Update: Cromwell Direct Property Fund (18 September 2015)

Over the past week I have been in discussion with management from Cromwell Property Group, discussing the implications on the Cromwell Direct Property Fund following the decision by investors to sell one of their key assets; a 9% stake in the Box Hill Trust.

The Box Hill Trust is a single-asset Trust, formed in 2013 to fund the building of new premises for the Australian Taxation Office in Box Hill, Victoria. At the time $66.5 million was raised, with loan financing used to fund the remainder of the $117 million completion value. Following an independent valuation of at $131.5 million in March 2015 (7.2% cap rate), the Trust was approached with an unconditional offer of $156 million (~6% cap) by a Korean investment company.With the sale of the property I felt it necessary to reevaluate the Direct Property Fund's portfolio.

Personally I liked having exposure to the Box Hill Trust. Not only did it provide an attractive tax-advantaged yield, but it complimented the Direct Property Fund's tenant profile. On the other hand, for existing investors the prospect of selling at a 19% premium to fair value was hard to pass up.

Following the sale of Box Hill the Direct Property Fund will be see look-through gearing fall to around 17%, while the rental yield from the portfolio's assets will drop from around 5.4% to around 4.6% (for the time being, the Fund has stated that it intends to continue paying 6.00 cents per unit; current unit price $1.1186).

However this still doesn't show us the full picture. Following the sale of Box Hill, around 1/3 of the Fund's property assets are tied up in their Parafield development (which has a value-at-completion of around $27.4 million). This is due for completion in May 2016, at passing yield of 8.3% (major tenant Woolworths) and development coupon of 7% along the way. In other words, come mid next year the Fund should be trading on a yield of close to, if not more than 8%.

Back to Box Hill. When we consider the impact of the sale we must be prepared that the Fund's yield will fall in the short-term. There isn't anything we can do about that. However as Parafield nears completion we should expect to see a material increase in the value of the portfolio's assets, followed by a jump in yield as Parafield comes on-line.

Sentimental feelings aside, the sale of the Box Hill Trust makes sense. If the Fund really wanted to they could easily enough redeploy their capital elsewhere at a higher cap rate. What's more, my discussions with the portfolio managers confirm my suspicion that they have their eye on other, more value-acretive assets. Unlike most of their peers, Cromwell are very, very careful in choosing which assets they do an don't buy. Which is one reason they hold such low levels of leverage and tend to make fewer, but larger investments.

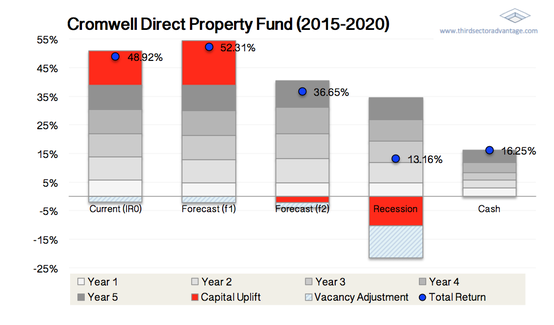

The chart above illustrates the forecast total return over the next 5 years for the Fund's assets before the sale of Box Hill "Current" and after the sale of Box Hill "Forecast (f1)". This suggests a total expected return of 8.78% per annum (CAGR). For comparison I have included a forecast projecting the expected total return in the event of economic downturn ("Forecast (f2)") and full-blown recession.

The Box Hill Trust is a single-asset Trust, formed in 2013 to fund the building of new premises for the Australian Taxation Office in Box Hill, Victoria. At the time $66.5 million was raised, with loan financing used to fund the remainder of the $117 million completion value. Following an independent valuation of at $131.5 million in March 2015 (7.2% cap rate), the Trust was approached with an unconditional offer of $156 million (~6% cap) by a Korean investment company.With the sale of the property I felt it necessary to reevaluate the Direct Property Fund's portfolio.

Personally I liked having exposure to the Box Hill Trust. Not only did it provide an attractive tax-advantaged yield, but it complimented the Direct Property Fund's tenant profile. On the other hand, for existing investors the prospect of selling at a 19% premium to fair value was hard to pass up.

Following the sale of Box Hill the Direct Property Fund will be see look-through gearing fall to around 17%, while the rental yield from the portfolio's assets will drop from around 5.4% to around 4.6% (for the time being, the Fund has stated that it intends to continue paying 6.00 cents per unit; current unit price $1.1186).

However this still doesn't show us the full picture. Following the sale of Box Hill, around 1/3 of the Fund's property assets are tied up in their Parafield development (which has a value-at-completion of around $27.4 million). This is due for completion in May 2016, at passing yield of 8.3% (major tenant Woolworths) and development coupon of 7% along the way. In other words, come mid next year the Fund should be trading on a yield of close to, if not more than 8%.

Back to Box Hill. When we consider the impact of the sale we must be prepared that the Fund's yield will fall in the short-term. There isn't anything we can do about that. However as Parafield nears completion we should expect to see a material increase in the value of the portfolio's assets, followed by a jump in yield as Parafield comes on-line.

Sentimental feelings aside, the sale of the Box Hill Trust makes sense. If the Fund really wanted to they could easily enough redeploy their capital elsewhere at a higher cap rate. What's more, my discussions with the portfolio managers confirm my suspicion that they have their eye on other, more value-acretive assets. Unlike most of their peers, Cromwell are very, very careful in choosing which assets they do an don't buy. Which is one reason they hold such low levels of leverage and tend to make fewer, but larger investments.

The chart above illustrates the forecast total return over the next 5 years for the Fund's assets before the sale of Box Hill "Current" and after the sale of Box Hill "Forecast (f1)". This suggests a total expected return of 8.78% per annum (CAGR). For comparison I have included a forecast projecting the expected total return in the event of economic downturn ("Forecast (f2)") and full-blown recession.