Strategy Update - October 2015

Overview

The past few months have been dominated by market volatility, with investors growing increasingly anxious about whether a US economic recovery can sustain itself in the midst of a likely Fed rate hike later this year. This is a very real concern, after all we have China slowing who (as we saw on two occasions in August) are willing to pull their trump card; a trifecta of currency devaluation, fiscal stimulus and monetary loosening. But for now US is delivering some fairly decent economic data with relatively low inflation, which is good news for investors. Europe has also continued to strengthen, and while debt levels are still higher than we would like, relative to the US and Australia valuations appear fair.

Meanwhile Australia has been going the other way. Earnings growth remains lackluster, labour costs are high and margins are under pressure. While a weaker $AUD has helped dampen the decline in some sectors we still have a significant proportion of our eggs in the commodities basket, the consequence of which is further downward pressure on aggregate earnings. With further weakness in commodity prices expected, the $AUD is currently trading at US$0.72 and the yield on long-dated treasury Bonds has evaporated. Capital seems to have flowed into equity markets in what looks to be investors chasing returns while standing very close to the exit door.

In light of these conditions we have made a number of important changes to our investment strategy. For some investors these changes will be immaterial, however for others this may cause substantial shifts in portfolio allocations. A summary of personal recommendations will be provided over the next week.

The following is a summary of our key moves and motivations:

Meanwhile Australia has been going the other way. Earnings growth remains lackluster, labour costs are high and margins are under pressure. While a weaker $AUD has helped dampen the decline in some sectors we still have a significant proportion of our eggs in the commodities basket, the consequence of which is further downward pressure on aggregate earnings. With further weakness in commodity prices expected, the $AUD is currently trading at US$0.72 and the yield on long-dated treasury Bonds has evaporated. Capital seems to have flowed into equity markets in what looks to be investors chasing returns while standing very close to the exit door.

In light of these conditions we have made a number of important changes to our investment strategy. For some investors these changes will be immaterial, however for others this may cause substantial shifts in portfolio allocations. A summary of personal recommendations will be provided over the next week.

The following is a summary of our key moves and motivations:

Summary:

A further explanation is provided below:

- Global macro positioning – moving to slight underweight equities, neutral bonds and overweight cash (and short-term bullet bonds)

- Further reducing our exposure to Australia (from underweight to heavily underweight)

- Reducing our exposure to North America from overweight to neutral

- Increasing our currency hedging to 60% or more

- Slight increase in our exposure to Europe; roughly neutral relative to benchmark

- Increase exposure to China from underweight to slight overweight

- Commodities: overweight benchmark (in particular oil, however expect 5 -10 years for this strategy to play out)

- Fixed income markets: exit Australian corporate debt and reduce exposure to long-dated treasuries. Actively reduce portfolio duration, look to 3-5 year re-set on bullet-bonds.

- Australian residential property market still a concern and threat to economic stability and growth outlook.

A further explanation is provided below:

|

Macro Positioning - reduce equities, neutral bonds, overweight cash

|

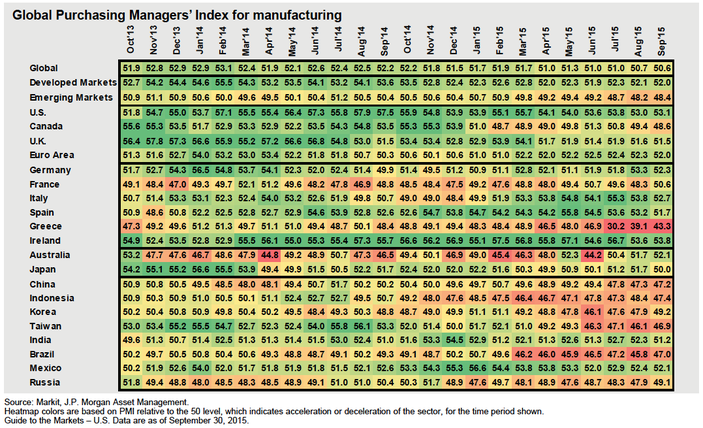

Globally economic conditions are better than they have been for some time. Trend GDP is still soft, but has resumed to levels that restore our faith that forecasts of "GFC Mark II" are now dead in the water (of course some markets are weaker than others, but we will get to that later). Our expectation is for further wind-down of quantitative easing and increases in interest rates. While this increase in rates could be cause for concern among the less well-developed markets (particularly those still using QE who have large amounts of foreign debt), so long as inflation can keep pace with the rise in interest margin, we should hopefully avoid too much of a mess. In summary: things are better than they were (5 years ago), but they still aren't great. From a valuation perspective, it could be argued that developed market equities are now priced to reflect (a) slow-but-steady earnings growth with continued low interest rates, or (b) strong earnings growth with moderate increases in interest rates. This is a fairly logical way to think of market pricing, but it doesn't leave a lot of room for error. If we were to use the US as proxy for global markets, we would see signs pointing toward a moderate increase in rates combined with a generally slow upward trend in earnings growth. In this case the upside potential for US equities (and global equities in general) seems fairly limited. It's still there, but it's hardly compelling. Given where we have come from, valuations appear to be moderately overheated, and in response we are reducing our overall equities exposure from net neutral to slight underweight. In these conditions we could almost skip over commentating on Bond markets, except to say that I was wrong. If you remember, 2 - 3 years ago I was forecasting a stronger-than-expected recovery in US equities (and market consolidation), from which we made the strategic call to heavily overweight US equities and $USD while getting as far away from mid and long-dated Bond markets as we could. Well, two out of three ain't bad. The Bond "crash" never eventuated. Why? Well, probably something to do with the way that QE was spent. We didn't see the inflation I thought we would but we saw business spending (and credit) pick up, so here we are: without QE but still sitting on ZIRP. From here it seems that markets have had plenty of time to catch their breath, and Bonds in most markets now seem fairly priced. Finally, cash. For most investors the real return (i.e., return net inflation) is tracking between -1.0% and +0.5%. Some incremental value can be obtained through short-term bullet-bonds. We are overweight cash primarily as a means of risk management and liquidity. The drag on returns caused by our overweight exposure to cash can be justified by expectations of valuation anomalies in (select) equity markets. This cash will be re-delployed as conditions normalise (or move into "cheap" territory).

|

|

Reduce Australian equities from underweight to heavily underweight

|

For several years now we have been heavily underweight Australian equities as we believed equity pricing did not properly reflect risk and overestimated earnings growth. This was one of the reasons we took such a heavy tilt away from Australia and toward unhedged North American equities. More recently Australian equities have had more than their fair share of "bad luck", a large amount attributable to our saviours through the GFC: China. And it doesn't look like getting much better anytime soon. Household debt levels are at extraordinary levels, unemployment has began to tick upwards, and even the influx of cheap credit has not been enough to spur on inflation (or meaningful levels of credit growth even!). But now if you value the Australian share market you could be excused for thinking otherwise. Valuation premiums (equity risk premiums) are below trend while Price-to-Cash flow ratios are now roughly 30% above trend. By our estimates, the Australian equity market is overvalued by around 7%, but with potential downside risk in the order of 20% - 30% should we slide into recession. While there are opportunities within the Australian share market, the market as a whole does not offer sufficient return to justify the risk. Almost counter intuitively, the areas that we do see value in tend to be cyclicals (example: energy companies with very low debt).

|

|

Reduce North American equities

|

Considering the economic growth and interest rate outlook, North American equities now appear moderately expensive. It also looks like domestic production has outpaced demand, leading to a sharp increase in inventory levels (not at critical levels, but could still cause some discounting in the near term). Though as a whole the market is not necessarily overpriced (earnings still look good) we believe it's sensible to moderate our exposure to the region. For many investors this will result in a meaningful change to portfolios (as our overweight exposure to the region has been further exacerbated by strong returns in recent years). Long term we still like the region, so for investors with multi-decade investment horizons North American equities should still provide a core element of global equity portfolios.

|

|

Increase currency hedging

|

The Australian Dollar is currently trading at around USD$0.72. While the outlook for economic growth and interest rates (both in Australia and the US) will place further downward pressure on the dollar, on the balance of risk it appears that there is an equal if not greater level of risk that the Australian dollar could strengthen from this level. Currency markets appear to have factored in a reasonably pessimistic view of Australia already. From a strategic perspective our decision to apply currency hedging is to help absorb risk from our heavily underweight Australian equities portfolio: in other words, if our equities call is wrong and Australia's economic growth rebounds strongly, then some of the losses from not holding Australian equities should be absorbed through a strengthening $AUD. The counter of this is that we believe the $AUD is already priced with expectations of economic downturn in mind, thus meaning that if we are correct the premium received from a weaker $AUD will not fully reflect the weakening of the Australian economy. Besides, if the Australian economy does weaken, it is unlikely we will want to unwind our $USD exposures to invest locally, instead we would use local cash to increase our overall equities exposure. In some ways this is an "each ways bet", but on balance we believe it is the best way to manage risk.

|

|

Slight increase to European equities

|

As previously mentioned, European equities are currently trading at a slight discount to trend, with the UK, Germany and France trading roughly 5% - 10% below trend on a justified PE and book value basis. There is not yet sufficient evidence that the recent accelaeration in earnings growth isn't just a flow-on effect from the ECB's QE program (which is still running hot), as such we feel it's better to be cautiously optimistic and selective with our exposure to European equities.

|

|

Increase exposure to China

|

For all the problems that China faces, long term it's the place to be. While all signs point to economic growth slowing in absolute terms they are still racing ahead of every other major economy, while transitioning toward capitalism. What many investors should find interesting is that valuation of their equity market from a fundamentals perspective uncovers significant untapped anomalies, not only relative to other global markets, but to their own. Even if China's economic growth fell to 2% their markets would still appear fairly priced. There are a number of reasons that China appears to trade so cheaply. Their market is highly concentrated, the market is informationally inefficient and the cost of credit is still relatively high. But on the flip side, this concentration can be managed and by leaning toward assets with strong balance sheets we can build in a margin of safety. For investors with a multi-decade investment horizon, we expect value to be extracted from a number of sources: (1) a narrowing in the risk-spread between China and the rest of the developed world should see the prices of Chinese list companies expand; (2) the wealth affect flow through to consumption; (3) real GDP growth; (4) lower cost of debt; (5) transition from export-driven to consumption-driven growth. Late last week China's central bank added fuel to the fire by lowering the official cash rate by 0.25% and reducing bank reserve requirements. In the near term equity market prices may still come under pressure, however over the mid-term we hold very high hopes for China's economy and markets.

|

|

Commodities: overweight oil

|

December last year we moved back into commodity markets, favouring oil. In hindsight it appears we moved too early, and while prices have improved over the course of the year the outlook still looks dire. As explained earlier in the year, this was a consequence of the deliberate flooding of the market by OPEC in an effort to shut down North American shale operators. And at a market level they did a fairly good job. However the problem for OPEC here is threefold: (1) Shale operations are inherently elastic (and low cost) - they can quickly and easily re-start operations as soon as it is financially viable to do so; (2) at a market level the bulk of financial loss has been sustained by OPEC members (to the tune of roughly $1 trillion, by my estimates); (3) lower oil prices mean less investment in new "traditional" wells (which can cost in excess of $40 billion to build), reducing long run supply; (4) lower oil prices act as an indirect economic stimulus to net importers of oil (which is pretty much everywhere but OPEC members and Russia). In other words, this flood in supply has actually helped boost economic growth and consumption of net importers while slowing economic growth among OPEC members, while at the same time burning through billions of dollars of savings. If IEA data is anywhere near correct (which is a debate for another day) depletion of supply not really a major consideration at this stage. Similarly, Indonesia rejoining OPEC and Iran lifting supply should have any meaningful impact on global supply (Iran has high sunk and lift costs). While anecdotal evidence suggests that Saudi Arabia can lift oil (i.e., extraction from existing wells) for only a few dollars a barrel, they do not have the infrastructure to meet supply alone. If we expect global consumption to increase over the next 10 - 20 years we will need to see new investment, and at US$40/bbl it doesn't make sense for anyone (not even Saudi Arabia) to invest in new wells. The key negative for oil prices mid-term is that Strategic Reserves are filling quickly. Although the US does not confirm how much spare capacity they have, using their stores at Cushing as proxy, there is reason to believe that oil prices may fall in the short term: indeed 2 month futures are cheaper than 1-month futures, reflecting market expectations that prices will fall further ("contango").

In fact if you want to see how scared markets really are, check out Russia's market and economic forecasts. Their economy is broken (they don't have the same cash reserves as OPEC's key players), but for the brave (crazy?) investors who are dipping their toes in the Russian equity market, the potential payoff (and risk) is astronomical. Market fundamentals (PE, PB, P/CF) are trading at around 4 standard deviations below trend! The point is that talk of the risk of a further downturn in oil markets is more than just doomsayers jumping at shadows -- it is literally the lived experience of some of the world's largest oil producing nations (Russia is the world's single largest oil producing nation, but their lift costs are much higher than their Arab rivals). From an investment perspective our preferred market is Brent, the idea being that prices will have maximum sensitivity to price volatility on the upside, with less political risk. To explain, we consider that disruption to supply from OPEC through the strait of Hormuz would be devastating for oil markets, however on the other hand if the relationship between Arab nations and the US/Europe broke down, or if sanctions were imposed, we could see a supply glut form in Hormuz ports while at the same time stretching demand for oil from "safer" waters (such as North Sea). While none of these outcomes would be good from a political or social perspective it would likely help boost Brent returns over the short term. Based on the marginal cost of production (sunk cost and uplift cost) we should expect a price closer to US$65-$70/bbl (adjusted to inflation). Current price of Brent Crude US$47.9/bbl. Short-term investors may prefer to access the market via futures (remembering we are in contango), however for passive investors looking to increase exposure to oil over the long term there are some reasonable alternatives. Example Betashares Oil ETF (ASX:OOO); currently trading at $19.34. |

|

Fixed income markets

|

Within the Australian fixed income markets we recommend selling existing holdings of sub-A grade corporate debt on concerns that economic weakness - and the threat of recession - could trigger a widening in credit spreads, and with it substantial capital loss. The additional margin received for risk has all but disappeared. I am also recommending shortening portfolio duration by reducing exposure to long-dated treasuries and reallocating toward short and mid-term Bonds. Present valuations of long-dated treasuries show that liquidity premiums have all but disappeared, and while this might be justified if we were expecting to fall into a deep and long recession we don't think that the economic outlook is quite that depressing (and if it is, then out decision to heavily underweight Australian equities and property should provide us with sufficient cash to extract yield from discounted equity or debt securities).

Globally long-dated treasury Bonds also look very expensive, however unlike in Australia we actually like high-yield debt in both the United States and Europe. While there is substantial duration risk (value will be lost if/when interest rates go up), as risk comes off the table we expect the high-yield sector to benefit from a reduction in risk spreads and, ultimately, the reclassification of high-yield into investment-grade debt. |

|

Australian residential property market

|

There isn't much here that hasn't already been said. As I've written about on many occasions the Australian residential property market is (in aggregate) extremely overvalued, now trading with similar return characteristics to Treasury Indexed Bonds, but of course with much greater risk. Interestingly some talk of a "bubble" has made it through to mainstream media, but of course have been dismissed by property "experts" like real estate agents. We retain our "sell" recommendation over Australian residential property (at an asset-class level) and while we expect a correction in the mid-term (within the next 5 - 10 years) we don't expect it to be too dramatic; perhaps a 15% - 20% fall in prices before a protracted period of stagnation. Locally, Melbourne property prices would need to correct by roughly 35% (from current levels) to justify investment (relative to other opportunities). We reaffirm our sell rating and warn that sectors tied to the residential property market (and household credit growth) may have a tough few years ahead.

|