ASX:DRR - Deterra Royalties Ltd

11 January 2021

Current Price: $4.42

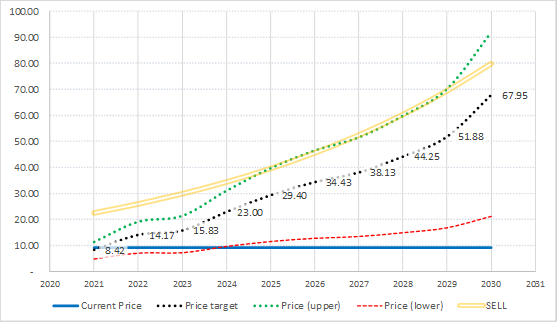

5 Year Price Target: $7.76 ($4.1 billion)

RoIC (inc. dividends): 14% pa gross / ~8.6% pa net real

5 Year Price Target: $7.76 ($4.1 billion)

RoIC (inc. dividends): 14% pa gross / ~8.6% pa net real

Background

Deterra (ASX:DRR) was created from a limited demerger of selected royalties that were previously owned by Illuka. The main asset is a royalty entitlement for Mining Area C (simply referred to as “MAC”) which pays DRR 1.232% of revenues produced within the area, plus a one-off payment of $1m for every additional DMT in annual production capacity. MAC currently only produces from their North Flank. Production on the South Flank is due to commence within the next 2 – 3 years, at which point volumes are expected to increase by around 144% to ~ 139 DMT. This is expected to be sustained for more than 30 years. In a report to WA EPA, BHP has also stated they intend to continue operations in MAC to 2073 (giving a potential effective life of up to 50 years).

DRR own four other assets including mineral sands and gold. Only one of these is producing, three are still in exploration/pre-production. Immaterial contribution to earnings.

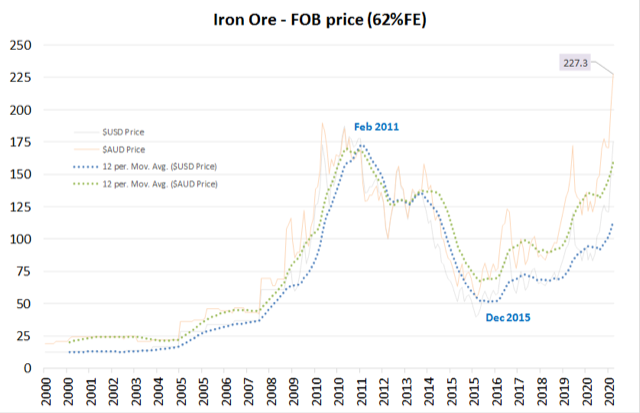

Ore prices expect to fall significantly over the mid/long term

As I write this the price of iron ore is US$169 at a similar level to the post-GFC peak from 2010 – 2013. This is mostly a result of a rapid acceleration in China’s infrastructure spend and supply disruptions (Vale etc). Even under more “normal” conditions China consumes around 75% of all global ore exports, but reports on port storage and transfer indicate they have been receiving up to 123 million DMT equivalent per week. While data out of China needs to be treated with caution it seems probable some of these imports are being used to bolster supply. If correct, it could mean a much lower iron ore price could be with us sooner rather than later.

Regardless if current prices hold up for 6 months or 5 years, there is little doubt the fall will come. Although there is some cyclicality to demand and prices longer term China’s demand will increasingly be met through recycling which could mean a permanently lower ore price. Industry forecasts vary but consensus seems to find comfort in a long term price in the US$60 – US$80 range.

Note: For Deterra, the production timeline for MAC’s South Flank (which at full production will become their producer) mean they are unlikely to see much benefit from the current peak (maybe $50 - $100m in total over the next 3 years).

Deterra (ASX:DRR) was created from a limited demerger of selected royalties that were previously owned by Illuka. The main asset is a royalty entitlement for Mining Area C (simply referred to as “MAC”) which pays DRR 1.232% of revenues produced within the area, plus a one-off payment of $1m for every additional DMT in annual production capacity. MAC currently only produces from their North Flank. Production on the South Flank is due to commence within the next 2 – 3 years, at which point volumes are expected to increase by around 144% to ~ 139 DMT. This is expected to be sustained for more than 30 years. In a report to WA EPA, BHP has also stated they intend to continue operations in MAC to 2073 (giving a potential effective life of up to 50 years).

DRR own four other assets including mineral sands and gold. Only one of these is producing, three are still in exploration/pre-production. Immaterial contribution to earnings.

Ore prices expect to fall significantly over the mid/long term

As I write this the price of iron ore is US$169 at a similar level to the post-GFC peak from 2010 – 2013. This is mostly a result of a rapid acceleration in China’s infrastructure spend and supply disruptions (Vale etc). Even under more “normal” conditions China consumes around 75% of all global ore exports, but reports on port storage and transfer indicate they have been receiving up to 123 million DMT equivalent per week. While data out of China needs to be treated with caution it seems probable some of these imports are being used to bolster supply. If correct, it could mean a much lower iron ore price could be with us sooner rather than later.

Regardless if current prices hold up for 6 months or 5 years, there is little doubt the fall will come. Although there is some cyclicality to demand and prices longer term China’s demand will increasingly be met through recycling which could mean a permanently lower ore price. Industry forecasts vary but consensus seems to find comfort in a long term price in the US$60 – US$80 range.

Note: For Deterra, the production timeline for MAC’s South Flank (which at full production will become their producer) mean they are unlikely to see much benefit from the current peak (maybe $50 - $100m in total over the next 3 years).

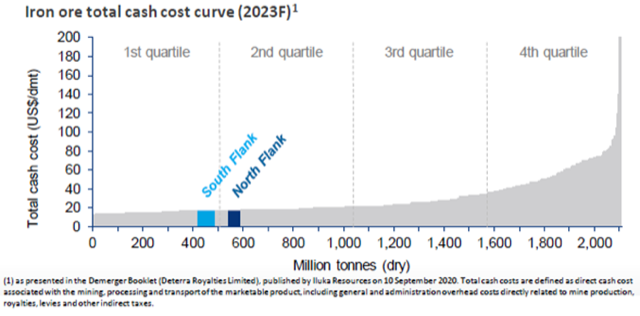

MAC (DRR’s primary asset) is a low cost producer… but marginal cost curve is flat

At global demand between 1.4 and 1.6 billion DMT the marginal cost of production cost is approximately US$40. DRR’s main asset, MAC, operates at a cash cost of less than US$20 DMT, within the cheapest 600 DMT of global production.

The marginal cost of production is important when we consider the impact that ore prices have on future investment (and thus, supply). Although MAC is among the lowest cost producers, unless ore prices fall below US$40 or $US50 it’s unlikely we will see much change to supply… and even then, production could continue at a price below the cash cost – much like we saw with Brent crude in 2014/2015.

At global demand between 1.4 and 1.6 billion DMT the marginal cost of production cost is approximately US$40. DRR’s main asset, MAC, operates at a cash cost of less than US$20 DMT, within the cheapest 600 DMT of global production.

The marginal cost of production is important when we consider the impact that ore prices have on future investment (and thus, supply). Although MAC is among the lowest cost producers, unless ore prices fall below US$40 or $US50 it’s unlikely we will see much change to supply… and even then, production could continue at a price below the cash cost – much like we saw with Brent crude in 2014/2015.

Source: Deterra Royalties 2020

Production forecasts

MAC is currently producing around 57 DMT from their North Flank, with the South Flank expected to start producing shortly and increasing total supply to about 139 DMT by 2023. For our estimates we model this as a slow increase from 58 DMT in FY2021 to 65, 92 and 132 DMT in 2022, 2023 and 2024 respectively. We assume a 30 year productive life for MAC.

Revenue forecasts

Revenue – MAC maturity

As royalties are based on the $AUD FOB value, royalties are subject to fluctuations in both the iron ore price (denominated in $USD) and the $AUD exchange rates. At full production, a US$55 – US$85 ore price would be expected to generate royalties of approximately US$103 – US$159 million per annum. At AUD$0.70 this would earn DRR between $147 and $227 m per annum.

Short-term outlook...

Deterra is expected to provide a half-year update in February 2021, their first since listing, but in the meantime we can make some estimate of their earnings based on observed changes in the ore price and $AUD, and some reasonable forecasts of prices over the remaining five months of FY2021. The table below is based on a full year production rate of 58 DMT.

MAC is currently producing around 57 DMT from their North Flank, with the South Flank expected to start producing shortly and increasing total supply to about 139 DMT by 2023. For our estimates we model this as a slow increase from 58 DMT in FY2021 to 65, 92 and 132 DMT in 2022, 2023 and 2024 respectively. We assume a 30 year productive life for MAC.

Revenue forecasts

Revenue – MAC maturity

As royalties are based on the $AUD FOB value, royalties are subject to fluctuations in both the iron ore price (denominated in $USD) and the $AUD exchange rates. At full production, a US$55 – US$85 ore price would be expected to generate royalties of approximately US$103 – US$159 million per annum. At AUD$0.70 this would earn DRR between $147 and $227 m per annum.

Short-term outlook...

Deterra is expected to provide a half-year update in February 2021, their first since listing, but in the meantime we can make some estimate of their earnings based on observed changes in the ore price and $AUD, and some reasonable forecasts of prices over the remaining five months of FY2021. The table below is based on a full year production rate of 58 DMT.

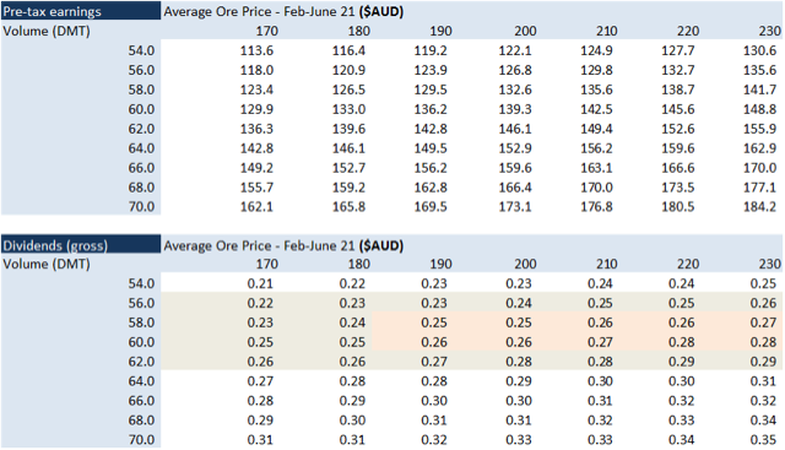

What this tells us is that if ore prices for the remaining 5 months of the year average US$155, and the AUD$0.70, Deterra would be expected to earn a pre-tax profit of around A$138 m (NPAT $96.7m). Deterra intends on paying 100% of profits to shareholders, suggesting that in this scenario investors might expect to receive gross (pre-tax) dividends of around $0.26 per share (say, $0.18 per share, fully franked).

We can extend this to consider different ore prices, exchange rates and production volumes. As ore and exchange rates can be reported simply as the $AUD equivalent ore price, a two-dimensional model sufficiently describes the range of outcomes:

We can extend this to consider different ore prices, exchange rates and production volumes. As ore and exchange rates can be reported simply as the $AUD equivalent ore price, a two-dimensional model sufficiently describes the range of outcomes:

For FY2021, total volume of around 60 DMT, and an ore price for the remainder of the year at about AUD$200 seems reasonable. That would put us on track to a pre-tax profit of $139m (NPAT $97m). A $10 fall in the $AUD ore price and 2 DMT drop in production volume reduces pre-tax earnings to about $129m (NPAT $90 m).

Revenue – production bonuses

As production ramps up on MAC, DRR also receives a one-off $1m payment for every 1 DMT increase in production. Thus, from a revenue perspective, we expect this to be paid based on a period’s total production in excess of the maximum in all earlier periods. From a cash flow perspective, this means we expect approximately AUD$82m in bonuses to be paid between 2H 2021 and 2H 2024.

Other revenue

Deterra have royalty agreements with four other projects and have a stated intention of growing their portfolio through acquisitions. They have a debt facility available, if or when required. Notwithstanding lags between development and production, most if not all acquisitions should be day one value accretive (low interest rates and DRR’s advantaged position to identify opportunities via their partners/investors).

As their existing portfolio outside of MAC generates an insignificant level of revenue, so is excluded from our analysis. Importantly DRR is not required to contribute further capital to these projects.

Expenses

DRR’s structure allows it to operate with very low overheads. Inclusive of establishment fees, they are currently spending around $6.5 m in corporate overheads, plus ~$0.5m in D&A and interest. Amortisation will increase once production begins on MAC’s South Flank, but (assuming no growth in their portfolio) I expect total expenses to be contained at less than $10m pa.

Cash flow / Dividends

DRR intends to pay 100% of earnings to shareholders. Even before MAC’s South Flank comes online, I estimate dividends somewhere in the order of $0.15 - $0.25 per share (3.4% - 5.7% per annum on current share price of $4.42). With MAC fully operational, this should increase to between $0.30 - $0.50 per share (6.8% - 11.3% pa).

As production ramps up on MAC, DRR also receives a one-off $1m payment for every 1 DMT increase in production. Thus, from a revenue perspective, we expect this to be paid based on a period’s total production in excess of the maximum in all earlier periods. From a cash flow perspective, this means we expect approximately AUD$82m in bonuses to be paid between 2H 2021 and 2H 2024.

Other revenue

Deterra have royalty agreements with four other projects and have a stated intention of growing their portfolio through acquisitions. They have a debt facility available, if or when required. Notwithstanding lags between development and production, most if not all acquisitions should be day one value accretive (low interest rates and DRR’s advantaged position to identify opportunities via their partners/investors).

As their existing portfolio outside of MAC generates an insignificant level of revenue, so is excluded from our analysis. Importantly DRR is not required to contribute further capital to these projects.

Expenses

DRR’s structure allows it to operate with very low overheads. Inclusive of establishment fees, they are currently spending around $6.5 m in corporate overheads, plus ~$0.5m in D&A and interest. Amortisation will increase once production begins on MAC’s South Flank, but (assuming no growth in their portfolio) I expect total expenses to be contained at less than $10m pa.

Cash flow / Dividends

DRR intends to pay 100% of earnings to shareholders. Even before MAC’s South Flank comes online, I estimate dividends somewhere in the order of $0.15 - $0.25 per share (3.4% - 5.7% per annum on current share price of $4.42). With MAC fully operational, this should increase to between $0.30 - $0.50 per share (6.8% - 11.3% pa).

Valuation & position sizing

Low cash production costs, long mine life and DRR’s capital and operational advantages – including very low overheads, seniority of cash flows, almost no debt, potential new income streams from low cost acquisitions and other assets – mean that although underlying earnings are pro-cyclical, over the medium term core earnings should support valuations somewhere between infrastructure (on a capital-adjusted basis) and the producers from which the royalties are paid. An environment of lower interest rates, QE and increased fiscal stimulus will also support valuations. It is, however, likely to take a few years for the market to recognise DRR (my guess: once dividends start getting paid it will attract more institutional interest and when MAC North & South are fully operational it will become a pro-cyclical yield play).

Assuming sharply lower demand from China and slower global economic growth I have based my valuation on a long-term ore price in the US$55 to US$75 range. Iron ore is Australia’s key export, followed by coal and natural gas. As global consumption of coal falls, a lower iron ore price presents a systemic risk to Australia’s economic stability and global standing, a consequence of this is a weaker $AUD.

With DRR’s royalties based on the $AUD value of DMT exports (FOB price), a weaker $AUD will help offset falls in the USD denominated ore price. For example, an ore price of US$55 DMT at A$0.60 is equivalent to an ore price of US$78 DMT at A$0.85.

Of course there are situations where DRR’s earnings could be substantially damaged. Reductions in productivity and/or increases in the cash cost of production may disincentivise management from pursuing maximal production. Typically shareholders would make a scene if management used this excuse, but given DRR’s very concentrated ownership (by entities associated with producers) there is a chance this could happen. The other risk is regulatory, environmental, or safety issues. Unlikely to have a material impact over the long term, but always a possibility.

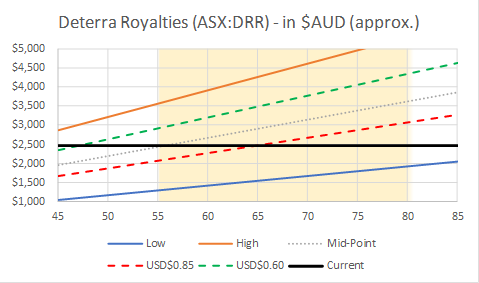

On projected cash flows we can estimate the value of DRR, first in $USD, and then based on our estimated range for the Australian Dollar:

Low cash production costs, long mine life and DRR’s capital and operational advantages – including very low overheads, seniority of cash flows, almost no debt, potential new income streams from low cost acquisitions and other assets – mean that although underlying earnings are pro-cyclical, over the medium term core earnings should support valuations somewhere between infrastructure (on a capital-adjusted basis) and the producers from which the royalties are paid. An environment of lower interest rates, QE and increased fiscal stimulus will also support valuations. It is, however, likely to take a few years for the market to recognise DRR (my guess: once dividends start getting paid it will attract more institutional interest and when MAC North & South are fully operational it will become a pro-cyclical yield play).

Assuming sharply lower demand from China and slower global economic growth I have based my valuation on a long-term ore price in the US$55 to US$75 range. Iron ore is Australia’s key export, followed by coal and natural gas. As global consumption of coal falls, a lower iron ore price presents a systemic risk to Australia’s economic stability and global standing, a consequence of this is a weaker $AUD.

With DRR’s royalties based on the $AUD value of DMT exports (FOB price), a weaker $AUD will help offset falls in the USD denominated ore price. For example, an ore price of US$55 DMT at A$0.60 is equivalent to an ore price of US$78 DMT at A$0.85.

Of course there are situations where DRR’s earnings could be substantially damaged. Reductions in productivity and/or increases in the cash cost of production may disincentivise management from pursuing maximal production. Typically shareholders would make a scene if management used this excuse, but given DRR’s very concentrated ownership (by entities associated with producers) there is a chance this could happen. The other risk is regulatory, environmental, or safety issues. Unlikely to have a material impact over the long term, but always a possibility.

On projected cash flows we can estimate the value of DRR, first in $USD, and then based on our estimated range for the Australian Dollar:

|

|

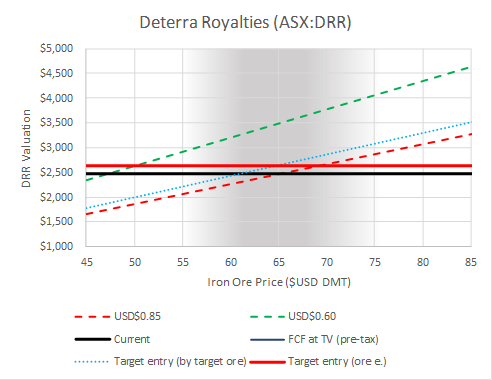

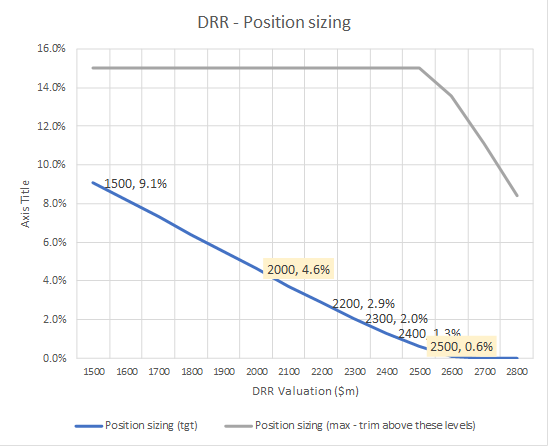

We then apply some judgement to our valuation range to narrow in our estimate of value and target entry price, and from their our target position sizing:

|

|

Summary

This is only a quick, high level look at DRR. The investment case for DRR is based on the very long life of their assets, extremely high margins, and a belief that while end user demand and prices are likely to reduce the profitability of miners, a weaker $AUD will dampen these falls. I believe there is a better than even chance that things won’t be as bad as valuations might imply…. But in saying that, the current valuation is not overly cheap and there is plenty that can go wrong. Just cheap enough to be on the radar and hoping for a 15% - 25% pull-back.

Price targets

DYOR, not advice etc. Disclosure: I hold (a very tiny amount of) DRR.

Note: a more creative/interesting approach would be hedging DRR exposure with long OTM put options on iron ore or mature producers (expiry 2023 onwards, to coincide with MAC reaching full capacity). To protect against volume gains offsetting price reductions you would need to target mature producers only — ie, those with net reduction in production over investment horizon (production volume of decommissioned mines > production volume from new sites).

_____________________________________

This is only a quick, high level look at DRR. The investment case for DRR is based on the very long life of their assets, extremely high margins, and a belief that while end user demand and prices are likely to reduce the profitability of miners, a weaker $AUD will dampen these falls. I believe there is a better than even chance that things won’t be as bad as valuations might imply…. But in saying that, the current valuation is not overly cheap and there is plenty that can go wrong. Just cheap enough to be on the radar and hoping for a 15% - 25% pull-back.

Price targets

- Current price: $2.33 billion ($4.42)

- PV: $2.64 billion ($5.00)

- 5 year target: $4.1 billion ($7.76; inc. dividends ~14% pa pre-tax, ~ 8.6% pa net real)

DYOR, not advice etc. Disclosure: I hold (a very tiny amount of) DRR.

Note: a more creative/interesting approach would be hedging DRR exposure with long OTM put options on iron ore or mature producers (expiry 2023 onwards, to coincide with MAC reaching full capacity). To protect against volume gains offsetting price reductions you would need to target mature producers only — ie, those with net reduction in production over investment horizon (production volume of decommissioned mines > production volume from new sites).

_____________________________________