Mark & Julie Keenan |

Summary of Benefits (estimate) - 28 July 2017 |

Dear Mark and Julie,

I am pleased to provide a summary of the expected benefits available by making some relatively simple changes to your financial situation and structures.

I am pleased to provide a summary of the expected benefits available by making some relatively simple changes to your financial situation and structures.

Included in these estimates are allowances for investment spreads and transaction fees, however advice fees (which includes costs to update your Wills, EPoA etc) have not been accounted for.

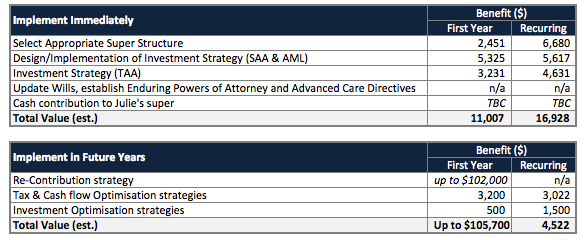

The strategies in the first table are able to be implemented immediately, while those listed in the second table ("Implement in Future Years") refers to strategies you will qualify for when Mark turns 60 and/or retires. If Julie works (in any paid capacity) during the year we might be able to take advantage of the co-contribution (compared to the other items on the list it's not a major windfall).

For the purpose of calculating benefits I made the assumption that Mark retires in about 2 years time; at this point, and following implementation of the strategies above (some have multiple "moving parts") we estimate the total recurring benefit - that is, the difference between implementing changes and your current structures - will be equivalent to around $20,000 per annum. I have excluded any benefits related to salary sacrifice arrangements as (for the purpose of calculations) I assumed Mark is already taking advantage of his tax-deductible (concessional) contribution limits.

I will also draw attention to the "one-off" benefit of around $102,000 from the re-contribution strategy. While this is technically correct, it's also a "worst-case" scenario; assuming you both continue to lead a long and healthy retirement the value of this benefit will reduce over time. If I were to put a rough value on this part of the strategy, I would say it is around $30,000 to $50,000. Even so, that's a great return for filling out a bit of paperwork. All-in, we expect the cumulative benefit over the next 5 years to be around $100,000.

Finally, while the estimated benefits are quite substantial the actual strategies involved are not overly complicated. What's important is getting things setup correctly the first time, and knowing what to look for when reviewing your portfolios, means that you can focus on more important things like enjoying your retirement.

Take some time to review this schedule of benefits and we will talk soon about the next steps. Have a great weekend.

Kind Regards,

Joel Mitchell, CFA

Director, Insight Wealth Solutions

The strategies in the first table are able to be implemented immediately, while those listed in the second table ("Implement in Future Years") refers to strategies you will qualify for when Mark turns 60 and/or retires. If Julie works (in any paid capacity) during the year we might be able to take advantage of the co-contribution (compared to the other items on the list it's not a major windfall).

For the purpose of calculating benefits I made the assumption that Mark retires in about 2 years time; at this point, and following implementation of the strategies above (some have multiple "moving parts") we estimate the total recurring benefit - that is, the difference between implementing changes and your current structures - will be equivalent to around $20,000 per annum. I have excluded any benefits related to salary sacrifice arrangements as (for the purpose of calculations) I assumed Mark is already taking advantage of his tax-deductible (concessional) contribution limits.

I will also draw attention to the "one-off" benefit of around $102,000 from the re-contribution strategy. While this is technically correct, it's also a "worst-case" scenario; assuming you both continue to lead a long and healthy retirement the value of this benefit will reduce over time. If I were to put a rough value on this part of the strategy, I would say it is around $30,000 to $50,000. Even so, that's a great return for filling out a bit of paperwork. All-in, we expect the cumulative benefit over the next 5 years to be around $100,000.

Finally, while the estimated benefits are quite substantial the actual strategies involved are not overly complicated. What's important is getting things setup correctly the first time, and knowing what to look for when reviewing your portfolios, means that you can focus on more important things like enjoying your retirement.

Take some time to review this schedule of benefits and we will talk soon about the next steps. Have a great weekend.

Kind Regards,

Joel Mitchell, CFA

Director, Insight Wealth Solutions

About your Adviser

Your wealth adviser is Joel Mitchell, CFA®. As Senior Portfolio Manager and Director of Insight Wealth Solutions, Joel has been providing strategy and investment advice to clients for over a decade and presently advises on a portfolio of assets valued at more than $220 million on behalf of superannuants, professional investors, charitable foundations and the Australian government.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.

Joel is a Chartered Financial Analyst (CFA), Fellow of FINSIA, holds a Masters degree in Applied Finance, Certificate in Investment Performance Measurement (CIPM®), Graduate Diploma of Financial Planning, and has expertise in Self-Managed Superannuation Funds, mortgage broking, stock broking, taxation law, business succession planning, property economics, resource operations and engineering. Before beginning his finance career he was a paratrooper and assault pioneer with the 3rd Battalion, Royal Australian Regiment.

Outside of work, Joel is on the Education Advisory Committee (EAC) for CFA Institute and is regularly called on to sit on the Board of Management and advisory committees of not-for-profit organisations and private companies. He is also the author of “Not for Profits in Australia: A Boardroom Guide to Asset Management” and “IWS Residential Property Review”.