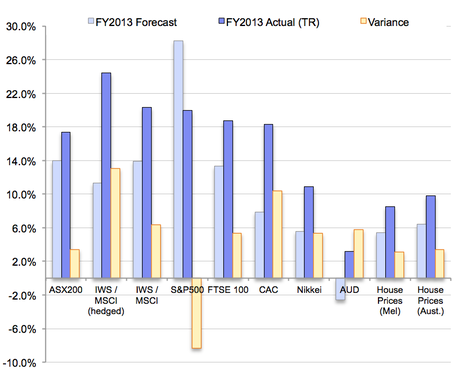

2014 in ReviewLooking back on FY2014 it's hard not to be happy with the results. At a market-level, all major developed markets achieved double-digit returns, with Australia (+17.4%), UK (+18.7%), France (+18.3%) and even Japan (+10.9%) exceeding our forecasts.

In fact the only market to fall short of expectations was the United States (+19.9% vs forecast 28.2%), which endured repeated pressures on valuations in the wake of a faster-than-expected slow down in Quantitative Easing.

The Australian dollar also had an interesting year, seemingly defying gravity as investors sought refuge from the deflationary risks of Europe and (to a lesser extent) the United States. By year-end the Aussie had strengthened by 3.2%, nearly 6% higher than our forecast of -2.6%.

Here in Australia, early signs that we're in for a smoother than expected transition from mining CAPEX boom toward public sector investment, in combination with interest rate cuts and generally improving global economic health, helped push valuations in equity, debt and property markets higher.

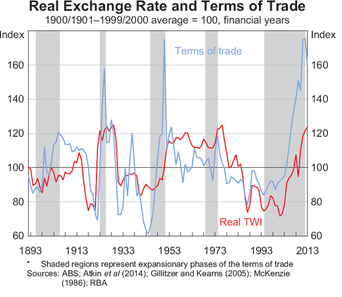

Of course, we mustn't conflate "perception" and "reality". I'd go so far as to say that the optimism which has accompanied the first signs of "green shoots" is unprecedented….well at least since mid-2007. After all, we're still standing on the shoulders of a huge boost in Terms of Trade (thanks largely to the rapid industrialisation of East Asia); it would be foolish to think that our current brand of reality is here to stay.

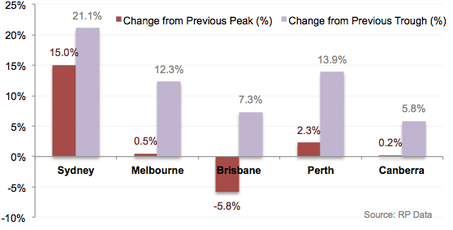

Finally, no review of the domestic economy is complete without taking a look at the Australian residential property market. As it turns out, FY2014 was a pretty good year for house prices. Even though private sector credit growth was pretty flat, Melbourne house prices soared by around 8.5% to finish the year approximately 0.5% above their 2010 peak.

While we believe Australian residential property market is overvalued (and especially Melbourne), given Australia's macro prudential settings these results aren't entirely unexpected. However they are extremely worrying. As discussed in TSA's 2013 report "Speculation and Yield Compression", Australia's recent history of loose monetary policy fuelling household debt and not spending is cause for considerable concern (as sentiment recently echoed by the RBA).

In the absence of perpetual Real wages growth this trend is not only unsustainable, but over the long term impossible. Our central thesis for a severe correction in Real house prices (equivalent to collective write-down of more than $400 billion) over the next 5 to 10 years remains intact. There will be more to come on this in coming months as we lead up to the release of the 2014 IWS Australian Residential Property Review.

|

2015: the good, the bad and the ugly.Economic OutlookAs we look to the year ahead, there are several themes which are likely to dominate the financial landscape.

At a macro-global level will be Central Banks' policy response to inflation. Generally speaking inflation risks remain low. The US Federal Reserve, ECB and BOJ all seem happy feeding fuel into the fire in the hope of stimulating a fresh investment and spending spree. And the great news is it seems to be working. The US clearly has been the most successful in this regard, though the UK, Germany and even to a lesser extent France, have all been moving in the right direction.

In contrast, those working with more extreme levels of debt and Veblen-economies like the "PIIGS" of Europe continue to struggle under the burden of insurmountable debt and a weak domestic production (as a side-note, for those with the stomach for volatility and a long investment horizon - 15 years plus - the thesis for exposure to these regions is strong).

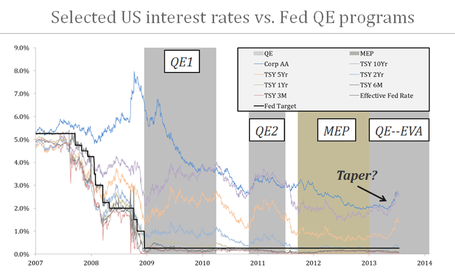

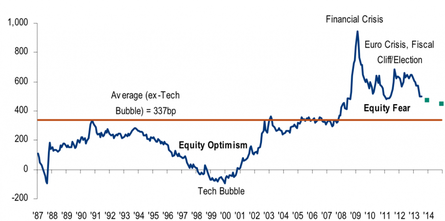

Japan is in a class of its own. Prime Minister Shinzo Abe's combination of extreme QE, tax increases and massive infrastructure investment has begun to turn the tide on over 20 years of economic purgatory. Despite some relative improvement to last year we are not convinced that Japan is out of the woods yet and retain an heavily underweight exposure to the region. Market OutlookGiven these economic conditions, as we see global activity increase we can expect to see a gradual acceleration in QE taper with a corresponding narrowing of equity risk premiums (see chart below, source: BoAML) and up-tick in inflation forecasts.

If the cost of capital remains cheap - as appears very likely - then there's a good chance we're in for a significant jump in investment activity and global growth (in fact, we expect US GDP growth in FY2015 to be roughly 50% higher than FY2014). With profits returning we should see further appreciation in equity prices over the coming year (albeit softer than last year). Whether or not we make it through the next 9 - 12 months without incident, history tells us that the prospect of a US Federal election in late 2016 is likely to brighten the mood of markets.

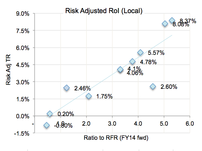

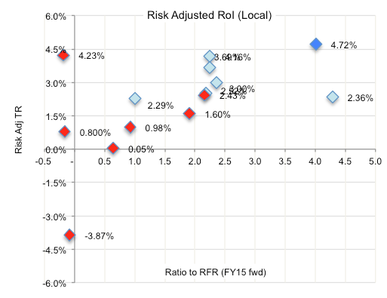

So far as how this translates to equity markets, our analysis suggests that globally most markets should perform moderately well over FY2015 (between 5.3% and 12.0%). In risk-adjusted terms, the stand-out performers include the MSCI (unhedged), long-dated Australian Bonds and, for the first time in several years, UK equities. We anticipate a significantly weaker year for short-dated Bonds and Australian property (listed and direct) to under perform. Our outlook for markets is summarised in the two charts below. The first chart illustrates forecast returns by asset class, adjusted for risk (vertical axis) and as a ratio to local 10-year government Bonds (proxy RFR).

If we compare this to the same chart presented last year (for FY2014 forecasts) it's clear that the "easy" gains have all but evaporated. If you want returns this year, you have to pay for it.

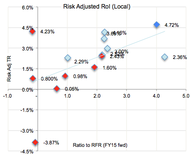

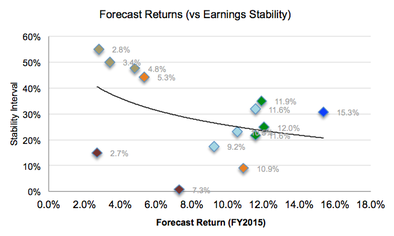

This next chart provides our market return forecasts by region (North America, Europe (ex-UK), UK, Australia, Japan etc.). The vertical axis measures earnings stability/certainty against economic conditions and policy settings. Despite equity market volatility (VIX) declining over recent months, economic uncertainty is on the increase. All in all it's shaping up to be another interesting year, albeit with some significant risks.

Local Risks & OpportunitiesBack home in Australia the picture is particularly murky. As we hurtle toward a crushing dip in GDP growth and Terms of Trade we have the uncomfortable legacy of extremely high household debt and the very likely prospect of rising unemployment and declining wages.

This feeds through nearly every part of the Australian economy, and as investors this has significant bearing on everything from currency to property to equity and debt markets.

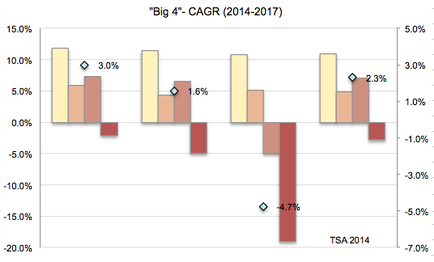

Undoubtedly the greatest risk of is to the household sector (via Australian residential property market prices) as wages growth slows (and/or unemployment rises) and credit growth contracts. From there it's really a question of whether investors are prepared to spend the next 20 years slowly deleveraging, or whether there's a rush for the exit. Recent history can answer this in pretty definitive terms. Weaker Terms of Trade flow through to our $AUD forecasts, which have been downgraded to $0.82 from $0.87 (equivalent to 14.5% currency adjustment from present value of $0.939). Obviously this presents an opportunity for local stocks with strong offshore earnings to benefit from a depreciation in the dollar. Tying this into a global economic recovery we see the greatest opportunity in companies and sectors that are likely to benefit from strong growth in organic earnings, investment spending and rising inflation. While the natural contenders are banking and insurance stocks, this is not without risk. Australia's banking sector in particular is has stretched forward earnings expectations to extreme levels. While some analysts argue that the past 10 -15 years is an indicator of future profitability, declining interest margins and slowing credit growth raises questions about the future of the sector. This is a topic explored in depth within our June 2014 Banking Sector Review, where we analysed the financial statements and projections of Australia's major banks, and set this against a range of four economic scenarios. The chart below summaries the outcomes as average Compound Annual Growth Rate (CAGR) over the next 3 financial years (FY2015 - 2017).

Clearly some banks are more robust than others, yet the potential upside does not compensate investors for this risk. As is often the case in markets, when consensus is formed on blue-sky forecasts without regard to downside risk, it's usually not a bad time to take a cold shower.

Looking 3 - 5 years down the track, our analysis does point toward slower credit growth and expanding equity risk premiums (ERP), resulting in a devaluation feedback-loop for the banking sector and property. Consequentially companies with predominantly offshore earnings are likely to offer considerably more robust earnings in the years ahead. Meanwhile we continue to monitor economic developments closely, and although 2015 is unlikely to deliver the same level of returns as 2013 or 2014, over the near-term the most probable scenario is for most developed markets to continue their march upwards, and some toward their inevitable conclusion. If you have any questions about this or any of our other reports or analysis, please do not hesitate to contact us. Market Risk and Return (Forecasts): FY2014 vs 2015

Upcoming reports

TSA Capital Markets 2014

|