at historic lows (and widespread expectations of lower equity returns for developed markets) we have seen investors adapting growth outlooks by discounting their discount rates.

If we were living within a vacuum, with no exogenous variables (such as Trump, OPEC and terrorism) then this might be reasonable. But we are not.

The risk, as we see it, comes from the way that risk is being valued. Or more correctly, the way it is being ignored.

This, in turn, presents risks for all investors. For your portfolio these risks are somewhat more exaggerated by sequencing risk: that is, the exaggerated effect that market volatility can have on your portfolio when we also consider your portfolio’s cash flows. This requires us to pay particular attention to the potential impact not only from permanent capital loss, but from volatility.

If we were living within a vacuum, with no exogenous variables (such as Trump, OPEC and terrorism) then this might be reasonable. But we are not.

The risk, as we see it, comes from the way that risk is being valued. Or more correctly, the way it is being ignored.

This, in turn, presents risks for all investors. For your portfolio these risks are somewhat more exaggerated by sequencing risk: that is, the exaggerated effect that market volatility can have on your portfolio when we also consider your portfolio’s cash flows. This requires us to pay particular attention to the potential impact not only from permanent capital loss, but from volatility.

Our Recommendations

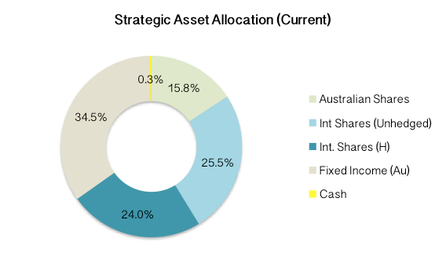

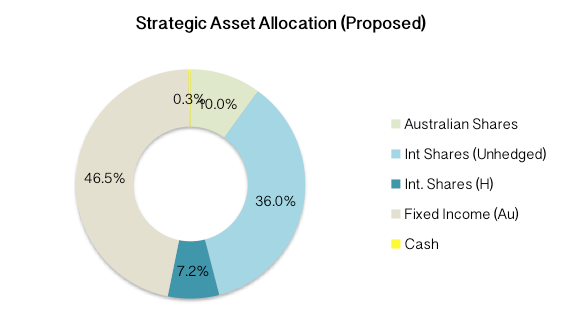

As a result we have undertaken a full risk-analysis of your portfolio’s asset exposures. Subsequently we recommend you make the following strategic adjustments to your portfolio:

- Reduce your equity exposure by approximately 12% (-6% Australia, -6% International Developed Markets)

- Reallocate equity sale proceeds toward fixed income assets

- Increase exposure to the $USD (reduce $AUD exposure) by around 10%

It is recommended that these adjustments be made with the following investment transactions:

Note: Recommended trades based on portfolio at 15 February 2017. Actual trades will be rounded to nearest 1% to achieve desired result, based on account balance at time of portfolio adjustment.

- Account Based Pension (account #2472580):

- Sell 9.8% Australian Shares Index

- Buy 9.9% International Shares Index (unhedged)

- Account Based Pension (account #27982048):

- No change

- Superannuation (account #VS34201)

- Buy 17.0% International Shares Index (unhedged)

- Sell 60.3% International Shares Index ($A Hedged)

- Buy 43.3% Fixed Interest – Australian Index

Note: Recommended trades based on portfolio at 15 February 2017. Actual trades will be rounded to nearest 1% to achieve desired result, based on account balance at time of portfolio adjustment.

|

|

Impact of Recommendations

Upon implementation of these recommendations we expect to see a reduction in portfolio returns, equivalent to approximately -0.54% in fully hedged terms, and about -0.26% per annum once adjusted for currency.

In dollar-terms, this equates to a reduction in investment returns of around $1,250 per annum or $6,500 over rolling 5-year periods. I believe that this opportunity cost, while by no means insignificant, represents a fair trade-off for greater portfolio stability and protection of capital which can be opportunistically redeployed should the opportunity arise. By way of comparison, $6,500 (the estimated 5-year opportunity cost) is equivalent to around 10.8% of the reallocated capital (~$60,000). With market volatility presently floating around 14% per annum, under normal market conditions this would suggest that we have a roughly 22% chance of seeing equity prices dip lower than this level within the next twelve months, and a 36% chance of it happening within the next five years. However, as discussed, these are not normal market conditions. Best-case scenario we expect equity prices to grow only slightly faster than global GNP, worst case we could see risk premiums spike and falls of 30% or more. In fact, even if we took a (very optimistic) view that equity premiums will continue to outperform fixed income assets by 4% per annum, then a 20% overvaluation of equity prices (and after adjusting to include our currency forecast of $USD/AUD +8.6%) indicates we should expect a greater than 77% chance of seeing the cumulative return from shares underperform fixed income over the next five years[1].

This brings us to our next point. Ultimately we want to retain sufficient exposure to market-linked assets such as shares and property so that we can preserve, as best as is possible, the inflation-adjusted value of your portfolio throughout your retirement. As such, this reduction in equity exposure may be reversed should (when) markets become substantially undervalued. As previously noted, because we are more susceptible to risks associated with price volatility (i.e., sequencing risk) we should only move to re-enter markets if assets look undervalued by 20% or more[2]. It's worth mentioning that (as a general observation) volatility tends to peak in market down-turns as investors rush for the door, which makes conveniently increases the probability of an event like this occurring. To illustrate, if current volatility (MSCI DM) is 14% and spikes to 20% when markets fall, then it becomes more than twice as likely that prices will fall by more than 20%.

In dollar-terms, this equates to a reduction in investment returns of around $1,250 per annum or $6,500 over rolling 5-year periods. I believe that this opportunity cost, while by no means insignificant, represents a fair trade-off for greater portfolio stability and protection of capital which can be opportunistically redeployed should the opportunity arise. By way of comparison, $6,500 (the estimated 5-year opportunity cost) is equivalent to around 10.8% of the reallocated capital (~$60,000). With market volatility presently floating around 14% per annum, under normal market conditions this would suggest that we have a roughly 22% chance of seeing equity prices dip lower than this level within the next twelve months, and a 36% chance of it happening within the next five years. However, as discussed, these are not normal market conditions. Best-case scenario we expect equity prices to grow only slightly faster than global GNP, worst case we could see risk premiums spike and falls of 30% or more. In fact, even if we took a (very optimistic) view that equity premiums will continue to outperform fixed income assets by 4% per annum, then a 20% overvaluation of equity prices (and after adjusting to include our currency forecast of $USD/AUD +8.6%) indicates we should expect a greater than 77% chance of seeing the cumulative return from shares underperform fixed income over the next five years[1].

This brings us to our next point. Ultimately we want to retain sufficient exposure to market-linked assets such as shares and property so that we can preserve, as best as is possible, the inflation-adjusted value of your portfolio throughout your retirement. As such, this reduction in equity exposure may be reversed should (when) markets become substantially undervalued. As previously noted, because we are more susceptible to risks associated with price volatility (i.e., sequencing risk) we should only move to re-enter markets if assets look undervalued by 20% or more[2]. It's worth mentioning that (as a general observation) volatility tends to peak in market down-turns as investors rush for the door, which makes conveniently increases the probability of an event like this occurring. To illustrate, if current volatility (MSCI DM) is 14% and spikes to 20% when markets fall, then it becomes more than twice as likely that prices will fall by more than 20%.

[1] This is calculated as: Cumulative Probability years 3 to 5 = (Prob)^n3 x (Prob)^n4 x (Prob)^n5 } – 1, where Probability = ~SD = [{(1.04^n)/1.086}-1]/(14% x sqrt(n))

[2] At this level prospective returns from equities would over a 10-year market cycle would be expected to generate a real return approximately 6%, around 33% above the long-term average for developed markets (PE expansion 20%, ERP 4.0%, RFR 2.0%, Corp Bond premium 2%).

[2] At this level prospective returns from equities would over a 10-year market cycle would be expected to generate a real return approximately 6%, around 33% above the long-term average for developed markets (PE expansion 20%, ERP 4.0%, RFR 2.0%, Corp Bond premium 2%).

Product Recommendations

While we have recommended several transactions, the underlying Funds (predominately index) are within your existing portfolio.

Why we have recommended these changes

Equity Market Exposure

With a global economic recovery well underway it may seem counterintuitive to be reducing exposure to equities, however as previously discussed we believe that investors (the market) has failed to properly consider not only the chance of an economic downturn, but also the impact of a stronger-than-expected recovery. Of course if we see no dramatic change in the geopolitical or economic landscape (or exogenous factors, such as conflict/terrorism, natural disaster) then it's likely (maybe 70% probability) that market expectations/prices are reasonable, and if we could guarantee this was the case we would be increasing our exposure to equities. Our recommendations are designed to protect your assets and dampen the impact of a potential downturn.

Currency

Within your Pension and Superannuation portfolios we have the option to invest globally with or without currency exposure/risk. Our current exchange rate is one Australian dollar for USD$0.78. We expect this to weaken in the years ahead. Our recommendation to transition toward unhedged global equities is based on a number of factors, in particular:

(1) Interest rate differentials: The market is currently forecasting four rate-rises from the United States between now and the end of 2018; compared against Australia’s monetary position, which points toward further easing if it can be accomplished without further exacerbating household debt levels, we see that for the $AUD to find additional strength we would need to see our country risk premium reduce significantly, or a spike in growth and inflation. This is not to say this isn’t possible, however it seems incredibly unlikely given how much of our growth is dependent on China’s growth ambitions and the threat of a more protectionist United States (BAT etc).

(2) Australian residential property prices: When we talk of interest rate differentials, and the risk premiums implied in exchange rates, we tend to concentrate our discussion on broad economic growth and inflation trends (covered interest rate parity, or IRP for short). One of the problems with IRP models is that it provides a poor measure of tail risk; that is, the risk that unexpected but significant events can have on currency values. Australia’s residential property prices present one of these risks. Risk-adjusted valuations are massively out of balance (overpriced in real terms by 30% - 40%) and with slowing wages growth, rising dependency rations, rising household size and continued high levels of household debt all suggest that it is a matter of when, and not if, we see prices correct. The flow on effects will likely include: contraction in the construction sector, increase in defaults, reduction in credit growth, lower consumer spending (“wealth effect”) and a high likelihood of recession. All of which point toward a more accommodative monetary and fiscal response coupled with a period of lower economic growth.

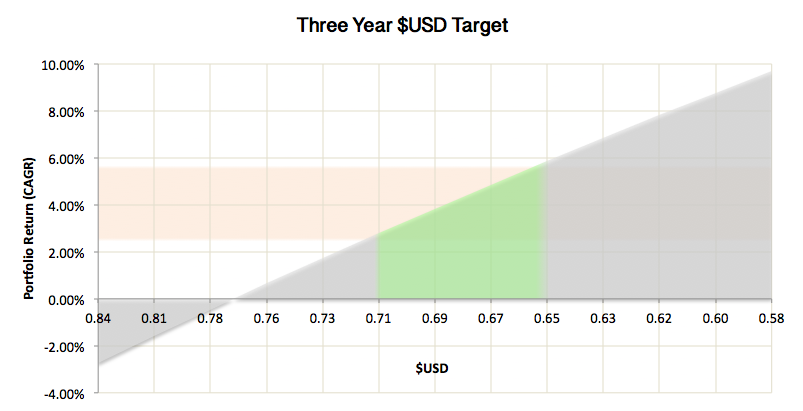

While we are not game to forecast where the $AUD will be in one, six or twelve months (and it doesn’t really matter), we can make some longer term predictions based on different economic growth scenarios. Below present our three-year Australian-United States exchange rate forecasts. Assumed hedging costs at 0.1% p.a. (total returns in brackets):

Our outlook for the next three years is for the interest rate and risk differential to widen by between 0.25% and 0.55%, suggesting that the Australian dollar will weaken to less than USD$0.71. Over a three-year period, this equates to a difference in annual return of between 2.80% and 5.86% p.a.

With a global economic recovery well underway it may seem counterintuitive to be reducing exposure to equities, however as previously discussed we believe that investors (the market) has failed to properly consider not only the chance of an economic downturn, but also the impact of a stronger-than-expected recovery. Of course if we see no dramatic change in the geopolitical or economic landscape (or exogenous factors, such as conflict/terrorism, natural disaster) then it's likely (maybe 70% probability) that market expectations/prices are reasonable, and if we could guarantee this was the case we would be increasing our exposure to equities. Our recommendations are designed to protect your assets and dampen the impact of a potential downturn.

Currency

Within your Pension and Superannuation portfolios we have the option to invest globally with or without currency exposure/risk. Our current exchange rate is one Australian dollar for USD$0.78. We expect this to weaken in the years ahead. Our recommendation to transition toward unhedged global equities is based on a number of factors, in particular:

(1) Interest rate differentials: The market is currently forecasting four rate-rises from the United States between now and the end of 2018; compared against Australia’s monetary position, which points toward further easing if it can be accomplished without further exacerbating household debt levels, we see that for the $AUD to find additional strength we would need to see our country risk premium reduce significantly, or a spike in growth and inflation. This is not to say this isn’t possible, however it seems incredibly unlikely given how much of our growth is dependent on China’s growth ambitions and the threat of a more protectionist United States (BAT etc).

(2) Australian residential property prices: When we talk of interest rate differentials, and the risk premiums implied in exchange rates, we tend to concentrate our discussion on broad economic growth and inflation trends (covered interest rate parity, or IRP for short). One of the problems with IRP models is that it provides a poor measure of tail risk; that is, the risk that unexpected but significant events can have on currency values. Australia’s residential property prices present one of these risks. Risk-adjusted valuations are massively out of balance (overpriced in real terms by 30% - 40%) and with slowing wages growth, rising dependency rations, rising household size and continued high levels of household debt all suggest that it is a matter of when, and not if, we see prices correct. The flow on effects will likely include: contraction in the construction sector, increase in defaults, reduction in credit growth, lower consumer spending (“wealth effect”) and a high likelihood of recession. All of which point toward a more accommodative monetary and fiscal response coupled with a period of lower economic growth.

While we are not game to forecast where the $AUD will be in one, six or twelve months (and it doesn’t really matter), we can make some longer term predictions based on different economic growth scenarios. Below present our three-year Australian-United States exchange rate forecasts. Assumed hedging costs at 0.1% p.a. (total returns in brackets):

- Australian economic growth lifts 1.0%, US trend growth: USD$0.84 (-8.0%)

- Australian trend growth, US trend growth: USD$0.81 (-4.7%)

- Interest rate differential widens 0.25%: USD$0.71 (+8.6%)

- Interest rate & risk differential widens 0.55%: USD$0.65 (+18.6%)

- Interest rate & risk differential widens 0.85% USD$0.60 (+28.6%)

Our outlook for the next three years is for the interest rate and risk differential to widen by between 0.25% and 0.55%, suggesting that the Australian dollar will weaken to less than USD$0.71. Over a three-year period, this equates to a difference in annual return of between 2.80% and 5.86% p.a.

|

|

Currency exposure also helps balance returns from your domestic exposure to shares and property (including your family home) as deterioration in local economic conditions will be partially offset by enhanced returns from your global equity portfolio. This is essentially an “each way bet”: if Australian economic conditions strengthen considerably and outperform the United States, we will feel the uplift in our local assets (Australian shares, your home value etc.), while our currency exposure will record a loss. On the other hand, if economic conditions do deteriorate your losses on domestic assets will be partially offset by currency gains, which then enable us to use this opportunity to bring currency profits back to Australia and invest in assets at depressed prices.

Of course the question must be asked that if we do expect interest rate and risk differentials to widen, why wouldn’t we simply divest from Australia and invest instead into hedged global equities? While this is a fair point (and is already partly reflected in our asset allocation targets), we do acknowledge that despite Australia’s headwinds (of which there are many), we are still able to extract a return premium on Australian equities. The premium is not what it used to be, but is still hovering around the 3.5% - 5% range, which from a global perspective is pretty decent.

Of course the question must be asked that if we do expect interest rate and risk differentials to widen, why wouldn’t we simply divest from Australia and invest instead into hedged global equities? While this is a fair point (and is already partly reflected in our asset allocation targets), we do acknowledge that despite Australia’s headwinds (of which there are many), we are still able to extract a return premium on Australian equities. The premium is not what it used to be, but is still hovering around the 3.5% - 5% range, which from a global perspective is pretty decent.

Next steps

If you wish to proceed with these recommendations please let me know via email (this saves both of us paperwork) and I will arrange the trades.

Of course if you have any questions whatsoever please contact me to discuss.

Of course if you have any questions whatsoever please contact me to discuss.

Joel Mitchell, CFA®

F.Fin, MAppFin, GDFP

Insight Wealth Solutions

Third Sector Advantage Pty Ltd T/A Insight Wealth Solutions, Authorised Representatives of Synchron, AFS License 243313