Disclaimer: The information and opinions provided below are provided as general information only and is not personal advice. Forecasts are based on extracts from independent analysis carried out by Third Sector Advantage (TSA). We recommend conducting your own research and consulting with your adviser prior to making any investment decision.

Background

With a FY14 operating profit of over $255 million on gross revenues of $6.37 billion, Medibank Private is Australia's largest private health insurance provider. While the company has achieved significant growth in premiums over recent years, typical of Government-owned enterprises its profitability has under performed both its for-profit and not-for-profit peers.

The opportunity for investors, as it is presented, is to acquire shares in the public listing of Medibank Private and to benefit from potential improvements in profitability (though cost reductions, acquisitions and claims management) and more aggressive marketing.

Medibank's pro forma forecast for FY15 sets forth an expected increase in premium revenue of 6.2%, plus an increase in gross margin of 0.01% and reduction in management costs of 0.5%. Overall they are looking at increasing their Operating Profit margin from 4% to 4.3%.

While management have stated their expectations for dramatic improvement to their profitability margins we should keep in mind that Medibank is planning on following a well-worn path of other private health insurers (in fact there are 34 private health insurers, 10 of which already operate on a "for-profit" basis).

Medibank is the largest private insurer in Australia. They hold around 29.5% of the market, a lead of 2.7% over Bupa (26.8%). HCF, NIB and HBF together comprise 26% of the market, with the remaining 33% of the market spread across smaller providers. Although Medibank talk a lot about being the largest insurer (by market share), it is uncertain whether this represents a meaningful advantage to their company strategy, particularly as their market share is actually spread across two brands (Medibank Private & AHM).

Private Health Insurance (PHI) premiums are overseen and must be approved by the Minister for Health. This means that improving Medibank's bottom-line (relative to their peers) must come from efficiency improvements and better (stricter) underwriting. Whether this can improve their Operating Profit from 4% to 4.3% is one thing; whether they can do it while increasing premium revenue by 6.2% is another.

I will say that some of Medibank's expectations are entirely justifiable. Medibank's expense ratio, for example, is higher than that of the existing private-sector private health insurers. Others, such as their premium growth rates and operating margins seem less likely, and almost entirely contingent on the ageing population and an increasing dependence on private sector operators for healthcare services.... sure, they may be achievable, but you would want the wind to be blowing in the right direction for everything to pan out as planned, within the timeframe set out by management.

Given that management have some tidy performance bonuses linked to revenue growth (CAGR) I would tip that we are going to see Medibank (and AHM, which is part of Medibank) ramp up advertising in the coming years. In fact to think that Medibank will be able to eek out a profit margin equal to (or higher) than their peers without either losing market share or taking a gamble on super-aggressive marketing suggests that Medibank's management know something that their competitors don't.

The opportunity for investors, as it is presented, is to acquire shares in the public listing of Medibank Private and to benefit from potential improvements in profitability (though cost reductions, acquisitions and claims management) and more aggressive marketing.

Medibank's pro forma forecast for FY15 sets forth an expected increase in premium revenue of 6.2%, plus an increase in gross margin of 0.01% and reduction in management costs of 0.5%. Overall they are looking at increasing their Operating Profit margin from 4% to 4.3%.

While management have stated their expectations for dramatic improvement to their profitability margins we should keep in mind that Medibank is planning on following a well-worn path of other private health insurers (in fact there are 34 private health insurers, 10 of which already operate on a "for-profit" basis).

Medibank is the largest private insurer in Australia. They hold around 29.5% of the market, a lead of 2.7% over Bupa (26.8%). HCF, NIB and HBF together comprise 26% of the market, with the remaining 33% of the market spread across smaller providers. Although Medibank talk a lot about being the largest insurer (by market share), it is uncertain whether this represents a meaningful advantage to their company strategy, particularly as their market share is actually spread across two brands (Medibank Private & AHM).

Private Health Insurance (PHI) premiums are overseen and must be approved by the Minister for Health. This means that improving Medibank's bottom-line (relative to their peers) must come from efficiency improvements and better (stricter) underwriting. Whether this can improve their Operating Profit from 4% to 4.3% is one thing; whether they can do it while increasing premium revenue by 6.2% is another.

I will say that some of Medibank's expectations are entirely justifiable. Medibank's expense ratio, for example, is higher than that of the existing private-sector private health insurers. Others, such as their premium growth rates and operating margins seem less likely, and almost entirely contingent on the ageing population and an increasing dependence on private sector operators for healthcare services.... sure, they may be achievable, but you would want the wind to be blowing in the right direction for everything to pan out as planned, within the timeframe set out by management.

Given that management have some tidy performance bonuses linked to revenue growth (CAGR) I would tip that we are going to see Medibank (and AHM, which is part of Medibank) ramp up advertising in the coming years. In fact to think that Medibank will be able to eek out a profit margin equal to (or higher) than their peers without either losing market share or taking a gamble on super-aggressive marketing suggests that Medibank's management know something that their competitors don't.

Expected Outcome for Investors

|

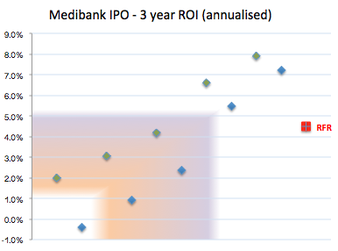

Based on an indicative listing price of $1.55 to $2.00 per share our analysis suggests that an investor's ROI is likely to fit within a range of -0.45% to +7.85% per annum. Final pricing will be announced on November 25.

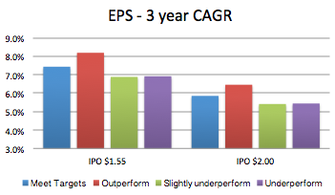

At an issue price of $2.00 per share and modest interest rate rises we expect returns to struggle to break above 2.3% p.a. over the next 3 years. The key variable here is price: we believe that $2.00 is substantially overpriced and certainly does not offer the "easy" returns seemingly expected by many retail IPO participants. This aside, earnings growth should be fairly well protected from major surprises. In fact presuming that management can maintain market share the difference between "best and worst" case pre-tax earnings is only around $109 million per annum. Management's performance relative to their targets is illustrated in the chart opposite (EPS - 3 year CAGR). From an economic perspective, deteriorating conditions are likely to adversely impact investment earnings and overall revenue growth as high-margin discretionary "extras" cover lapse rates increase and non-profit insurers potentially use their lower profit margins to claim greater market share. Although lower interest rates may improve share price multiples, we would expect to see this offset by an expansion in the equity risk premium. On the flip-side, improving economic conditions are likely to see the RBA leap to increase interest rates in an effort to dampen private-sector credit growth; this will reduce PER multiples and could substantially reduce share prices. Of course the actual outcome may be better or may be worse than any of these estimates. The chart opposite (3 Year ROI) provides our "best guess" of outcomes over the next 3 years, based on the financials of Medibank, industry growth trends, IPO price estimates provided in the prospectus, plus our own forecasts for interest rates and inflation (this feeds into our share price estimates). |

|

To buy or not to buy?

In my opinion the IPO does not offer sufficient "upside" for investors to warrant investment. The company itself will, I am sure, continue to flourish and make many (if not all) of the efficiency improvements that are being presented by management, however at a price of up to $2.00 per share the value (relative to alternative investment opportunities) does not adequately compensate for the risk of investment. For my money I wouldn't consider paying anything above $1.37, and even then I would need some convincing.

Till then it's worth remembering that often the best way to make money is to avoid losing money. This appears to be one of those times.

Updates

Final pricing of the shares was set at $2.00 for retail investors and $2.15 for institutional investors.

Shares opened trading on the Australian Stock Exchange 12:00 pm 25 November 2014 at an opening price of $2.22 (closing day $2.14)

Till then it's worth remembering that often the best way to make money is to avoid losing money. This appears to be one of those times.

Updates

Final pricing of the shares was set at $2.00 for retail investors and $2.15 for institutional investors.

Shares opened trading on the Australian Stock Exchange 12:00 pm 25 November 2014 at an opening price of $2.22 (closing day $2.14)